30 September 2022

Global Market Outlook

Global Market Outlook

Navigating a difficult near-term outlook

Fighting inflation remains central banks’ top priority. This makes a recession and further near-term downside in equities more likely, with the debate shifting to whether such a recession is going to be shallow (which is likely priced in) or deep.

We believe (i) Rebalancing into investment grade corporate bonds and some deeply undervalued equity markets, (ii) Rotating into high quality income assets, and (iii) Risk managing via hedges, cash and cash-like assets are strategies that can help navigate a difficult near-term outlook.

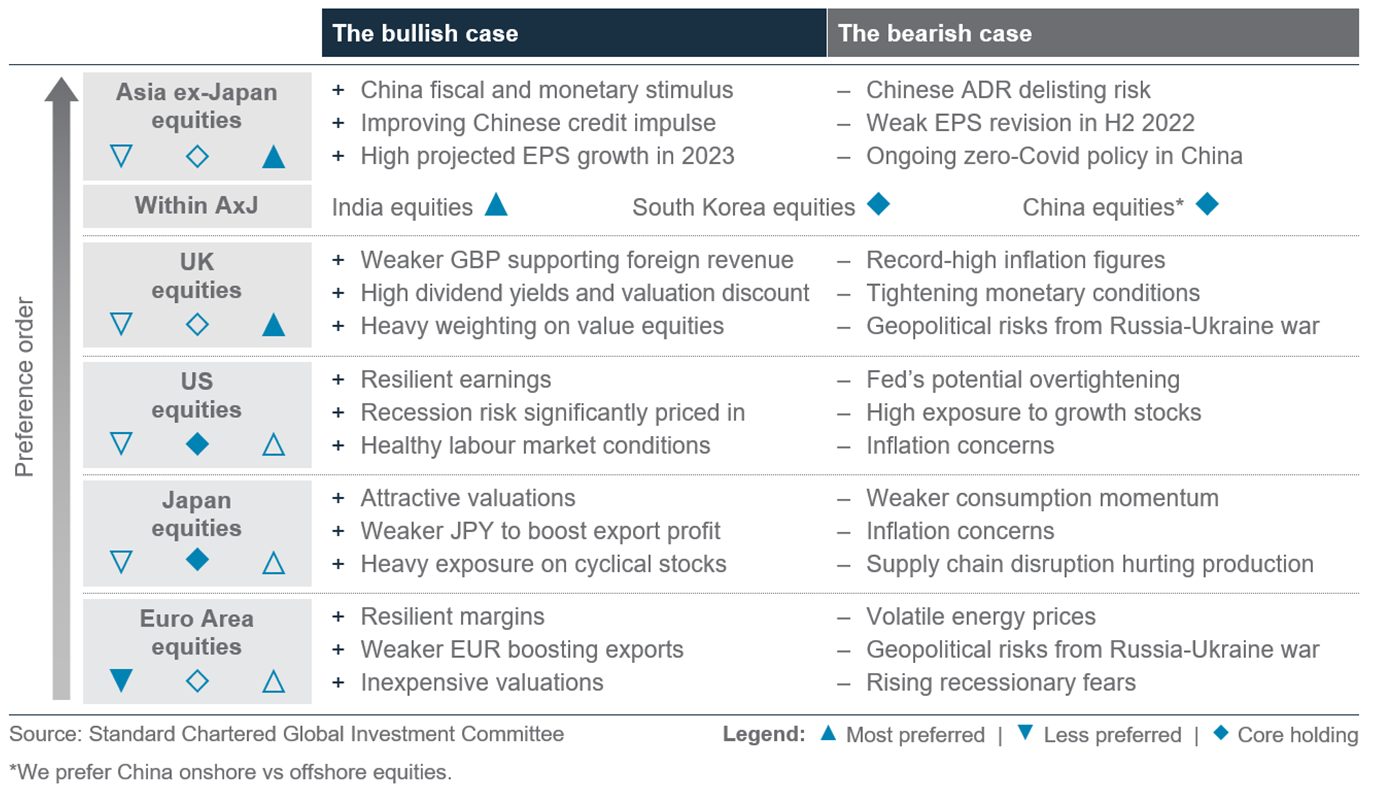

Within equities, we retain our regional preferences for Asia ex-Japan and the UK, but adopt a more defensive sector tilt. We expect the USD to go higher in the coming months.

Review our income basket which yields more than 7%

Is cash king once again?

Lessons from the former Fed Chair Volcker

Strategy

Investment strategy and key themes

|

|

||||

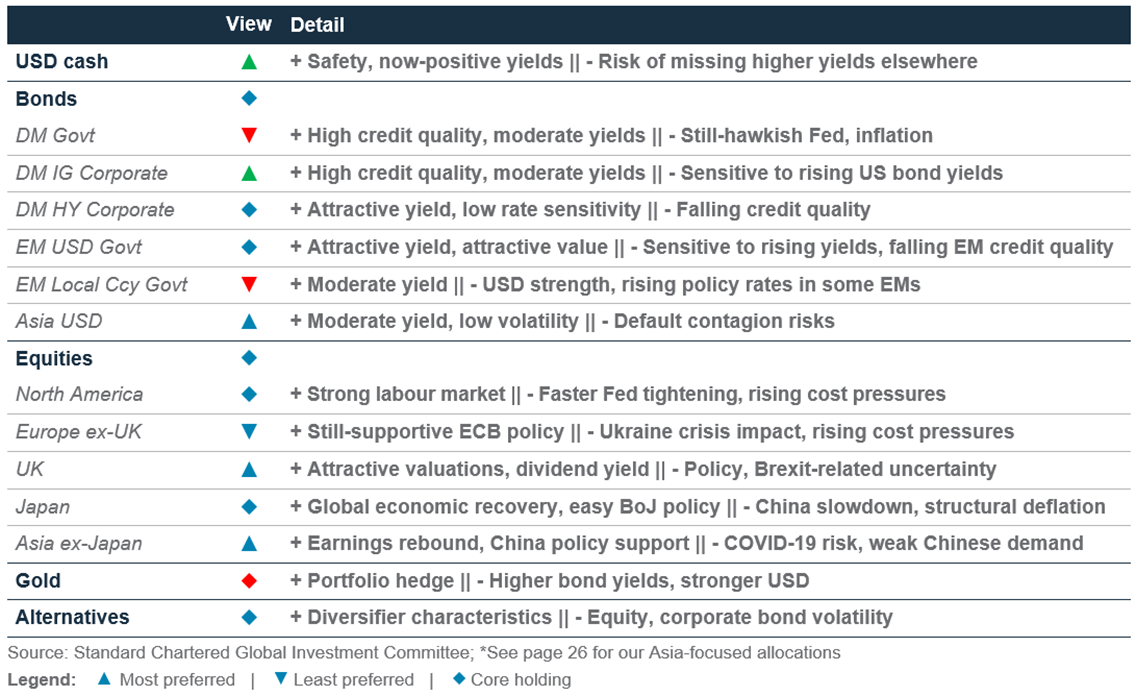

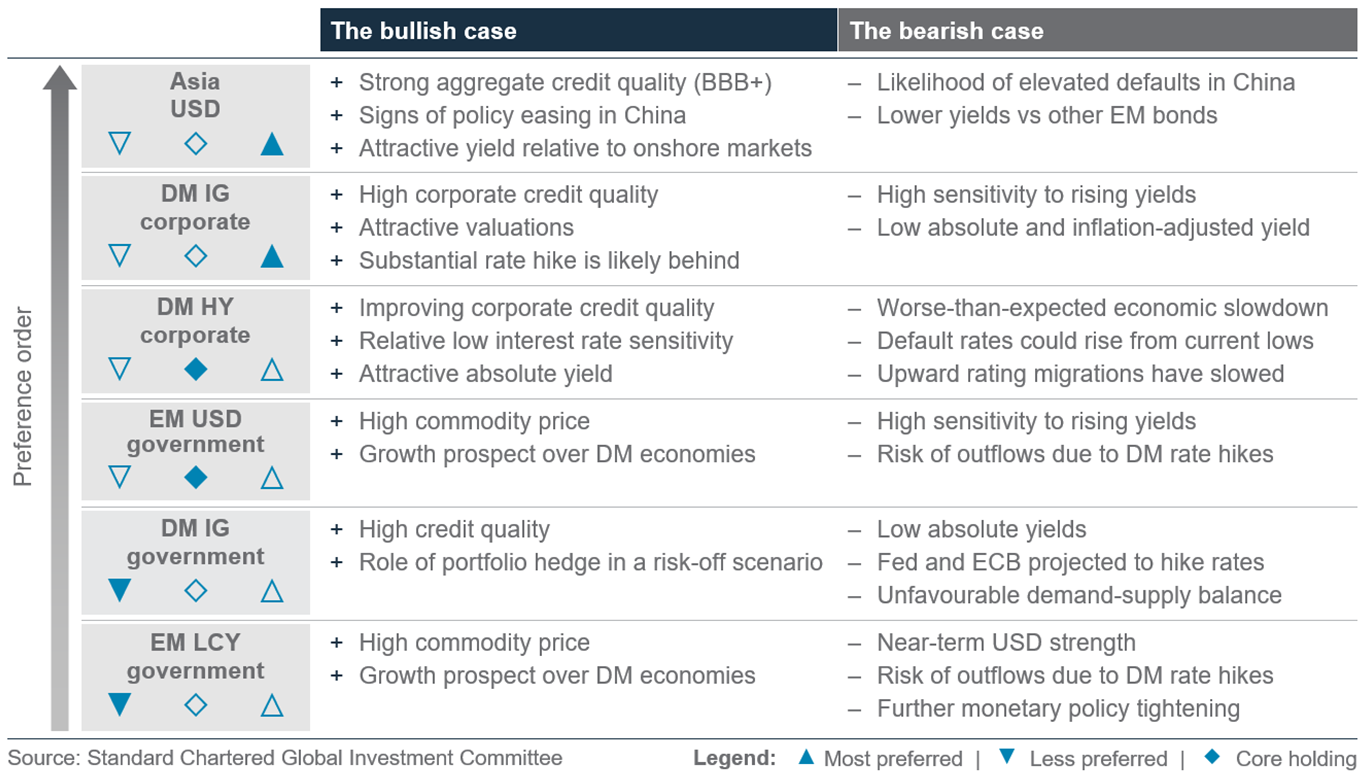

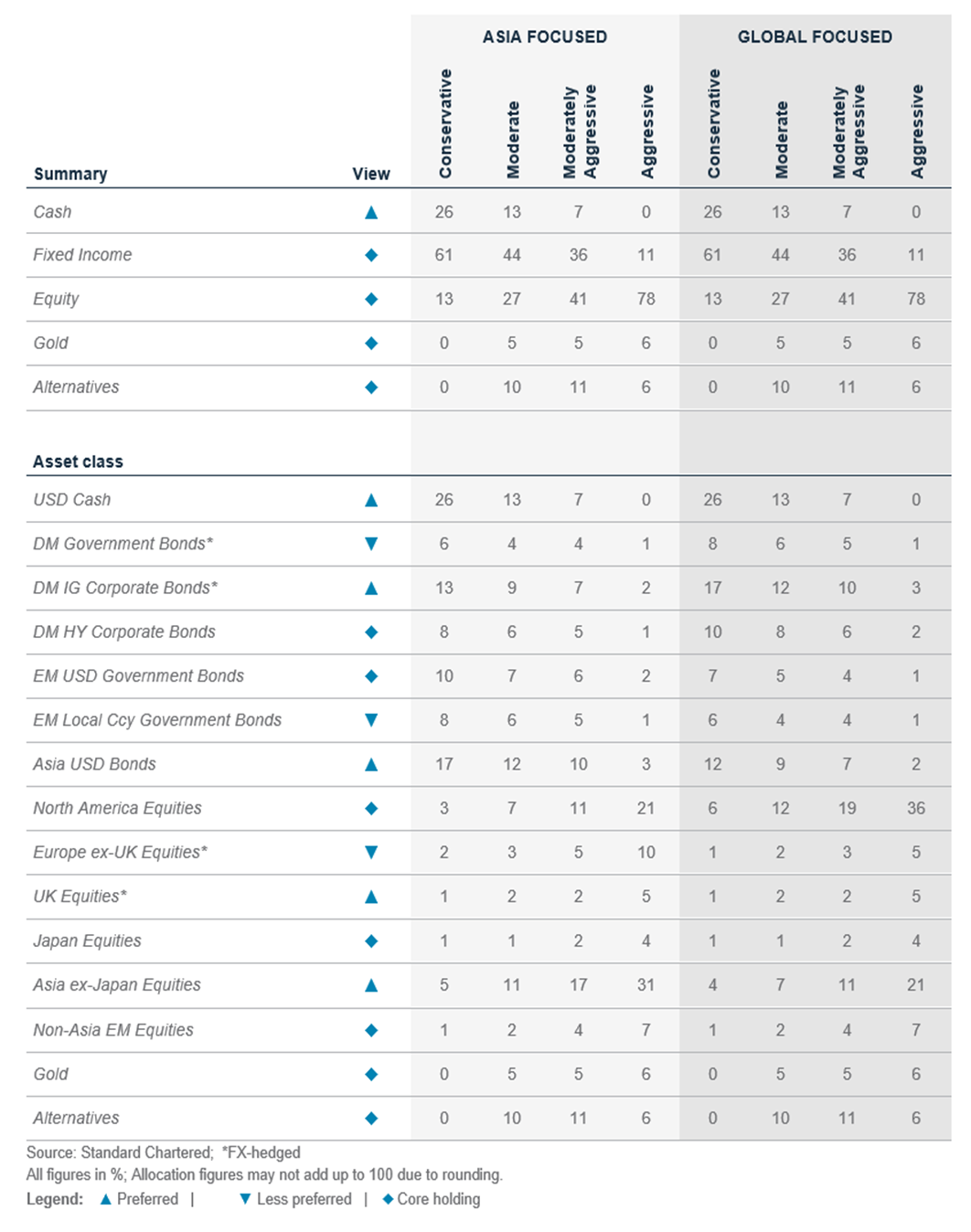

Our preferences (12-month view)

Foundation allocation preferences

- Prefer Cash

- In equities: Asia ex-Japan and the UK

- In bonds: DM IG corporate, Asia USD

Sector preferences

- US: Energy, Healthcare

- Europe: Energy, Financials

- China: Energy

Longer-term themes

- The Winds of Climate Change

- Clean Technology, Electric Vehicles, Water Scarcity, Infrastructure/ Green Capex

- China’s ‘Common Prosperity’

- Hard Tech/Semiconductor, Renewables

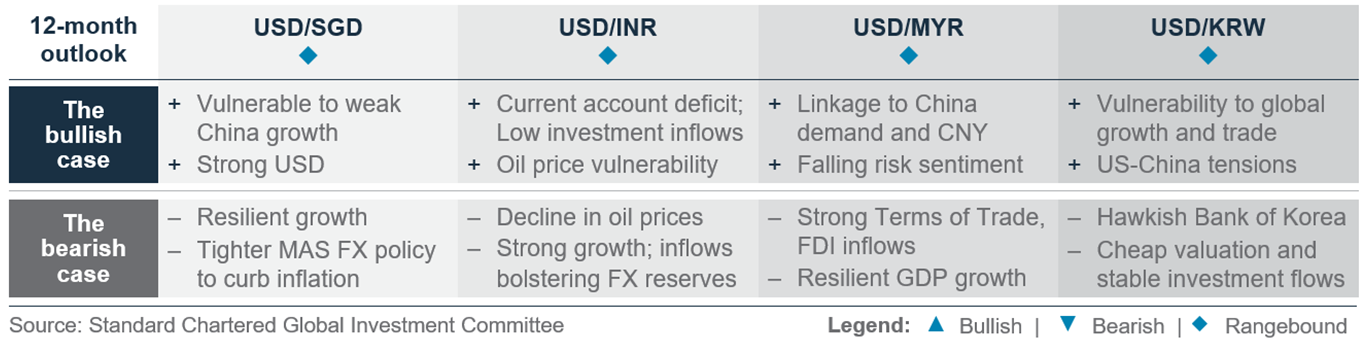

Our 3-month FX views

Bullish USD; bearish EUR, GBP, JPY and CNH

Navigating a difficult near-term outlook

- Fighting inflation remains central banks’ top priority. This makes a recession and further near-term downside in equities more likely, with the debate shifting to whether such a recession is going to be shallow (which is likely priced in) or deep.

- We believe (i) Rebalancing into investment grade corporate bonds and some deeply undervalued equity markets, (ii) Rotating into high quality income assets, and (iii) Risk managing via hedges, cash and cash-like assets are strategies that can help navigate a difficult near-term outlook.

- Within equities, we retain our regional preferences for Asia ex-Japan and the UK, but adopt a more defensive sector tilt. We expect USD to go higher by year end.

From a Fed pivot to a Fed adjustment

Over the past quarter, the Fed has continued to make it clear that expectations of it pivoting towards supporting growth were premature. After another 75bps rate hike, Fed Chair Powell said combating inflation remains the central bank’s priority, even if it proved painful at times and came at the expense of growth.

We believe investors should focus on a 3R strategy – (i) Rebalance into investment grade corporate bonds and deeply undervalued equity markets, (ii) Rotate into high quality income assets and (iii) Risk Manage via hedges, cash and cash-like assets.

Rebalance and diversify

The Fed’s approach raises the risk of further near-term downside in equities. While we see a high likelihood of an economic recession in the US, whether such a recession will be relatively mild or deep is key. History shows us that peak-to-trough drawdowns for the S&P500, for instance, have been as small as 20% (similar to this year’s move) in milder recessions like 1990 or as large as over 50% in 2008, an unusually deep recession. Fed policy, which remains aggressively focused on responding to inflation for now, risks tightening policy to the point where a recession is no longer shallow. Given these near-term uncertainties, it is important to rebalance into attractively valued assets, quality balance sheets, that are best able to ride out the volatility ahead.

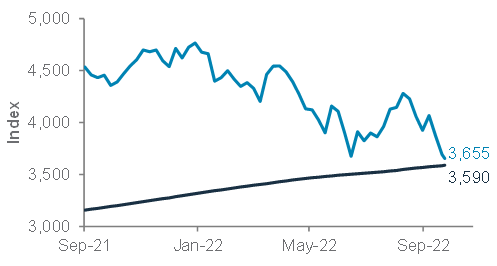

- Equities: We retain equities as a core holding on a longer 12-month horizon. On a shorter 3-month basis, we caution that equities may take another leg lower as markets price a bigger downgrade to earnings if the Fed shows no signs of easing the pressure, especially if the S&P500 decisively breaks below the key support area around June lows and the 200-Week Moving Average (3590-3637).

Fig.1 An S&P500 break below its key support zone could be significant from a technical standpoint

S&P500 Index and 200-week moving average

Regionally, we continue to prefer Asia ex-Japan. The strong USD undoubtedly remains a headwind for Asian, and indeed most EM, equity markets. However, we believe that is mitigated because of (i) Asian equities’ relatively inexpensive starting point, (ii) China’s growth-supportive policy, and (iii) our view that USD strength is a 3- rather than 12-month risk. Within Asia, though, we do reduce our risk slightly, reducing China to a core holding while retaining India as preferred.

UK equities remain our second preferred region based on (i) the region’s attractive dividend yield and (ii) large-cap firms’ largely global earnings. However, we now add an FX hedge to our UK and Euro area equities exposure, which should help both mitigate the risk of further FX volatility and ensure exposure to the benefits of a weaker GBP when translating large-cap firms’ international earnings.

- Bonds: Developed Market (DM) Investment Grade (IG) and Asia USD bonds remain our preferred exposures within bonds given (i) attractive yields, (ii) Asia USD’s predominantly IG credit quality (and, within that, our preference now for IG over High Yield [HY]), and (iii) the likelihood that IG bonds will benefit from lower yields at some point when markets start to worry about growth.

Recover using high quality income

Portfolios need close attention given the macroeconomic backdrop. Investors should position their portfolios to reflect the challenging conditions and ensure they are best positioned to recover any losses. Focusing on taking advantage of today’s attractive yields, while retaining a tilt to higher quality assets, is a good way to implement this.

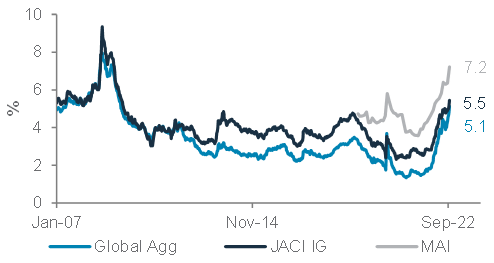

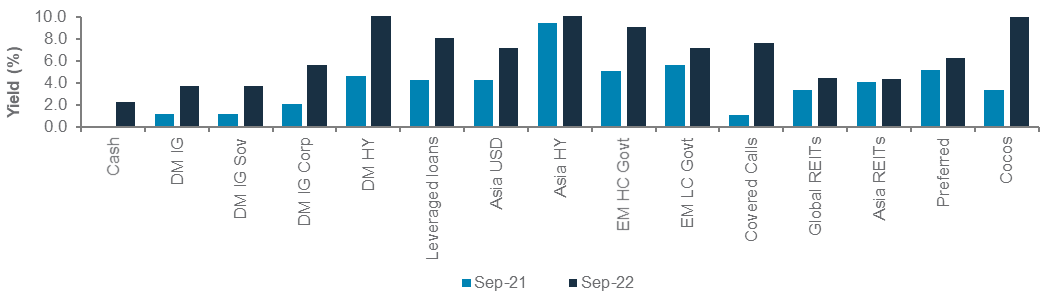

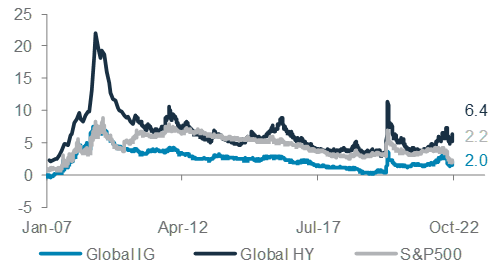

Today’s higher yields offer investors an opportunity to lock in yields that are approaching pre-2008 levels – c.5% for DM IG corporate bonds and over 7% now on our multi-asset income strategy, for example.

Our preference is to focus on the following:

- Multi-asset income strategies remain one way of taking advantage of higher yields, while maintaining a diversified allocation. While this does not mean immunity from volatility in risk assets, the yield should dampen the volatility to a significant extent.

Fig.2 Investment Grade bond yields now approaching pre-Global Financial Crisis levels

Global IG corporate, Asia USD bonds (yield-to-worst) and Multi-Asset Income yield (%)

- Within bonds, we prefer taking advantage of today’s yields via corporate credit rather than government bonds given (i) the risk of rising yields (falling government bond prices) and (ii) the fact that corporate bonds’ yield premia offer some buffer against rising yields, while offering higher income.

- Within equities, we prefer taking advantage of the attractive dividend yields available through a basket of consistently high dividend paying equities.

Risk-manage with hedges

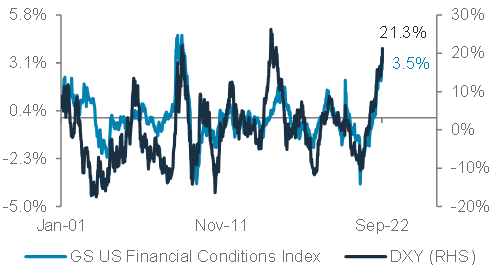

Managing risk is extremely important in the current environment. We increase our cash allocation, with its now-positive yield (a characteristic less commonly seen after 2008) making it a more attractive volatility hedge. See page 10 for a more detailed discussion of the costs and benefits of cash.

Fig.3 US financial conditions have to likely stop tightening for the USD to turn

USD Index (DXY) vs US financials conditions index (%y/y)

The USD could also provide a hedge against a still-hawkish Fed. On a shorter 1-3 month horizon, USD strength looks set to continue, with the Fed clearly intent on tightening financial conditions further. This creates opportunities such as using the EUR as a short-term funding currency (we expect EUR/USD to test 0.93-0.94).

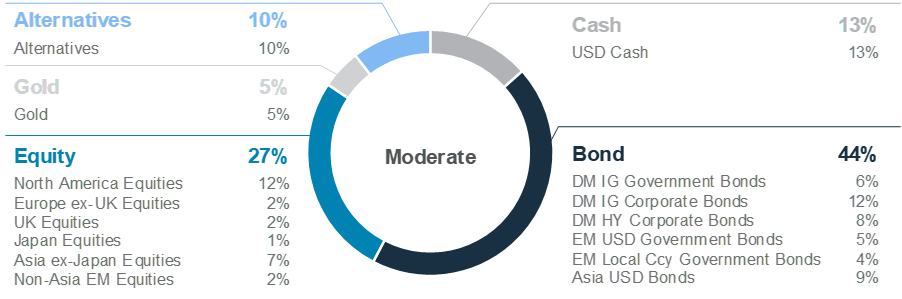

Foundation: Tactical asset allocation

Global* allocation model for a moderate risk profile

Multi-asset income allocation model for a moderate risk profile

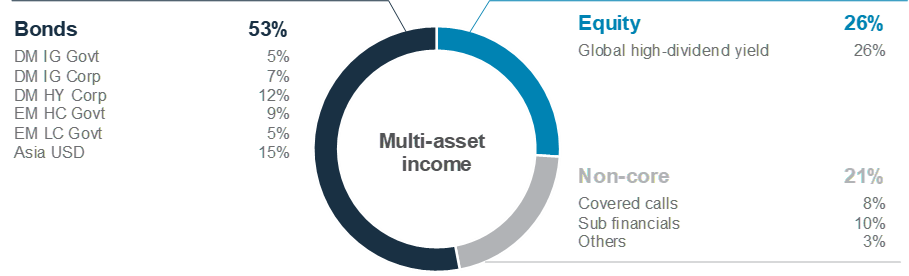

Multi-asset income at a glance

|

|

||||

Key themes

Our multi-asset income allocation now yields over 7% as central banks continue to hike rates to bring inflation down globally. Their hawkish stance has led to lower asset prices and higher bond yields this year. Today, over 59% of bonds offer in excess of 4% yields vs 3% a year ago, offering income investors a richer picking of income assets.

We continue to increase our allocation to fixed income, given the surge in government bond yields and wider credit spreads across bond asset classes this month. We have added to DM IG bonds, yielding 3.7%, which look attractive compared with cash. We also added to Asia USD bonds this month, given the high yield on offer and because the asset class is dominated by IG issuers.

Leverage loans should continue to benefit from rate hikes and upside risks to inflation. Subordinated financials bonds have sold off in sympathy as rates soared in Europe. Yields look attractive and the asset class is dominated by European banks, our preferred sector in Europe. We continue to expect dividend equities to outperform global equities as a higher dividend yield offers some protection against market volatility.

Key chart

We remain bullish on income strategies given more attractive yields on offer and its ability to cushion against market volatility

Fig. 4 Higher yields could offer some protection against further market volatility

Starting yield to worst (%) of DM HY vs 12m returns (%)

Fig. 5 Yields have risen across the income universe significantly since a year ago

Yield to worst/dividend yield (%)

Fixed income as an improving pillar for income generation

We have added to fixed income assets within our multi-asset income allocation. We see rising value in bonds, with yields in DM IG bonds over 3.7%, the highest since 2010. US real yields have risen sharply to almost 1%, one of the sharpest increases in recent history. While the Fed is likely to remain hawkish, the strong convergence of market expectations to the Fed’s, suggests the worst of bond yield increase is likely behind us.

We like bonds with a high-quality tilt, adding to DM IG bonds and Asia USD bonds (85% IG issuers) this month. Asia USD bonds look attractive, given their high yields on offer, wider credit premia and relative lower volatility compared with US government bonds. We expect China to continue easing its monetary policy, providing a more supportive macro backdrop relative to the US and Europe, which are tightening policies.

We continue to have a sizeable holding to Floating Rate Notes (FRNs), which tend to benefit from higher rates. Default rates continue to look benign. Additionally, FRNs historically have performed well in periods of high inflation and demonstrate a lower sensitivity to higher interest rates.

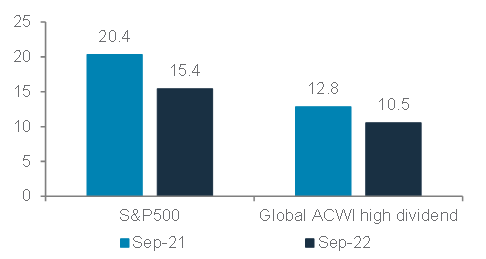

Fig.6 Valuations seem more favourable for dividend equities

12m forward P/E ratio

Equity income is still a necessity

We have pared back slightly on our allocation to dividend equities given rising recession risks and more attractive yields in fixed income assets.

While dividend equities have historically outperformed during high-inflation regimes and when global growth is slowing, there exists the potential for large drawdowns in the event of a recession. Hence, we used this opportunity to pare back on dividend equity to benchmark allocation, tactically.

Over the long term, dividend equities still offer a greater probability of delivering positive inflation-adjusted returns compared with bonds or cash. Unlike the income in bonds or cash, companies have the ability to raise dividend income as profitability grows, offering a decent hedge against inflation.

Supplement total returns using non-core allocations

Subordinated financials bonds have sold off in sympathy as rates soared in Europe. Yields look attractive from a sector dominated by European banks, a sector we are Overweight from an equity market perspective. We have added to this asset class given the 11% yield on offer and our expectations that write-down/coupon cancellation risks are low as capitalisation for most European banks remains robust.

Other equity-like income assets such as REITs and covered calls have traditionally been resilient in inflationary environments. We also view these instruments as attractive for income and their capital appreciation potential.

Opportunities in higher yields are attractive

Risk assets and income strategies have had a very difficult start to the year against the backdrop of elevated inflation, moderating growth and rising risk of a recession. Still, our multi-asset income allocation returned -17% since publishing our 2022 Outlook, outperforming a balanced allocation by c.1% as investors sought real cash flow. Looking ahead, we believe that a diversified income strategy will remain attractive as a core component of a diversified investment allocation.

The opportunities arising from income strategies are looking attractive after this year’s rise in interest rates, and our multi-asset income allocation currently offers a yield of 7.3%. While there might be further downside from the impact of higher yields, we believe that higher yields can cushion market volatility and any decline in prices, and it is opportune for investors to consider layering into higher income assets.

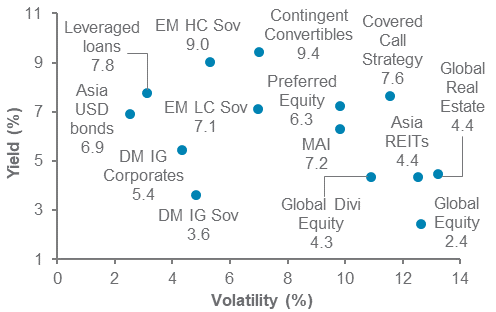

Fig. 7 Risk management will become increasingly important in a volatile environment

Yield/volatility of returns trade off across income assets

Perspectives on key client questions

|

|

||||

What can investors learn from Volcker’s experience?

We have seen a wave of central banks turning more hawkish over the past month. From an unprecedented 100bps rate hike by Sweden’s Riksbank to the third consecutive 75bps hike by the Fed, there is even greater willingness to tighten policy if inflation remains high, almost regardless, it seems, of the implications for global growth. US real rates (net of inflation) soared to almost 1%, clearly a major headwind for valuations across risk assets. Against this backdrop, equities, bonds and commodities sold off in September, with the USD soaring to a new 20-year high.

This current inflationary environment is undoubtedly new for most investors. Past decades of low interest rates and accommodative policies have reinforced investors’ expectations of a “central bank put” whenever growth faltered or markets slumped. Instead of focusing on recent past, investors may want to study the last high inflationary experience several decades ago, even though inflation today is much lower than what the world experienced in the 1980s. Here, we look at former Fed Chair Paul Volcker’s experience to see what lessons investors can draw to address the challenges.

Lesson 1: Policy easing before inflation is reduced will only prolong the pain

At both Jackson Hole and the Fed’s September meeting, Chair Powell declared the Fed “must keep at it until the job is done.” Fed watchers will point out that Volcker’s 2018 memoir, entitled “Keeping At It,” also uses the same phrase in relation to the Fed policy. Powell’s allusion to Volcker is no coincidence and should be taken as an indication that the Fed intends to take a page from Volcker’s playbook to rein in inflation. In his book “Changing Fortunes,” Volcker provides context to the economic conditions at that time. As the Fed restricted money supply and interest rates rose, the US economy slipped into a recession, the first of two that occurred during that time. Volcker eventually relented to intense public pressure to ease money supply.

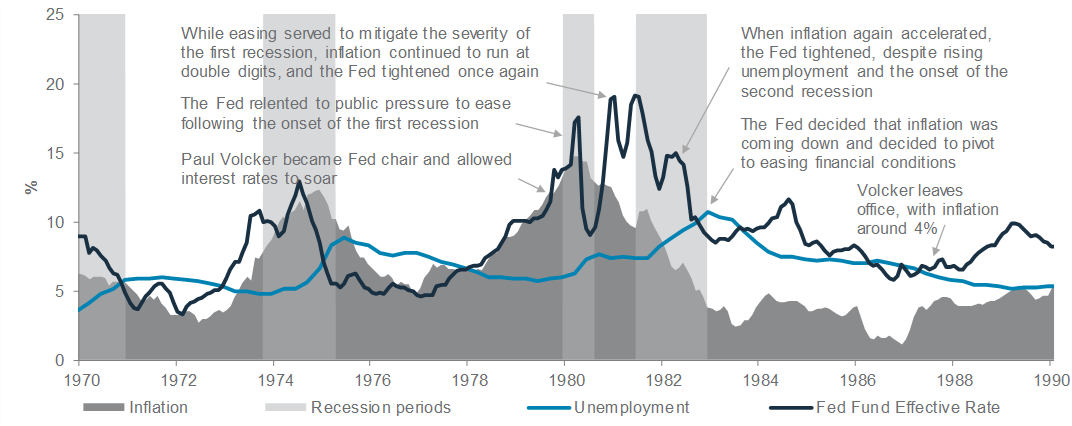

Fig. 8 Fed’s premature easing and subsequent tightening led to a deeper and longer recession in July 1981

While this resulted in a short-lived recession that lasted only four months, inflation continued to run at double-digits. This led the Fed to tighten money supply yet again, resulting in a deeper and longer recession that started in July 1981.

The main takeaway is that prematurely easing at the onset of a recession will only prolong the economic pain. Investors should be mindful that the Fed today, as it was in the 1980s, is serious about curbing inflation (even though it is significantly lower than in the 1980s) and is willing to sacrifice growth and accept higher unemployment to achieve meaningful progress towards the 2% inflation target.

Lesson 2: Inflation can be much stickier than expected

History suggests that inflation can be much stickier than expected. In the US, dating back to 1914, once inflation rises above 5%, it takes, on average, 52 months for it to drop below 2%. When Volcker was appointed the Fed chair in July 1979, inflation was running above 11% and the Fed Fund Effective Rate was at 10%. It took the Fed more than three years and a peak interest rate of 20% to declare the fight against inflation was over, and another 40 months to bring inflation below 2%.

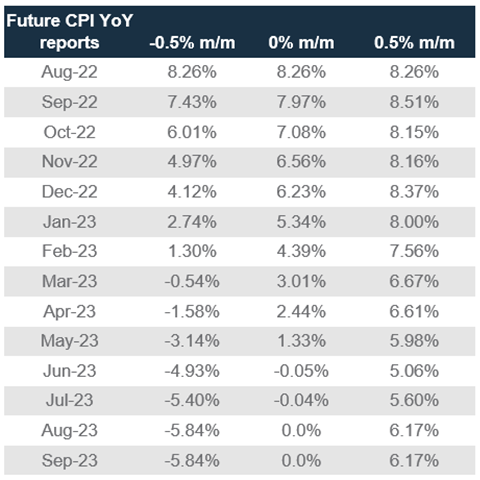

Of course, Inflation today is not as rampant as it was in the 1970s, and there are signs that headline inflation may have also peaked. However, even if inflation runs at a constant 0% m/m change from August levels, it will still require another nine months for inflation to fall below 2%.

Fig. 9 Headline inflation will take 9 months to fall below 2%, even if inflation runs at a constant 0% MoM

Potential y/y headline CPI inflation based on m/m CPI changes in the coming months

Lesson 3: Hope for the best but be prepared for the worst

The economic impact of monetary policies typically occurs with a lag. As interest rates rise, borrowing demand falls and spending declines. Unemployment then begins to increase, which reinforces the slowdown in consumer spending and lending by banks.

Meanwhile, as it takes time for the downturn to appear in the data, policymakers respond with a lag and the results of their response likewise come with a lag.

Investors can draw two useful conclusions from this description of delayed self-reinforcing feedback between economic conditions and policy response.

First, benign economic conditions are not a sure indication that the Fed is able to pull off a soft landing, especially if inflation remains persistently elevated. Since 1960, unemployment has risen, on average, six months before the official start of a recession and peaked only seven months after the end of the recession, when interest rates have already started to decline. Trailing 12-month EPS likewise only hits the bottom eight months after the end of a recession.

Second, while the Fed is targeting a relatively soft landing for the economy, based on its most recent projections (with median estimates of US unemployment expected to rise to c.4.4% by end-2024, from the current 3.6%), the probability of achieving such a soft landing appears remote, at least based on history. Once the US unemployment rate increases beyond a certain threshold, it tends to keep rising, as the impact from tighter monetary policies tends to occur with long, variable lags. Calculations from BCA Research have shown that through the past 75 years, whenever US unemployment has risen by 0.6 percentage points, it has then gone on to increase by at least 2.1 percentage points from the trough.

While the US labour market remains robust, with the unemployment rate close to 50-year lows, investors should be prepared that economic conditions are likely to deteriorate considerably over the coming months until central banks’ fight against inflation is over.

Short-term pain, long-term gain

In a year when most asset classes are nursing double-digit losses, it is hard to see the light at the end of the tunnel. But investors should draw on the lessons of Volcker’s experience and recognise that temporary pain today will pave way for a better tomorrow. The good news is that inflation today remains well below that in the 1980s, which means the Fed would have to tighten far less than it did four decades ago. Inflation will eventually subside, just as it did in the 1980s, and the market will recover, just as it did following the Fed pivot in 1982, when US stocks embarked on a nearly two decades-long bull run.

In the meantime, to ride the ongoing market volatility until we see a significant Fed policy pivot, we believe investors will be best served by reducing their overall risk in their portfolio over the next 12 months and maintaining a broadly diversified basket of cash, stocks, bonds, gold and alternative assets, with selective preferences for some assets and markets as described in our 3R Strategy in page 3.

GIC perspectives – The cash debate

|

Is cash king once again?

Cash can mean different things to different people. Most of us would associate its yield with that on a deposit, but this only partly captures the asset class. Many investors consider yields up to 12 months in maturity as a proxy for cash given its yield tends to be closely associated with policy rates. Several factors, however, are common across various approaches to ‘cash’ – perceived safety of the nominal value of principal, easy access to liquidity and a lower yield than on most riskier asset classes (in return for these attributes).

The case for cash today

In today’s investment environment, a case can be made for a greater-than-usual allocation to cash (see page 26 for how much this specifically entails for different risk profiles):

- Yields are no longer zero. The yield on cash is key because it is often viewed as the threshold that other asset classes ‘have to beat’. If the cash yield is available with (perceived) certainty, the expected return on any other asset class has to be higher for an investor to take on the additional risks associated with that asset class.

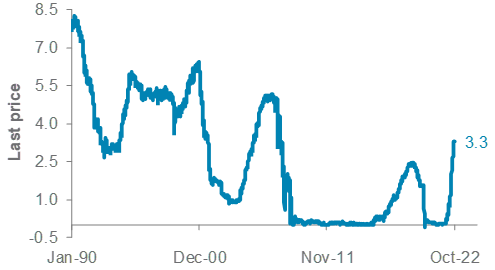

Fig.10 Cash yields have returned to levels last seen prior to the 2008-09 crisis

The 3m USD Treasury bill yield

Since 2008-09, this cash threshold was largely zero, which meant there was little reason to consider a significant allocation to cash for purely investment reasons (the TINA or ‘There Is No Alternative’ argument for riskier assets like equities). Today, however, the 3-month USD yield is just above 3.5% and could rise further until the Fed hiking cycle peaks. This significantly raises the threshold for other asset classes and starts to make a more attractive case for cash relative to other major asset classes.

- Safe haven appeal: In markets like today, cash can offer a safe-haven amid concerns that the drawdowns in equities and bonds are not yet complete – especially if the S&P500 takes another leg lower. This argument, of course, would hold regardless of the yield on cash.

The challenges of cash

Given the advantages of holding cash, why not hold much more? We see at least two reasons:

- Riskier asset classes usually pay a premium over cash over the long term: While it may not feel like it this year, over most longer periods, riskier asset classes do indeed pay a premium over cash. This premium can be negative during periods like today when the market is adjusting to a higher yield on cash, but these have been transitory and are usually short-lived.

Fig. 11 Higher cash yields have narrowed the yield premium offered by riskier asset classes

Asset class yield premiums over the 3m USD Treasury bill

- Cash can be detrimental to maintaining real purchasing power: Following on from the first point, the yield on cash may be positive in nominal terms, but it remains very negative on real, or inflation-adjusted, terms. Riskier asset classes can offer a good chance of beating inflation over longer horizons, but staying too long in cash reduces those chances significantly.

Today, we see a case for holding more cash than usual because of a heightened equities and bonds drawdown risk and because cash now pays a positive nominal yield. However, we remain mindful of the longer-term drawbacks of holding cash (even today, global IG corporate bonds yield around 5% vs c.3.5% on cash), which is why our preference is accompanied by an active willingness to redeploy into riskier asset classes at the soonest available opportunity.

Our thematic ideas

|

The winds of climate change

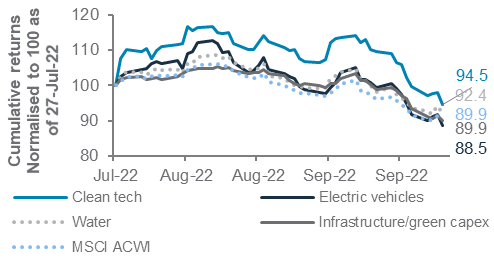

While Winds of Climate Change has not been spared the recent downturn in global equities, all sub-themes besides Electric Vehicles have managed to outperform the MSCI ACWI index since the announcement of the US Inflation Reduction Act (IRA) in July. More notably, we see Clean Tech, arguably the largest beneficiary from the Inflation Reduction Act, outperforming the MSCI ACWI by 4.5%.

Fig. 12 Clean Tech has outperformed global equities since the announcement of the US IRA

Cumulative returns of Winds of Climate Change themes since 27 July 2022

In the near term, while higher rates and elevated inflation remain key market narratives, the prospect of increased investments in clean energy is expected to help preserve the sub-theme’s outperformance against global equities. In addition, elevated energy prices amid the escalating Russia-Ukraine conflict would also help reduce the green premium and add to the investment incentives in the sector. A key risk is however seen in the growing likelihood of a recession, which could spur outflows into defensive sectors like utilities.

Beyond the near-term risk of a recession, structural drivers remain intact for the themes. Green capex continues to be a multi-year secular theme, which will drive the next wave of infrastructure investments as the world decarbonises. Penetration rate for electric vehicles continue to grow, with strong adoption in China and Europe, while US manufacturers will stand to benefit from the IRA.

Embracing a digital future

As we expect the Fed’s commitment to tighten monetary policies to put further upward pressure on interest rates, which will in turn weigh on valuations, we have decided to remove Cybersecurity from our preferred view.

However, we continue to see constructive long-term structural drivers in this space and will look to revisit key areas of the theme at a later date.

China’s ‘Common Prosperity’

While dismal economic conditions and downbeat sentiments have weighed on China equities and led China renewables to erase the strong gains made in Q2 22, we continue to find reasons to be optimistic on China’s renewables, with the New Energy Vehicles (NEV) sector, in particular, being a rare bright spot in the Chinese economy.

Our continued optimism stems from three factors. First, fiscal and monetary policies remain supportive. The NEV sector, which is a major component in the China renewables benchmark, stands to benefit alongside the broader auto industry from the ongoing policy stimulus, while an extension in purchase tax exemption to the end of 2023 should serve to maintain the economic incentive over ICEVs.

Second, fundamental progress continues to be made in the NEV sector. NEV sales have been robust, with August sales growing by 107.5% y/y and penetration rates rising to almost 28%. Given the current high order backlogs and thin inventories, the momentum in NEV sales is expected to continue for the remainder of 2022.

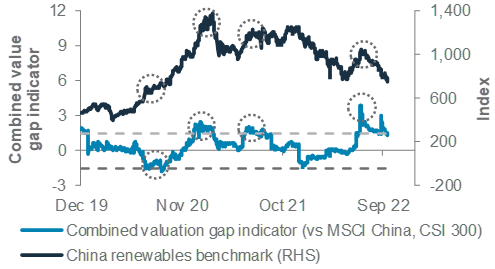

Third, valuations have come down and investor interest is returning. Our Combined Valuation Gap Indicator has fallen from a considerably overvalued territory to a historically neutral range, while earnings revisions have started to trend higher. ETF inflows have also returned in recent weeks.

Fig. 13 Relative valuation of China renewables has fallen from overvalued territory to a more neutral range

Combined Valuation Gap Indicator with +/- 1.5 thresholds*

Together, these factors suggest that while macro headwinds continue to be the dominant influence on China equities, strong fundamentals, supportive policies and improving investor sentiment mean that China renewables is well positioned to withstand the headwinds buffeting China equities.

Macro overview – at a glance

|

|

||||

Key themes

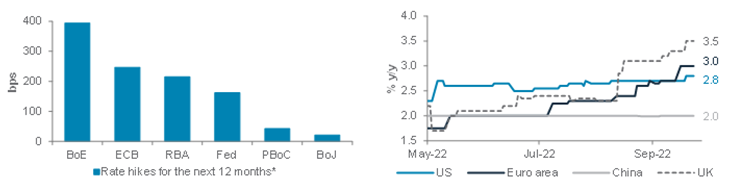

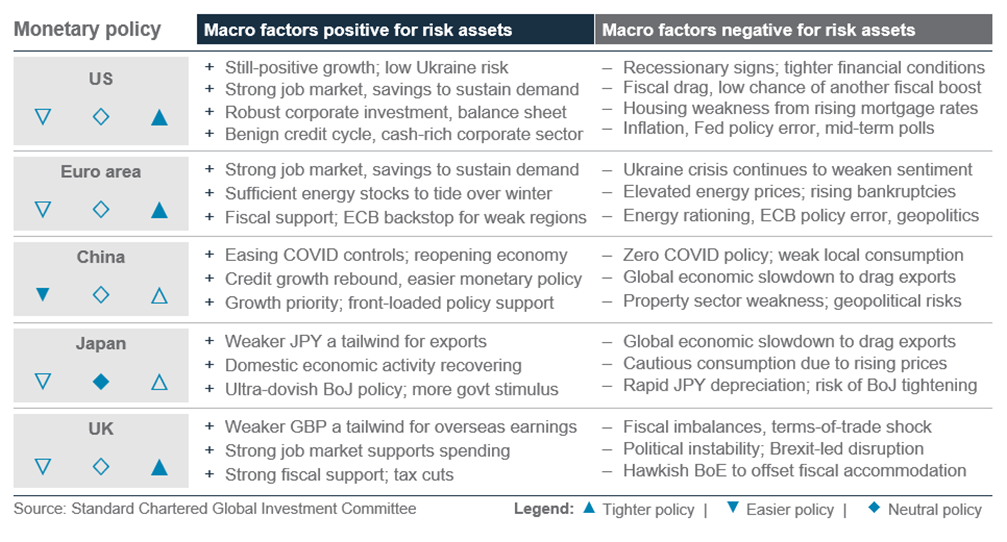

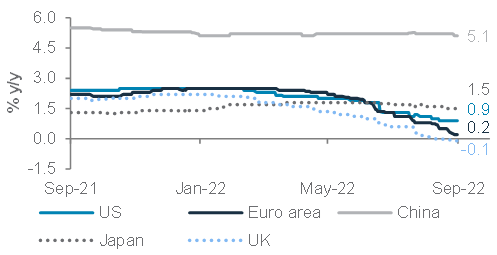

Global central banks have turned more hawkish over the past month, clearly signalling they are willing to sacrifice growth to sustainably bring down inflation from multi-decade highs. Given this, we see more front-loaded rate hikes in the coming months – we now expect the Fed funds target rate at 4.5% (from today’s 3.25%) and the ECB’s benchmark deposit rate in the 2.0-2.25% range (from 0.75%) by June 2023. Despite the rate hikes, we agree with the consensus that inflation is likely to stay above the central banks’ 2% target in the US and Europe through next year. The combination of high near-term inflation and hawkish central banks has raised the probability of US and Euro area recessions in the next 12 months to 75% and 80%, respectively.

China’s economic outlook sharply contrasts with that of the Developed Markets, in our view, primarily because inflation remains under control. We expect subdued inflation to enable the authorities to accelerate fiscal and monetary policy stimulus to revive the economy once the Communist Party Congress is over in October (which is slated to extend President Xi Jinping’s tenure to a rare third five-year term). China’s zero-COVID policy is also likely to be gradually relaxed after the Congress, although a normalisation of activity is more likely after the end of winter in Q1 2023. Based on this roadmap, we expect China’s growth to rebound close to 5% next year. Increasing geopolitical tensions with the US and a persistent slump in the property market, despite ongoing measures to stabilise the sector, remain key risks to this constructive outlook for China.

Key chart

The BoE and ECB are expected to hike rates more than the Fed as European inflation is expected to stay higher than in the US in 2023

Fig. 14 Most global central banks are likely to stay hawkish amid high near-term inflation

Market estimates of rate hikes for the next 12 months; consensus CPI estimates for Q4 2023

Outlook for US, Europe diverges from China

The global outlook has deteriorated in the past few months as major central banks turned more aggressive to reduce inflation at multi-decade highs. However, China’s economy appears to have bottomed in Q2, with economic activity picking up in recent months on sustained fiscal and monetary policy easing. Here, we review key indicators to assess the outlook for the world’s three largest economies.

US recession monitor: Several indicators in our US monitor have triggered recession warnings in recent months. Initial warnings came from slumping consumer confidence in H1, as soaring inflation hurt disposable incomes, and from an inverted government bond yield curve (the 10-year yield has consistently remained below the 2-year yield since July). Over the past month, more indicators have signalled a heightened risk of a recession: a renewed bear market in US equities; a fall in the new orders to inventories ratio below 1 (as companies, facing excessive inventory, cut new orders); and annual growth in Conference Board’s US Leading Indicator turning negative. The latest warning came from the Fed’s 75bps rate hike in September, which took the benchmark rate (3.25%) above the Fed’s so-called neutral rate of 2.5%, turning monetary policy restrictive. Further rate hikes in the coming months are likely to also invert the 10-year vs 3-month yield curve (historically seen as a timelier indicator of a coming recession) as bond investors worry that Fed policy has tightened enough to hurt growth in the coming years. Meanwhile, the rising yield premium of corporate bonds over US government bonds continues to tighten financial conditions, although the premium remains below the threshold that normally signals an imminent recession.

Against this growing number of recession signals, the US job market remains robust, with job openings near record highs and the unemployment rate, at 3.7%, still below the Fed’s 4% long-term target. The strong job market, along with nearly USD 2trn of household savings, continues to fuel US consumption, enabling the economy to offset the impact of the tightening fiscal and monetary policy. This explains why the Fed is determined to cool the job market in a bid to suppress wages, shelter costs (which account for a third of US inflation) and overall consumption. We believe the Fed’s initial target is

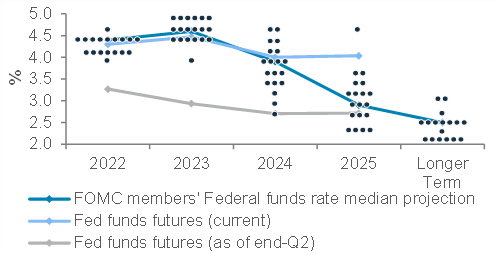

Fig. 15 Fed has caught up with the markets on rates

Fed and money market rate expectations until 2025*

to reduce the number of job openings and then accept a rise in the unemployment rate above its 4% target. Thus, the key metrics to watch in the coming months will be the number of people filing for unemployment relief (initial jobless claims) and the overall jobless rate. Business confidence indicators (PMIs) remain healthy in the US, despite falling from record highs this year, but any sharp downturn in the indices, along with any sharp rise in the jobless rate or fall in inflation, would raise the prospects of a pause in the Fed’s rate hiking cycle.

Stagflation pressures grow in Europe: Stagflation is technically defined as rising inflation, stagnating output and rising unemployment. Europe, being on the frontline of the energy crisis triggered by the Ukraine war, has already seen soaring inflation. While authorities are trying to shield consumers and industries from higher energy prices, the negative market reaction to the UK’s fiscal easing measures is likely to constrain fiscal policy. The consensus now expects Euro area economic activity to start contracting from Q4, a view that we align with. As the economy contracts, we expect the unemployment rate, which fell to a record low of 6.6% in July, to start rising. However, high and still rising core inflation means the ECB is likely to continue raising rates in the coming months, until inflation shows signs of sustainably falling m/m for a few months. We expect the ECB to raise its deposit rate to the 2.0-2.25% range by June 2023, below money market estimates of 3%, as we expect policymakers to pause in H1 2023 as the economy enters a recession.

China continues to recover: China’s economic activity has rebounded in recent months from Q2’s contraction on easier fiscal and monetary policies. As credit growth turned positive, industrial production and retail sales growth accelerated above 4% and 5%, respectively, in August. Fixed asset investment continued to expand, despite a contraction in property investments, as authorities brought forward spending on projects. We expect this recovery to continue in the coming quarters as below-target inflation enables authorities to ease policies further once the Communist Party Congress is over in October. COVID-19 lockdowns and rising tensions with the US remain key risks, but we expect authorities to ease restrictions significantly after winter, enabling growth to recover towards their 5% target next year.

Fig. 16 Biggest cuts seen in Europe’s growth estimates

Consensus estimates of 2023 growth for major economies

Source: Bloomberg, Standard Chartered; *the dots represent projections of the Fed funds rate by individual Fed policymakers

Asset Classes

Bonds – at a glance

|

|

||||

Key themes

We believe the Fed’s strong commitment to tighten monetary policies is likely to put further upward pressure on US government bond yields, keeping the 10-year yield hovering around a key technical resistance of 4% in the coming quarter before normalising to our 12-month target of 3.5-3.75%.

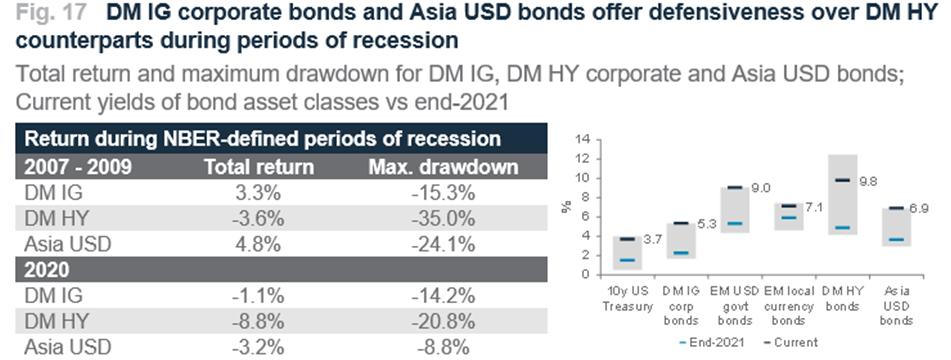

Bond yields have continued to edge higher on higher rates. Based on our assessment that rates are less likely to surge substantially higher from here in the next 12-months and IG-rated assets should offer a relatively better credit quality, we upgrade DM IG corporate bonds to Overweight. The change will put them, together with Asia USD bonds, to be our preferred asset classes within bonds.

We downgrade DM IG government bonds to Underweight, given the deteriorated risk-reward profile after interest rate volatility surged to multi-year highs. In addition, we downgrade EM local currency (LCY) government bonds to Underweight on our expectation that EM currencies are likely to remain under pressure against the backdrop of near-term USD strength, undermining the USD returns of EM local currency bonds.

Key chart

DM IG corporate bonds and Asia USD bonds offer better returns than their HY counterparts during periods of recessions; bond yields remain at, or close to, multi-year highs

What is our latest view on US Treasuries?

Global central banks have stuck to their hawkish stance by raising interest rates further and emphasised the need to continue on this path until inflation is on a clear path towards their long-term target. In the US, the Fed revised its forward guidance (‘dots’) significantly higher, where its median policy rate forecasts were raised to 4.375% for end-2022 (from 3.375%) and 4.625% for end-2023 (from 3.75%).

The tussle between hawkish monetary policies and slowing economic data have driven US Treasury yields higher, with 10-year yield hovering our three-month target of 4%. At this level, we believe the Fed’s hawkish shift in the next 12 months should have priced in and further sharp upward shift in rates should be likely behind us.

Having said that, for a 12-month perspective, the risk of recession in the US is surging upon a tighter financial condition. Hence, we see 10-year yield to normalise at 3.5–3.75%. In addition, our expectation for the Fed to hike rate to 4.5% as of mid-2023 would imply US government bond yield curve to stay inverted for a longer period from here.

Why have we downgraded DM and EM LCY government bonds?

We believe DM central banks’ hawkishness will continue to weigh on their government bond performance. In addition to revising our 12-month view on 10-year US government bond yield expectation higher to 3.5-3.75% (+25bps), we downgraded DM IG government bond to Underweight.

When bond market volatility is once again at near its two-year high, the risk-adjusted return for DM IG government bonds has driven lower. In an environment where bond yields are generally higher, we find the low absolute yield offered by this asset class not attractive. In addition, we have yet to see strong buying interest from traditional government bond investors, such as pensions and insurance companies. When the Fed is unwinding its balance sheet, we do not find the current supply-demand balance attractive.

Fig. 18 Elevated government bond market volatility has reduced the risk-reward profile

MOVE index

We downgrade EM LCY government bonds to Underweight as well. Although EM countries and central banks in general are facing less inflationary pressure than DM peers, we believe higher real yields in DM countries have reduced the relative attractiveness of EM local bonds. Also, our expectation for a stronger USD in the coming months is likely to weigh on EM currencies.

What value do we see in Asia USD bonds and DM IG corporate bonds?

We upgrade DM IG corporate bonds to Overweight, which falls in line with Asia USD bonds. Our constructive view for these two asset classes are driven by the following factors:

- We believe the surge in yields has created an attractive entry point for high quality bonds. DM IG corporate bonds and Asia USD bonds now offer a yield of over 5%, making them much more attractive than in the zero/low-yield world of the past decade.

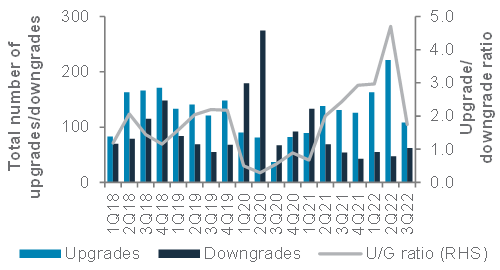

- Corporate fundamentals of these asset classes have improved in the post-pandemic quarters, as denoted by the IG rating and credit rating upgrades outpacing downgrades over the last 6-7 quarters. Although the implementation of the Inflation Reduction Act in the US, surging recession risk in the Euro Area and a slower China growth would likely be headwinds, we believe their strong credit quality should provide extra defensiveness.

- We believe the negative impact from a higher rate should gradually fade as most hawkish central bank policies are priced in. With the majority of the sharp upside move in US government bond yields likely behind us, we view the interest rate risk component as relatively contained for now.

Fig. 19 Credit fundamentals remain strong as rating upgrades continue to outpace downgrades

Total upgrades, downgrades and up/downgrade ratio of international rating agencies

Equity – at a glance

|

|

||||

|

Key themes

We are maintaining equities as a Neutral allocation within our asset allocation model. The Fed and the other central banks are prioritising the fight against inflation over maintaining growth. This is hurting investor sentiment, leading to elevated volatility and a less attractive risk-reward than in 2021.

Asia ex-Japan remains a preferred region, where we see the strongest earnings growth in 2023. We see Chinese equities performing in line with the region. The zero-Covid policy has led to an uneven economic growth. However, we are expecting the Chinese authorities to refocus their energy upon stimulating the economy, post the 20th Party Congress in October 2022.

UK equities is another preferred region. The new fiscal stimulus in the UK should be positive for growth, while GBP weakness should support corporate earnings of companies with significant overseas revenue. UK equities also have heavy exposure to sectors that may benefit from high inflation, such as energy, materials and financials. We prefer to take exposure on a currency-hedged basis.

Key chart

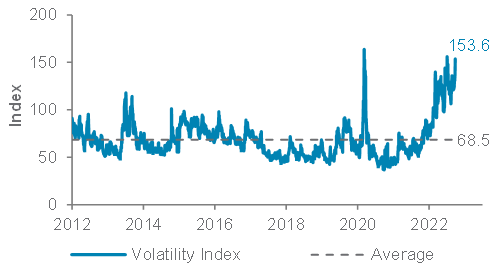

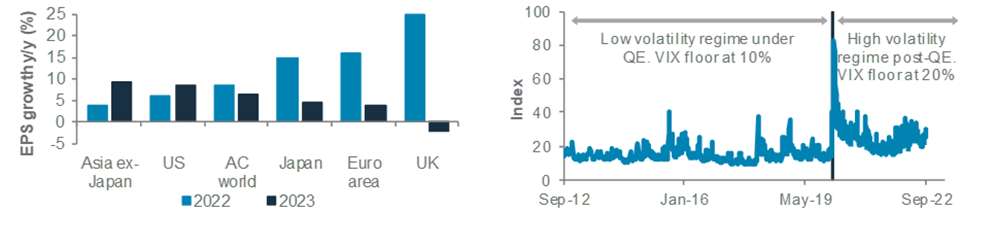

Earnings growth is a key supportive factor for Asia ex-Japan; elevated volatility hurting the risk-reward of equities

Fig. 20 Asia ex-Japan has the highest projected EPS growth in 2023; volatility is likely to be elevated vs the times of the low-rate regime prior to the pandemic

Projected EPS growth in 2022 and 2023 across major regions; VIX index

Asia ex-Japan and UK remain preferred; downgrade China to Neutral within the region

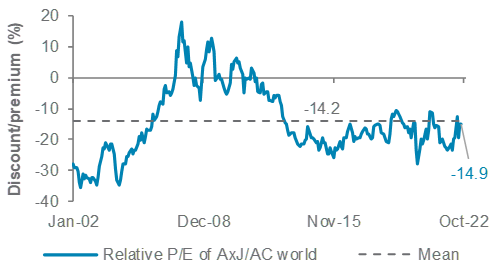

Asia ex-Japan continues to be a preferred region within global equities. While the relative valuation vs global equities have reverted to the long-term average, earnings growth in Asia ex-Japan is likely to be the highest among our regions in 2023.

Fig. 21 Asia ex-Japan valuation at long-term average discount vs global equities. Strong earnings growth in 2023 is the key supporting factor

Relative 12m forward P/E of MSCI Asia ex-Japan vs MSCI AC World

We have downgraded Chinese equities to perform in line within Asia ex-Japan, as the zero-COVID policy has led to unevenness in economic growth. However, we do believe the government is likely to refocus its direction into stimulating the economy after the 20th Party Congress. China’s credit impulse is already recovering, but further fiscal stimulus, primarily aimed at boosting consumption, remains likely, while regulatory pressures are likely to ease further.

We believe Indian equities are likely to outperform within the region. The country has continued to record good macro data, such as solid retail sales, as well as healthy property markets. We see continued prospects of good, internally driven, growth in India. The risk in Indian equities lies in their relatively expensive valuation, both vs Asia ex-Japan and on an absolute basis.

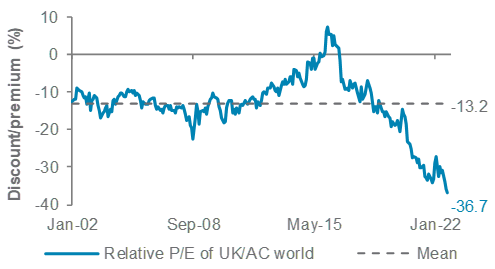

Fig. 22 UK equities at deep discount vs global equities

Relative 12m forward P/E of MSCI UK vs MSCI AC World

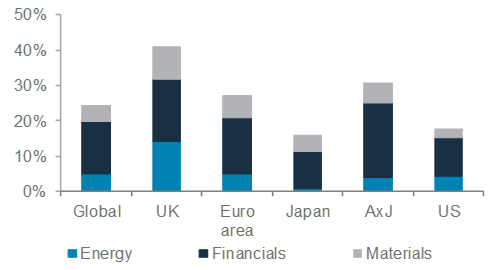

UK is another preferred region. Valuation is at its deepest discount compared with the last 20 years, and inexpensive on an absolute basis. Its equities offer a good balance between income and growth, offering relative dividend yield 2% higher than global equities. They are heavy on sectors that may benefit from an inflationary environment, such as energy and materials. The weakness in the GBP is also likely to benefit the large caps, which derive more than 70% of their revenues from overseas. We prefer to get exposure to UK equities on a currency-hedged basis.

Fig. 23 UK equities remain preferred on heavy exposure to sectors that may benefit from inflation

Weight of energy, financials and materials sectors in regional MSCI equity market indices

Meanwhile, we are maintaining our core exposure to US equities. Having dropped more than 20% from its peak, US equities have priced in a high likelihood of a recession, and valuation has become more reasonable, with 12-month forward P/E at 16x earnings, in line with the long-term average. However, there are still headwinds from potentially higher yields, as the Fed is unlikely to cut rates in 2023, which was previously priced into risky assets. This would hurt valuations, especially for growth stocks. Slowing growth also poses a risk to earnings.

Japan equities are also a Core Holding. Valuations remain attractive on an absolute and relative basis to global equities and the weak JPY has been tailwind for exporters as well as tourism. However, local consumption remains weak and inflation concerns may start to bite, given the country’s latest CPI print was the highest in years.

Lastly, we maintain the least preferred status for Euro area equities. Rampaging energy prices and continued uncertainties caused by the war between Russia and Ukraine are leading to heavy inflation and economic slowdown. This is leading to persistent downside risks to earnings, although margins remain healthy, and valuation is certainly undemanding.

Equity sector views

|

Cautious amid volatile markets

Energy sectors are preferred

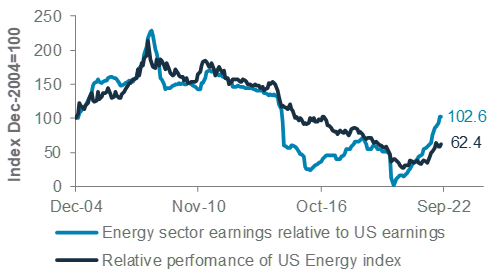

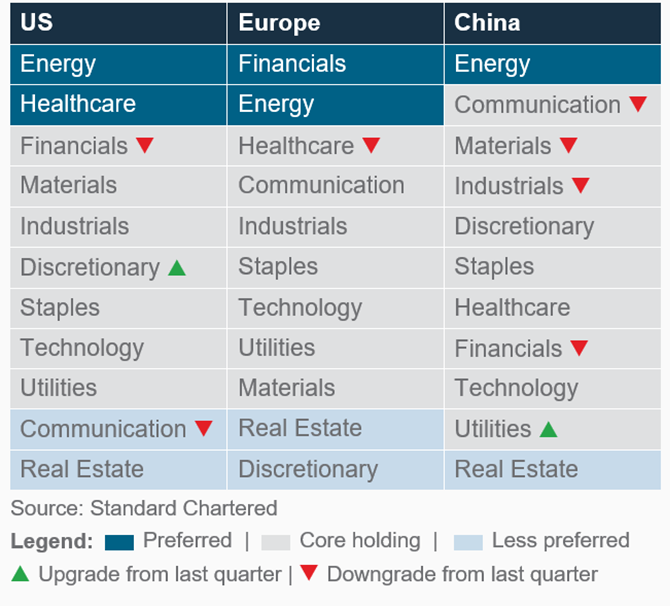

Equity markets are volatile amid high inflation, rising interest rates, recession fears and geopolitical tensions. Against this backdrop, we are selective and cautious in our sector picks, and sensitive to elevated valuations amid rising interest rates. Energy is the clear sector preference globally. A trend towards greater energy independence is driving governments to be supportive of energy investments even amid the green transition. Oil and gas producers remain disciplined on costs and capex. Consensus expectations are for global energy sector earnings to decline by 12% in 2023 from the high base in 2022, but we believe current depressed valuations more than make up for this. Energy equities have yet to catch up to the strong earnings outperformance.

US

Energy remains preferred, as valuation remains attractive. The consensus 12m forward P/E is 7.5x, a 52% discount to the broader market, compared with a median discount of 11% historically. Producers are disciplined in capex and returning cash to shareholders. The US is also helping Europe to diversify away from Russian gas.

Healthcare remains preferred, giving defensive exposure amid rising risks to growth. It offers steady earnings growth, which is less volatile than the broader market. Valuations remain reasonable, in line with the historical average discount to market. Margins are expected to be resilient, withstanding rising costs. The Inflation Reduction Act has manageable drug pricing provisions, although it introduced some uncertainty on whether drug-pricing controls could broaden.

Other changes: Financials are downgraded to core, as an inverted yield curve and slowdown in IPOs/M&As could be a

Fig.24 Outperformance in energy sector earnings points to further outperformance by energy equities

Consensus 12m forward EPS for MSCI US Energy relative to MSCI US and performance of MSCI US Energy relative to MSCI US index

drag on profitability. Rising recession risk could also lead to rising loan loss provisions.

Europe

Financials remain preferred, with valuation being an attractive buffer. Consensus 12m forward P/E of 7.6x is at the bottom of its historic range, despite rising interest rates supporting higher interest income for banks. Earnings revision has been positive for the sector and strong capital positions protect banks from the Russia-Ukraine conflict.

Energy remains preferred as the catch-up opportunity to its earnings outperformance remains. ESG concerns that used to be a headwind have moved more into the background amid geopolitical and energy supply concerns.

Other changes: Healthcare is downgraded to core. Although earnings are defensive, its valuation has climbed, with the premium to market above its historic average.

China

Energy remains preferred as valuation remains very attractive relative to its own history and relative to the market. The sector is also benefitting from elevated coal prices due to strong demand from coal-fired power plants, as hydropower stations face a drought. Sector costs remain well under control.

Other changes: Communication, materials, industrials and financials are downgraded to core. These sectors are linked to China’s economic growth, which is held back by lockdowns, where visibility is limited.

Fig.25 Our sector views by region

FX – at a glance

|

|

||||

|

Key themes

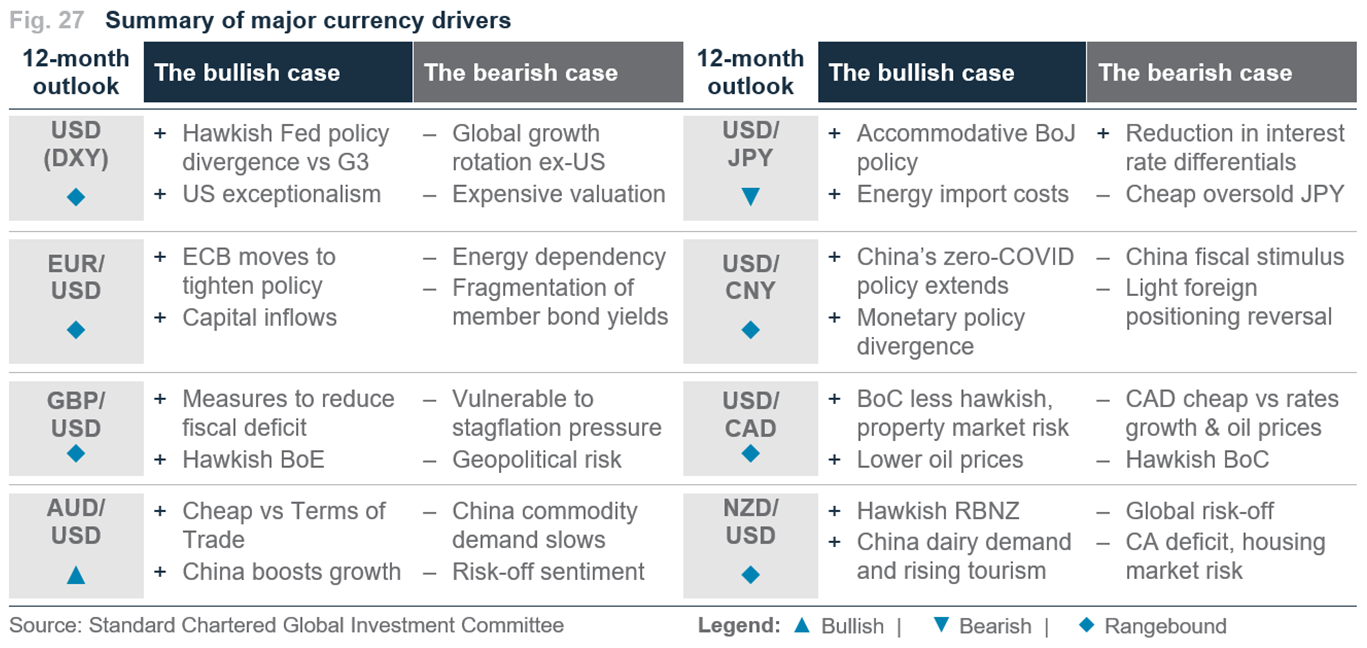

Over the past month, the USD has surged sharply higher, to its 20-year highs, due to a combination of a persistently hawkish Fed, which guided to faster-than-expected rate hikes, as well as idiosyncratic weakness in a number of other major currencies. This leads us to be bullish on the USD on a three-month horizon, with DXY likely to rise towards 116.5-117.0.

Near term USD strength is likely to be driven by (i) the likelihood of the Fed hiking rates at a faster pace relative to the other major central banks, which can continue to push interest rate differentials in favour of the USD, (ii) greater global growth concerns that are likely to fuel safe-haven USD demand, and (iii) elevated geopolitical concerns, especially in Europe and the Middle East.

However, over a 6-12 month horizon, we expect the USD to peak. In our assessment, (i) we expect US inflation to gradually turn lower over 2023, which should give the Fed the leeway to slow or even pause rate hikes, (ii) rate hikes from other major central banks through 2023 should narrow the interest rate differentials with the US, (iii) capital flows are likely to turn away from the US on slower US growth and robust growth in Asia, and (iv) easing of geopolitical uncertainty around Europe and improving Chinese growth could potentially reduce the safe-haven demand. The combination of all these factors should also trigger a modest correction of the current over-valuation in the USD.

Key chart

Hawkish Fed and rapid rate hikes have pushed the real interest rate differentials in favour of the USD. USD strength has also been helped by idiosyncratic risks in the EUR, GBP and JPY – the biggest components of DXY

Fig. 26 Strong momentum has pushed USD strength ahead of fundamentals

USD index (DXY), DXY-weighted real 10y yield differentials; composition of DXY

A kinked path for USD, EUR, GBP and JPY

EUR/USD is likely to weaken over the next 1-3 months, potentially testing support around 0.90, before settling around 0.93-0.94. While European gas inventories have reached nearly 85% of capacity, energy security and rationing concerns along with relatively slower pace of rate hikes from ECB are likely to exert downward pressure on EUR/USD in the near term. Over a 12-month horizon, we expect a reduction in interest rate differentials between US and Europe and a reversal of its current undervaluation to push the EUR higher. However, the persistent growth headwinds and elevated geopolitical risks lead us change our 12-month stance from Bullish to Neutral. We expect CHF to trade broadly in line with the EUR over a 12-month horizon.

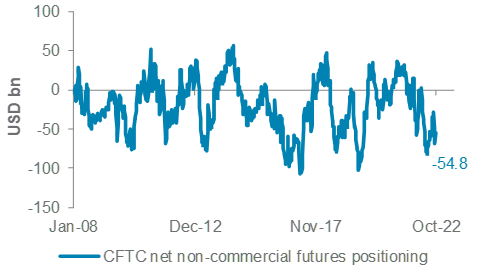

GBP/USD recently plunged into a 50-year intra-day low due to fiscal stability concerns after the new government announced an unfunded stimulus plan. While a test of parity cannot be ruled out, BoE intervention appears to have calmed the market and we see 1.05 as a strong support, given already substantial short positioning. We downgrade our 12-month stance from Bullish to Neutral as elevated inflation means that the BoE is likely to continue hiking rates even amid the downbeat growth outlook. Increasing twin deficits are expected to add further drag on the currency.

Fig.28 Stretched short positioning may cap near-term downside in GBP/USD, with 1.05 being the key support

GBP CFTC net non-commercial futures positioning

Strong USD momentum is likely to cause AUD/USD to trade in a range in the near term, but we remain bullish over a 12-month horizon. The AUD stands out as cheap from a valuation perspective. While valuation alone is rarely a

driver of trend reversals, we expect the strong Terms of Trade and expectations of stronger Australian growth relative to US and Europe are likely to act as tailwind

The rising risk of a global growth slowdown has led us to now expect materially lower oil prices over the next 12 months. While the BoC is likely to continue hiking rates to curb inflation, Canada is likely to witness a growth slowdown in 2023, similar to the US. Hence, weaker risk sentiment and lower oil prices are likely to weigh on the CAD, leading us to turn Neutral on the CAD over the next 3 and 12 months. We expect USD/CAD to trade in a 1.33-1.38 range, with a modestly lower bias.

Fig.29 Summary of our key FX forecasts

In the near term, we expect USD/JPY to continue trending higher as the divergent monetary policies – Hawkish Fed vs firmly dovish BoJ – are likely to push 2-year interest rate differential higher, pushing USD/JPY to re-test the 146-147 resistance, a level which saw intervention by the MoF. We turn bearish USD/JPY over a 12-month horizon as we expect peaking out of US government bond yields to reduce interest rate differential, which, combined with lower oil prices and partial reversal of short-positioning and undervaluation, are likely to push USD/JPY towards the 140-141 range.

Similar to Japan, we expect divergent monetary policies between the Fed and the PBoC to put upward pressure on USD/CNY in the near term, with 7.20 being a key resistance. However, our expectation of an acceleration in Chinese growth in 2023, combined with proactive measures from the PBoC, should lead the pair to trade in a broadly rangebound manner over a 12-month horizon.

Gold, crude oil – at a glance

|

|

||||

Key themes

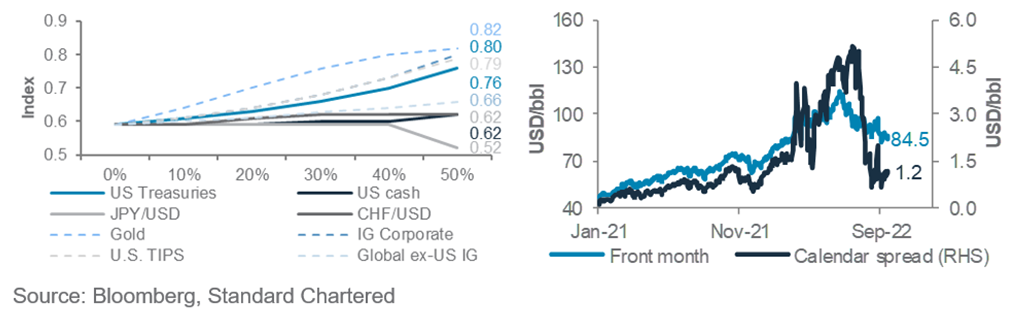

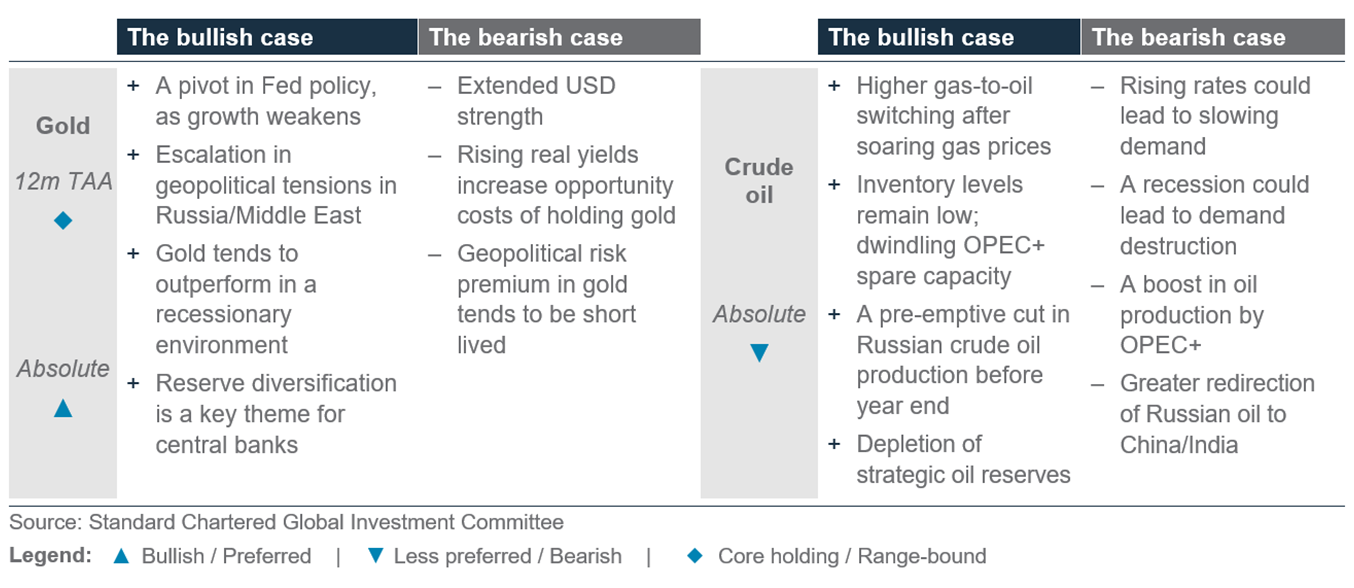

Gold remains a core holding and a key portfolio diversifier. Gold prices have trended broadly lower since peaking earlier in February this year. The precious metal is facing major headwinds against a backdrop of rising yields and a stubbornly strong USD as the Fed reiterated its hawkish stance. Outflows from global gold ETFs continued for the fourth consecutive month. Nonetheless, gold prices are still likely to move higher on a 12-month horizon as positioning has since scaled back and is looking extremely short on a historical basis. Geopolitical risks continue to flare as the Russia-Ukraine military conflict rages on. Additionally, risk of a recession appears to have materially increased and gold has proven to be a superior hedge in the event of a downturn. Hence, we believe gold should remain an integral part of clients’ portfolios.

Oil prices are likely to stabilise. We turn Neutral on oil prices over a 12-month horizon as the likelihood of a recession is rising. With more central banks being forced to take a harder stance against inflation, it is likely to lead to a significant contraction in demand, which could help rebalance the oil market on a longer term. However, we remain bullish on oil prices over a three-month horizon as EU sanctions are expected to take effect in December, while the proposed cap on Russian oil prices by the G7 could tighten supply and increase volatility of oil prices. As winter approaches and natural gas prices remain elevated, we could see rising short-term oil demand from gas-to-oil switching.

Key chart

Growing recessionary fears, equity market drawdowns and elevated geopolitical tensions are key tailwinds for gold

Rising interest rates could curb economic activity and weigh on the demand for oil

Fig. 31 Gold provides the best risk-adjusted return when added to a portfolio; tightening spreads indicate an easing of oil markets

LHS chart: Sharpe ratios of portfolios with proportionately increasing allocation to safe-haven asset

RHS chart: WTI front month vs first-to-third calendar spread (1m-3m price)

Liquid alternatives – at a glance

|

Key themes

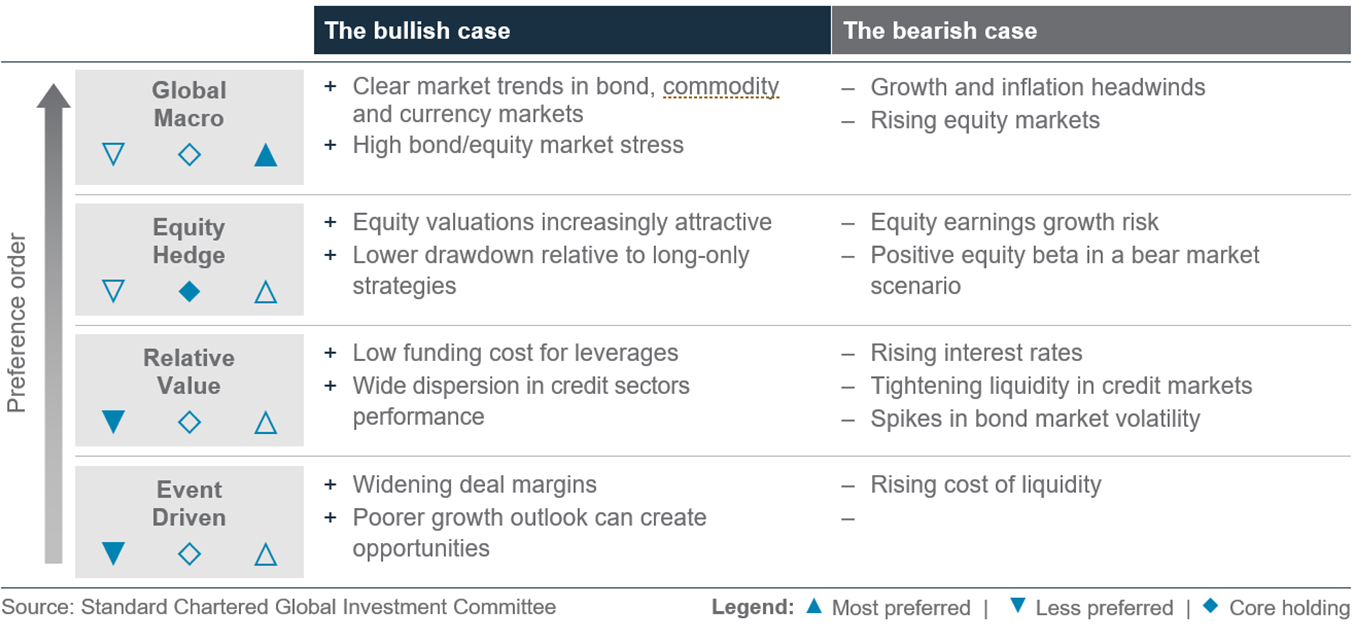

As we discussed in the Investment Strategy section, the Fed’s still-hawkish tone is once again putting downward pressure on risky assets. Against this backdrop, we continue to see Liquid Alternative Strategies as a strong core holding, particularly in a market where correlations across major asset classes continue to be unusually high.

Our top pick continues to be the global macro/commodity trading advisor (CTA) sub-strategy. First, it has a historical track record of delivering positive returns during the past economic recessions, outperforming other alternative strategies. Second, they have successfully benefited from the rising trend in bond yields, which we believe makes it an attractive strategy in today’s market environment for both returns and portfolio diversification.

We retain equity hedge strategies as a core holding. On the upside, they remain one interesting way to retain some exposure to equities in today’s volatile markets given they have a positive correlation with global equities, but with a lower ‘beta’ – ie, they tend to underperform during periods of rising equity markets, but downside volatility tends to be much more limited relative to long-only equities given their long/short approach. Having said that, the correlation with equities is still a positive one, at least at a broad asset class level; hence, they are unlikely to be immune to significant drawdowns in global equities.

We continue to view Event Driven strategies as less preferred. Rising interest rates and recession concerns remain significant headwinds to M&A volume, which remains a key driver of this asset class. A worsening growth and credit quality outlook would benefit distressed strategies, though these remain small as a component of the sub-asset class. We also continue to see Relative Value strategies as less preferred as they tend to underperform when interest rates rise.

Key chart

Global Macro/CTA strategies maintained a good track record during past economic recessions

Fig. 32 Macro/CTA strategies successfully benefiting from trending bond yields

HFRX Macro/CTA Index vs 10y US government bond yield

Quant perspective

US market risk model – bullish bond

|

Bearish equity but bullish bond risks

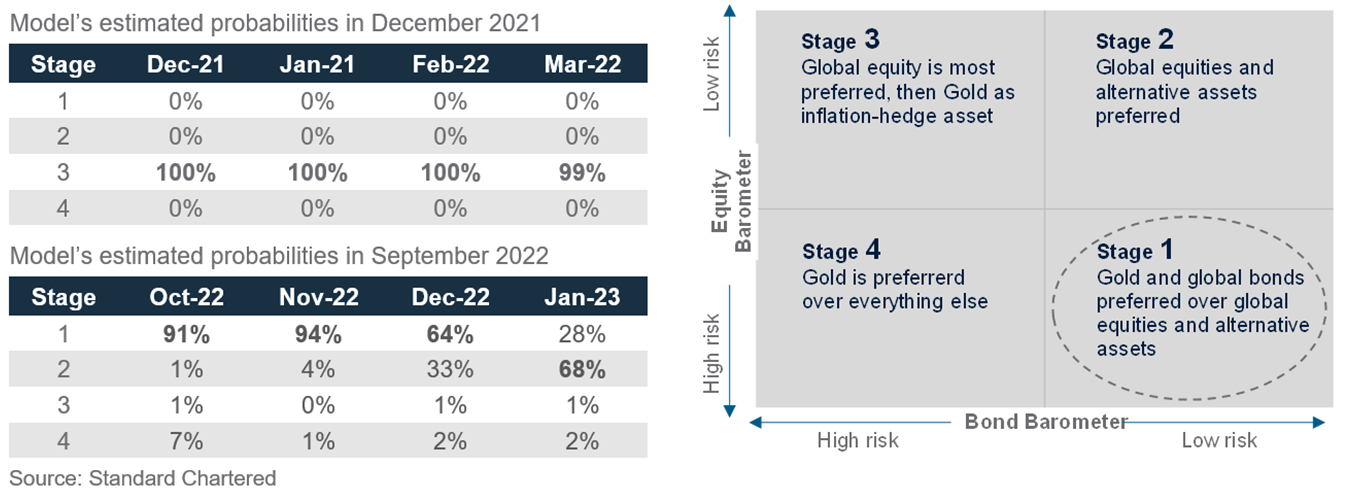

Our US Equity-Bond Market Risk (EBMR) models the downside risks in US equities and the US 10-year government bonds. It uses 11 economic and market factors to create equity and bond risk barometers. If the value of a barometer falls below 50, it signals higher downside risks and vice versa.

The US EBMR model remains in Stage 1, where it continues to anticipate higher downside risks in US equities, but lower downside risks in US government bonds. Since the equity barometer fell below 50 in January, the S&P500 has fallen by c.20%. Meanwhile, the bond barometer, which previously captured c.2.1% rise in the US 10-year government bond yield, views the risks of sustained spikes in yields to be low going forward. This implies that the recent steep rise in US 10-year yield due to Fed hikes signals a potential overtightening, given weaker fundamentals.

Fig. 33 EBMR bearish on equity and bond market risks

US equity and bond market risk barometers

The equity barometer consists of 11 equity indicators. In September, the barometer remains at a low of 9 due to still elevated inflation and higher interest rates, as they lead to slower growth (as indicated more recently in the YoY change in US housing starts) and bearish momentum in equity and commodity markets. With a combination of these depressed factors, the equity barometer is unlikely to bounce above 50 over the short term.

Meanwhile, the bond barometer, which tracks six bond indicators, improved further to 71 from 57 in the previous month. The improvement is driven by a weaker signal from US housing starts as weaker fundamentals tend to support defensive assets such as US government bonds. Another growth factor that has been similarly supporting the bond barometer is the decline in the US Manufacturing PMI. Low US jobless claims remain the only negative factor for the bond barometer as a tight labour market provides room for the Fed to hike rates further.

The model’s projections are skewed towards Stage 1, but they now show a high likelihood of entering a recovery phase or Stage 2 in Jan-23. This implies that the near-term volatility in US equities is unlikely to abate over the next three months. Meanwhile, we also caution against taking excessive risk in high duration bonds based on the bond barometer yet as monetary policy and inflation remain key drivers.

Implications on global assets

Data since 1999 suggest gold and bonds are the most preferred in Stage 1. The model’s preference for the asset is based on its long-term relationship with the market cycle, which favours gold and bonds as defensive assets in Stage 1.

Fig. 34 Scenarios over the coming months till January 2023 vs December 2021 (Outlook 2022) projections

Probability of the evolution of financial market risk cycle from the current Stage 1 and preferred assets

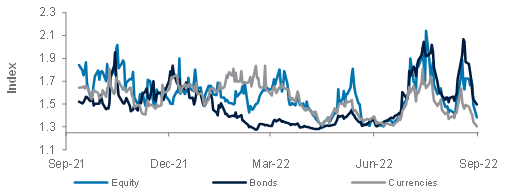

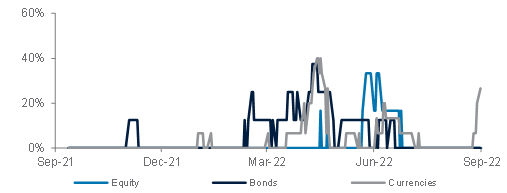

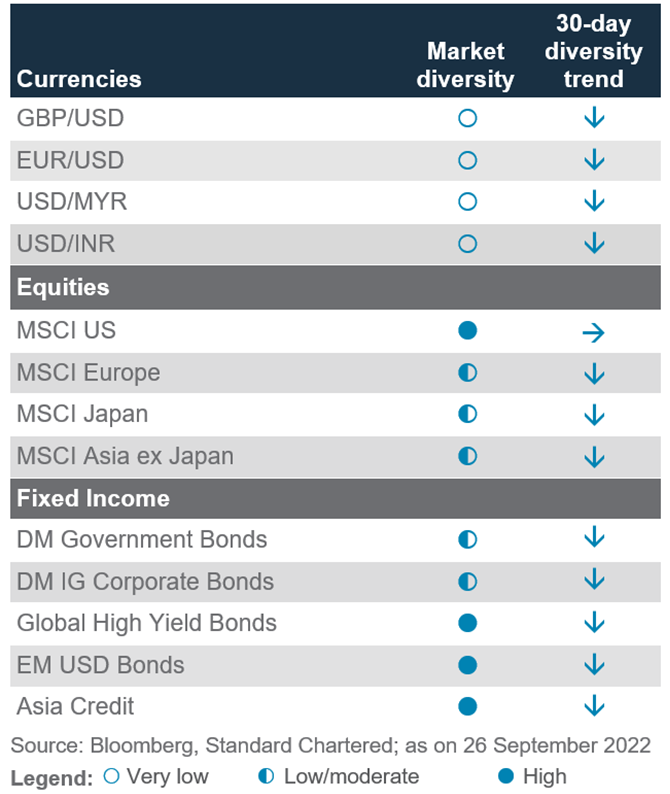

Tracking market diversity

|

About our market diversity indicators

Our market diversity indicators help to identify a potential change in short-term trends due to a fall in market breadth across equities, credit, FX and commodities. When market diversity falls, it implies either buyers or sellers are dominating, leading to a rapid rise or fall in asset prices. This is usually unsustainable and is likely to be followed by a slowdown or a reversal. Our diversity indicator is based on a statistical index called fractal dimension; a value below 1.25 serves as a guideline that prices are rising or falling too fast.

Where is diversity falling or rising this month?

Our indicators show market diversity across equities, bonds and currencies have dipped sharply in September amid the sell-off in both bond and equity markets and the rally in DXY. Although the average of our indicator values is still above the critical thresholds for each of these asset classes, we spotted some reversal opportunities within currencies.

Continued weakness in equity markets has caused their diversity levels to narrow significantly over the past month. However, none of the major equity markets we track has diversity level breaching below the 1.25 critical threshold of our diversity indicator. This is due to elevated market volatility we have seen this year, as they act to balance out any supply demand imbalances that typically lead to short-term reversal opportunities. Despite more than 7% sell-off across major equity indices since August, we may need to see further downside before our diversity indicators flag a significant risk of potential reversals.

Fig. 35 Average market diversity score by asset class

Diversity narrows steeply as 2022 trends resume

Fig. 36 Percentage of assets with diversity score <1.25

No red flags across key asset classes

Similarly, there are no reversal signs for major bond markets. DM government and corporate bonds have the lowest diversity values currently, as they led the sell-off since July. Despite trading sharply lower, however, these bond indices have also yet to breach the 1.25 threshold. As a result, we continue to caution against taking excessive exposure in high duration bonds, despite the bullish view from our longer-term macro model (US EBMR) as monetary policy remains a key uncertainty.

For currencies, reversal signals have started to emerge for multiple USD pairs – EUR/USD, GBP/USD, USD/MYR and USD/INR. This coincided with the Fed’s third consecutive hike of 75bps, which led to a more than 3.5% rise in DXY over the past week, indicating overbought conditions in the USD. The oversold condition of the GBP against the USD is also triggered by UK tax cuts.

Fig. 18 Diversity across key assets

Performance Review

Foundation: Asset allocation summary

Performance of our calls

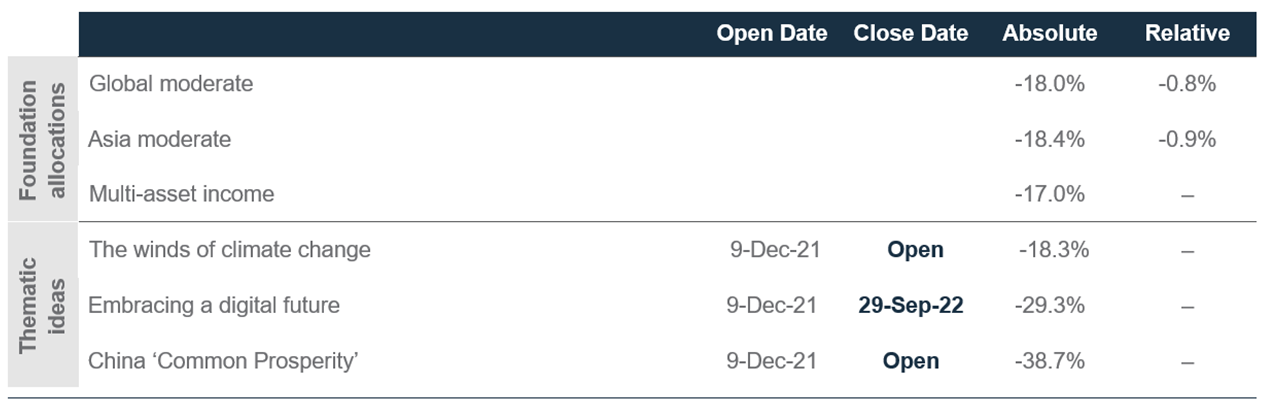

Fig. 38 Summary of our 2022 calls

Performance measured from 9 December 2021 or when the call was opened, to 29 September 2022 or when the view was closed.

Past performance is not an indication of future performance. There is no assurance, representation or prediction given as to any results or returns that would actually be achieved in a transaction based on any historical data.

‘Absolute’ represents the simple absolute return. ‘Relative’ tracks our Tactical Asset Allocations vs. our Strategic Asset Allocation, or if a relative measure was specified in individual themes.

Global moderate and Asia moderate comprise our Tactical Asset Allocations as described in the Global Market Outlook publications. Broad asset class allocations are represented by MSCI AC World, FTSE Non-MBS WorldBIG Index, Bloomberg commodities ex-agriculture & livestock, HFRX total return and J.P. Morgan 3m cash indices. Equity allocations are represented by MSCI USA, EMU, UK, Japan, Asia ex-Japan and Other EM total return indices. Bond allocations are represented by FTSE WorldBig Government Index, FTSE WorldBig Corp Index, J.P. Morgan EMBI Global Diversified, EM Local, Asia Credit Index and Bloomberg Global High Yield indices.

In our Multi-Asset Income allocation, bond allocations are represented by Bloomberg Global High Yield Index, S&P Global Leveraged Loan Index, J.P. Morgan EMBI Global Diversified, EM Local, Asia Credit and Asia Credit Index Non- Investment Grade, FTSE WorldBig Corp Index and FTSE WorldBig Government Index. Equity allocations are represented by MSCI AC World and AC Europe High Dividend Yield Index. Non-core allocations are represented by Chicago Board Options Exchange S&P 500 BuyWrite Index, Barclays Global Contingent Capital Index Value Unhedged USD, SPDR ICE Preferred Securities ETF, FTSE EPRA/NAREIT Asia Pacific Index and FTSE EPRA/NAREIT Global Index.

For indices used to measure thematic ideas, please refer to the respective thematic publications.

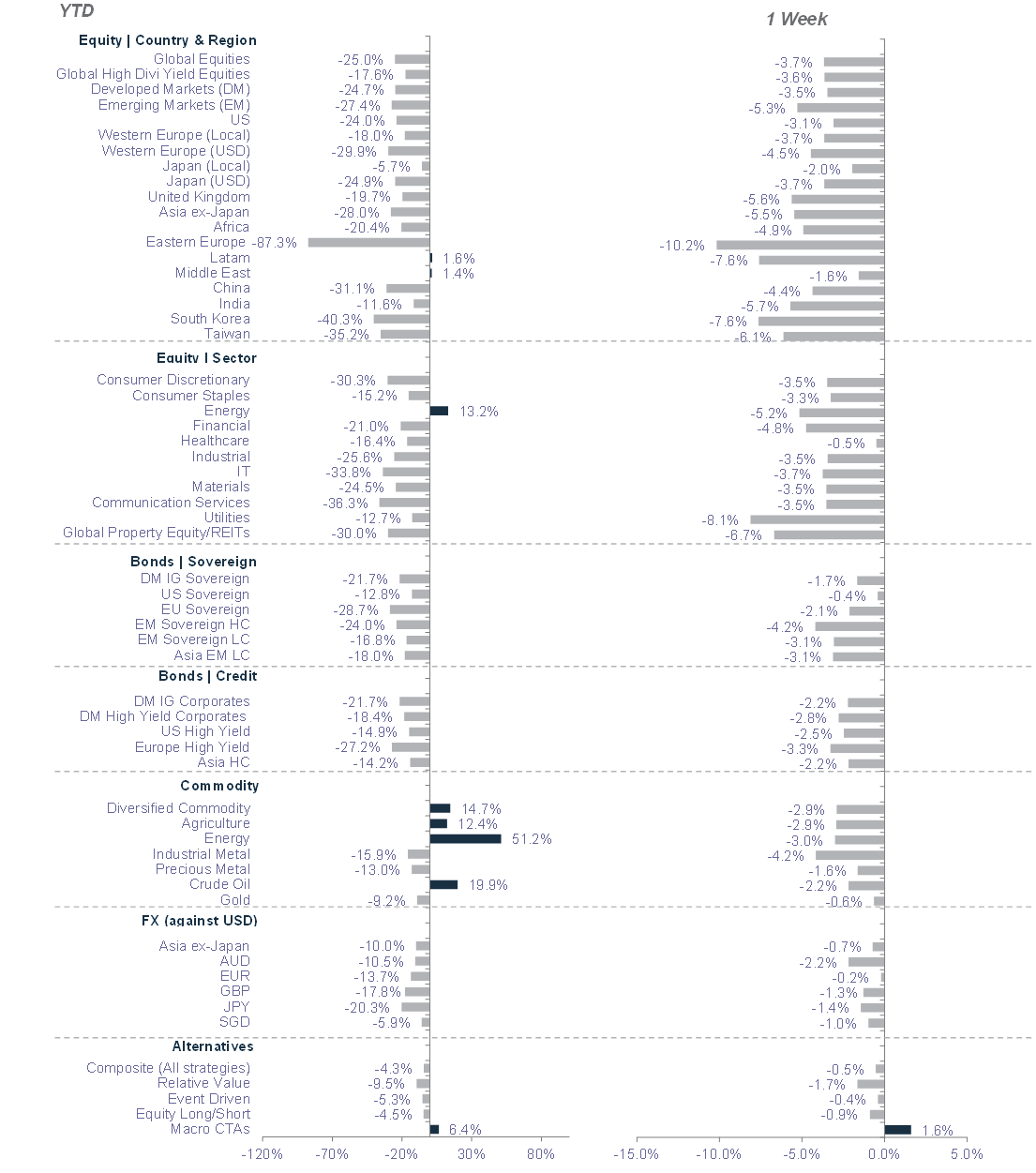

Market performance summary*

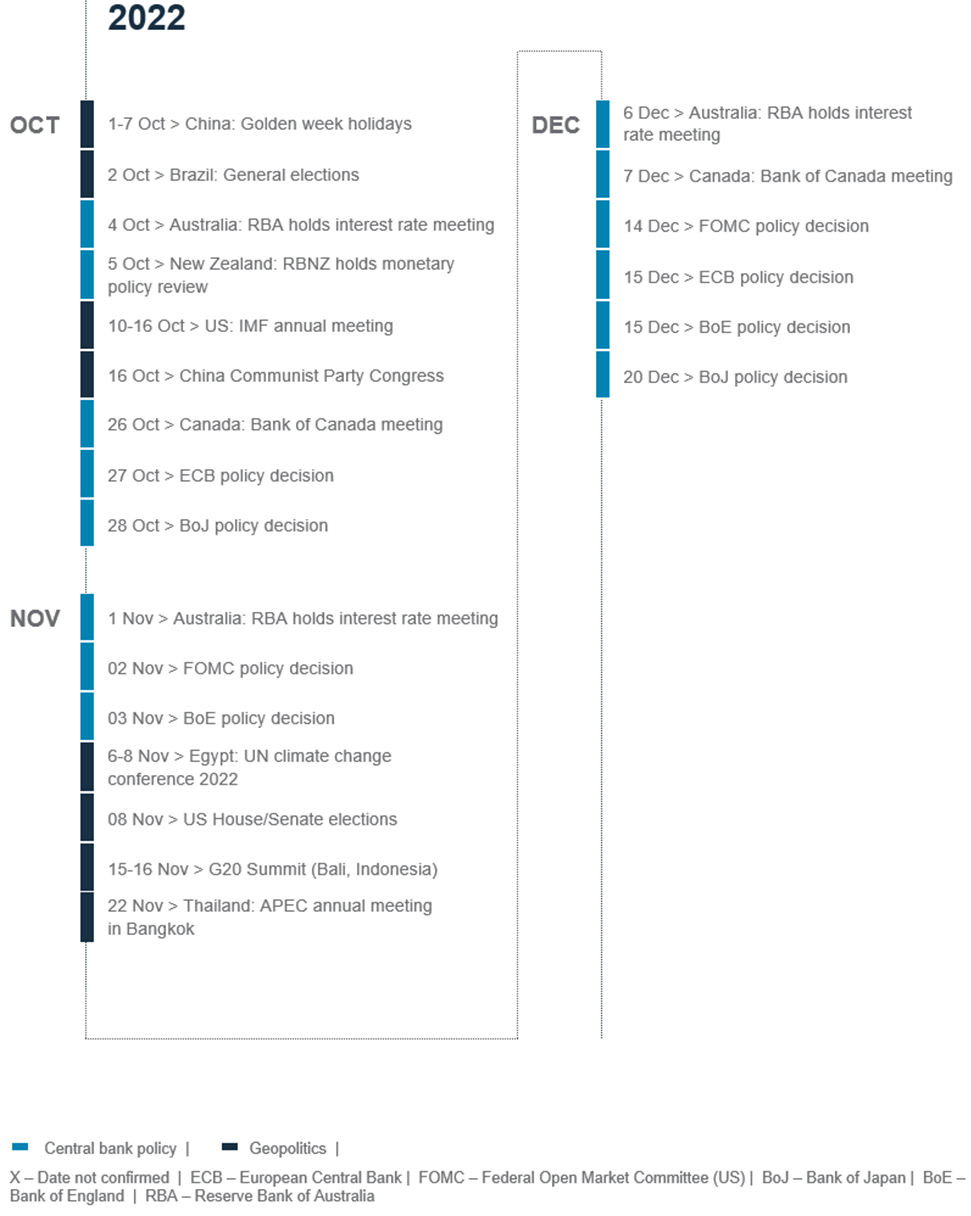

Key events

For more insights

Explanatory notes

1. The figures on page 5 show allocations for a moderate risk profile only – different risk profiles may produce significantly different asset allocation results. Page 5 is only an example, provided for general information only and they do not constitute investment advice, an offer, recommendation or solicitation. They do not take into account the specific investment objectives, needs or risk tolerances of a particular person or class of persons and they have not been prepared for any particular person or class of persons.

2. Contingent Convertibles are complex financial instruments and are not a suitable or appropriate investment for all investors. This document is not an offer to sell or an invitation to buy any securities or any beneficial interests therein. Contingent convertible securities are not intended to be sold and should not be sold to retail clients in the European Economic Area (EEA) (each as defined in the Policy Statement on the Restrictions on the Retail Distribution of Regulatory Capital Instruments (Feedback to CP14/23 and Final Rules) (“Policy Statement”), read together with the Product Intervention (Contingent Convertible Instruments and Mutual Society Shares) Instrument 2015 (“Instrument”, and together with the Policy Statement, the “Permanent Marketing Restrictions”), which were published by the United Kingdom’s Financial Conduct Authority in June 2015), other than in circumstances that do not give rise to a contravention of the Permanent Marketing Restrictions.

Disclosure

This document is confidential and may also be privileged. If you are not the intended recipient, please destroy all copies and notify the sender immediately. This document is being distributed for general information only and is subject to the relevant disclaimers available at our Standard Chartered website under Regulatory disclosures. It is not and does not constitute research material, independent research, an offer, recommendation or solicitation to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments. This document is for general evaluation only. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person or class of persons and it has not been prepared for any particular person or class of persons. You should not rely on any contents of this document in making any investment decisions. Before making any investment, you should carefully read the relevant offering documents and seek independent legal, tax and regulatory advice. In particular, we recommend you to seek advice regarding the suitability of the investment product, taking into account your specific investment objectives, financial situation or particular needs, before you make a commitment to purchase the investment product. Opinions, projections and estimates are solely those of SC at the date of this document and subject to change without notice. Past performance is not indicative of future results and no representation or warranty is made regarding future performance. The value of investments, and the income from them, can go down as well as up, and you may not recover the amount of your original investment. You are not certain to make a profit and may lose money. Any forecast contained herein as to likely future movements in rates or prices or likely future events or occurrences constitutes an opinion only and is not indicative of actual future movements in rates or prices or actual future events or occurrences (as the case may be). This document must not be forwarded or otherwise made available to any other person without the express written consent of the Standard Chartered Group (as defined below). Standard Chartered Bank is incorporated in England with limited liability by Royal Charter 1853 Reference Number ZC18. The Principal Office of the Company is situated in England at 1 Basinghall Avenue, London, EC2V 5DD. Standard Chartered Bank is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and Prudential Regulation Authority. Standard Chartered PLC, the ultimate parent company of Standard Chartered Bank, together with its subsidiaries and affiliates (including each branch or representative office), form the Standard Chartered Group. Standard Chartered Private Bank is the private banking division of Standard Chartered. Private banking activities may be carried out internationally by different legal entities and affiliates within the Standard Chartered Group (each an “SC Group Entity”) according to local regulatory requirements. Not all products and services are provided by all branches, subsidiaries and affiliates within the Standard Chartered Group. Some of the SC Group Entities only act as representatives of Standard Chartered Private Bank and may not be able to offer products and services or offer advice to clients.

Copyright © 2025, Accounting Research & Analytics, LLC d/b/a CFRA (and its affiliates, as applicable). Reproduction of content provided by CFRA in any form is prohibited except with the prior written permission of CFRA. CFRA content is not investment advice and a reference to or observation concerning a security or investment provided in the CFRA SERVICES is not a recommendation to buy, sell or hold such investment or security or make any other investment decisions. The CFRA content contains opinions of CFRA based upon publicly-available information that CFRA believes to be reliable and the opinions are subject to change without notice. This analysis has not been submitted to, nor received approval from, the United States Securities and Exchange Commission or any other regulatory body. While CFRA exercised due care in compiling this analysis, CFRA, ITS THIRD-PARTY SUPPLIERS, AND ALL RELATED ENTITIES SPECIFICALLY DISCLAIM ALL WARRANTIES, EXPRESS OR IMPLIED, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE, to the full extent permitted by law, regarding the accuracy, completeness, or usefulness of this information and assumes no liability with respect to the consequences of relying on this information for investment or other purposes. No content provided by CFRA (including ratings, credit-related analyses and data, valuations, model, software or other application or output therefrom) or any part thereof may be modified, reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval system, without the prior written permission of CFRA, and such content shall not be used for any unlawful or unauthorized purposes. CFRA and any third-party providers, as well as their directors, officers, shareholders, employees or agents do not guarantee the accuracy, completeness, timeliness or availability of such content. In no event shall CFRA, its affiliates, or their third-party suppliers be liable for any direct, indirect, special, or consequential damages, costs, expenses, legal fees, or losses (including lost income or lost profit and opportunity costs) in connection with a subscriber’s, subscriber’s customer’s, or other’s use of CFRA’s content.

Market Abuse Regulation (MAR) Disclaimer

Banking activities may be carried out internationally by different branches, subsidiaries and affiliates within the Standard Chartered Group according to local regulatory requirements. Opinions may contain outright “buy”, “sell”, “hold” or other opinions. The time horizon of this opinion is dependent on prevailing market conditions and there is no planned frequency for updates to the opinion. This opinion is not independent of Standard Chartered Group’s trading strategies or positions. Standard Chartered Group and/or its affiliates or its respective officers, directors, employee benefit programmes or employees, including persons involved in the preparation or issuance of this document may at any time, to the extent permitted by applicable law and/or regulation, be long or short any securities or financial instruments referred to in this document or have material interest in any such securities or related investments. Therefore, it is possible, and you should assume, that Standard Chartered Group has a material interest in one or more of the financial instruments mentioned herein. Please refer to our Standard Chartered website under Regulatory disclosures for more detailed disclosures, including past opinions/ recommendations in the last 12 months and conflict of interests, as well as disclaimers. A covering strategist may have a financial interest in the debt or equity securities of this company/issuer. All covering strategist are licensed to provide investment recommendations under Monetary Authority of Singapore or Hong Kong Monetary Authority. This document must not be forwarded or otherwise made available to any other person without the express written consent of Standard Chartered Group.

Sustainable Investments

Any ESG data used or referred to has been provided by Morningstar, Sustainalytics, MSCI or Bloomberg. Refer to 1) Morningstar website under Sustainable Investing, 2) Sustainalytics website under ESG Risk Ratings, 3) MCSI website under ESG Business Involvement Screening Research and 4) Bloomberg green, social & sustainability bonds guide for more information. The ESG data is as at the date of publication based on data provided, is for informational purpose only and is not warranted to be complete, timely, accurate or suitable for a particular purpose, and it may be subject to change. Sustainable Investments (SI): This refers to funds that have been classified as ‘Sustainable Investments’ by Morningstar. SI funds have explicitly stated in their prospectus and regulatory filings that they either incorporate ESG factors into the investment process or have a thematic focus on the environment, gender diversity, low carbon, renewable energy, water or community development. For equity, it refers to shares/stocks issued by companies with Sustainalytics ESG Risk Rating of Low/Negligible. For bonds, it refers to debt instruments issued by issuers with Sustainalytics ESG Risk Rating of Low/Negligible, and/or those being certified green, social, sustainable bonds by Bloomberg. For structured products, it refers to products that are issued by any issuer who has a Sustainable Finance framework that aligns with Standard Chartered’s Green and Sustainable Product Framework, with underlying assets that are part of the Sustainable Investment universe or separately approved by Standard Chartered’s Sustainable Finance Governance Committee. Sustainalytics ESG risk ratings shown are factual and are not an indicator that the product is classified or marketed as “green”, “sustainable” or similar under any particular classification system or framework.

Country/Market Specific Disclosures