This is to inform that by clicking on the hyperlink, you will be

leaving

sc.com/sg

and entering a website operated by other parties.

Such links are only provided on our website for the convenience of

the Client and Standard Chartered Bank does not control or endorse

such websites, and is not responsible for their contents.

The use of such website is also subject to the terms of use and

other terms and guidelines, if any, contained within each such

website. In the event that any of the terms contained herein

conflict with the terms of use or other terms and guidelines

contained within any such website, then the terms of use and other

terms and guidelines for such website shall prevail.

*SingPass holders with a MyInfo profile can use MyInfo

to automatically fill up the form. By clicking “Next”, you will

be re-directed to the MyInfo

portal, which is not owned or controlled by Standard Chartered

Bank (Singapore) Limited or any member of the Standard Chartered

Group (the “Bank”). The Bank bears no liability or

responsibility over your usage of the MyInfo portal.

*Please note that MyInfo is temporarily unavailable at the stipulated downtimes:

Mon, Tues, Thurs, Fri, Sat: 5:00AM to 5:30AM. Wed: 2:00AM

to 6:00AM. Sun: 2:00AM to 8:30AM

I am an existing Standard Chartered Current/Checking/Savings

Account holder

*SingPass holders with a MyInfo profile can use MyInfo

to automatically fill up the form. By clicking “Next”, you will

be re-directed to the MyInfo

portal, which is not owned or controlled by Standard Chartered

Bank (Singapore) Limited or any member of the Standard Chartered

Group (the “Bank”). The Bank bears no liability or

responsibility over your usage of the MyInfo portal.

*Please note that MyInfo is temporarily unavailable at the stipulated downtimes:

Mon, Tues, Thurs, Fri, Sat: 5:00AM to 5:30AM. Wed: 2:00AM

to 6:00AM. Sun: 2:00AM to 8:30AM

I am an existing Standard Chartered Current/Checking/Savings

Account holder

Why doing nothing may often be best during volatile times

From time to time, investment markets go through periods of uncertainty.

This could be due some poor economic news, a political crisis, something affecting a particular industry sector, or changes in government policy.

The sharp falls that can be experienced at such times are understandably unsettling for investors. They can even tempt some to change their long-term plan by selling their investments.

However, market volatility does tend to be short lived. Here are some reasons why doing nothing may often be best during times of volatility.

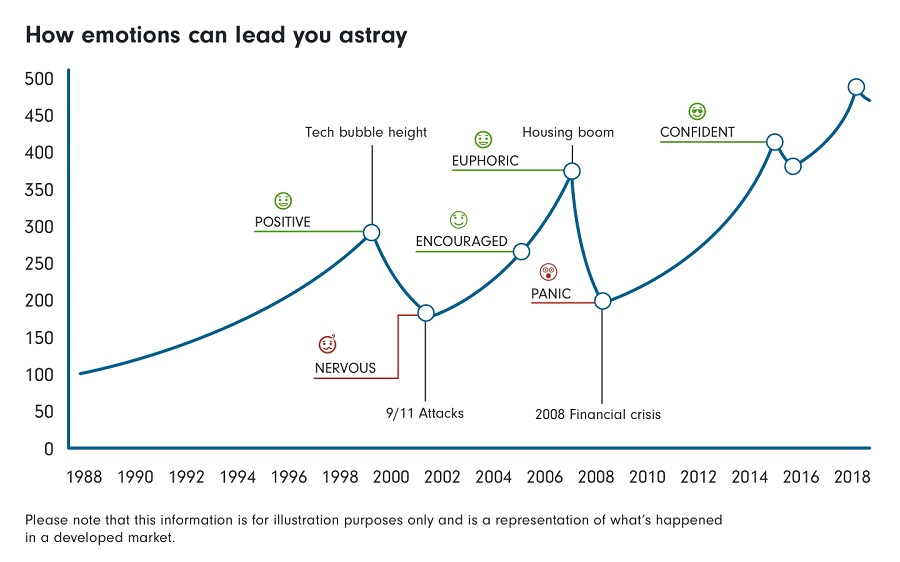

1. Emotions can lead you astray

When you see a sudden change in the stock market, you might feel tempted to rush into buying or selling stocks, either to ride a wave of growth or minimise losses.

However, instinctive reactions don’t always make for sound financial decisions. By acting too quickly you’re more likely to make costly mistakes, like selling low or buying too high.

It’s important to keep a cool head when the market is volatile and avoid being distracted by your emotions.

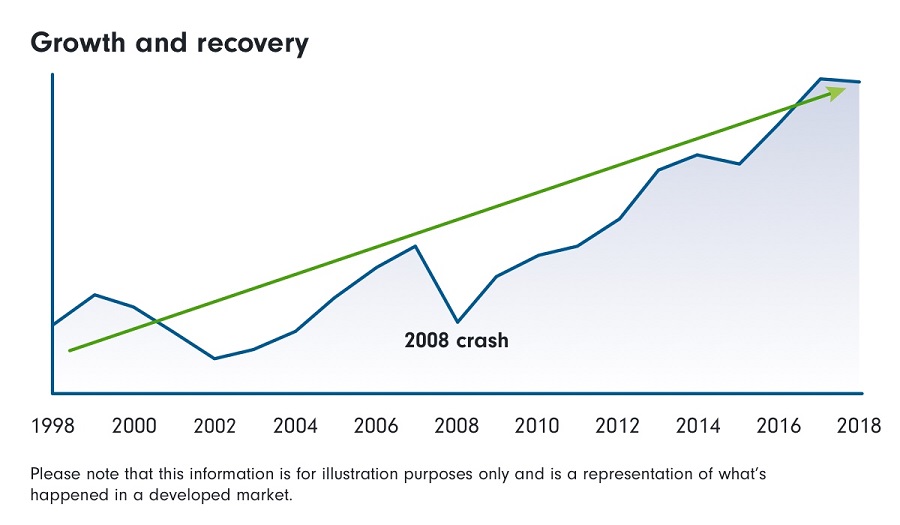

2. A stop/start approach is a lose-lose

One of the key principles of long-term investing is to stay invested, especially during times when investing can feel like a rollercoaster ride.

When markets are going up and down, spotting an opportunity and buying more during a correction is one thing, but jumping in and out of the market should generally be avoided.

History shows that sharp falls in stock markets tend to be concentrated in short periods of time. Similarly, the biggest gains are often clustered together, and it is quite common for a large gain to follow a big fall (or vice versa).

While most markets will experience periods of short-term volatility, over the long-term they generally maintain a steady, upwards path.

And those investors who remain invested will benefit the most from these long-term upward trends.

By moving too quickly to sell assets, you may run the risk of missing out on seeing your portfolio recover from falls, and even grow in value. Missing the best recovery and performance dates in the market can have a significant impact on your long-term return.

Though past performance is not a guide to the future, staying invested can be a way to capture as much growth from the market as possible.

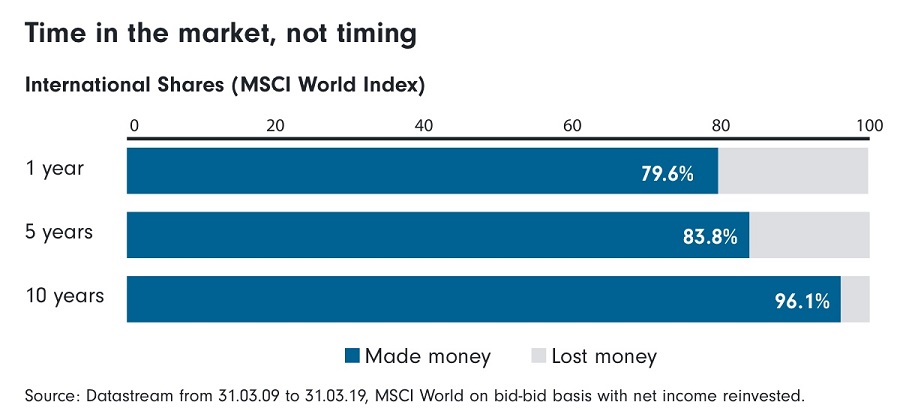

3. Reap the benefits of dollar cost averaging

Irrespective of your time horizon, it can make sense to invest a certain amount of money, an approach known as ‘dollar cost averaging’.

While it doesn’t promise a profit or protect against a market downturn, it does help you to reduce the risk of investing at a single point in time.

And although regular investing during a falling market may seem counter-intuitive to investors looking to limit their losses, it is precisely at this time when some of the best investments can be made, because asset prices are lower and will benefit from any market rebound.

This article is written by Fidelity International.

Disclaimer

This article is for general information only and it does not constitute an offer, recommendation or solicitation of an offer to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments, nor does it constitute any prediction of likely future movements in rates or prices or any representation that any such future movements will not exceed those shown in any illustration. This article has not been prepared for any particular person or class of persons and it has been prepared without regard to the specific investment objectives, financial situation or particular needs of any person, and does not constitute and should not be construed as investment advice nor an investment recommendation. Where the article describes any insurance product or service, it also does not constitute an offer, recommendation or solicitation of an offer to buy or sell any insurance product or service, nor is it intended to provide insurance or financial advice. You should seek advice from a licensed or an exempt financial adviser on the suitability of a product for you, taking into account these factors before making a commitment to purchase any product. In the event that you choose not to seek advice from a licensed or an exempt financial adviser, you should carefully consider whether the product is suitable for you.

Standard Chartered Bank (Singapore) Limited (the “Bank”) will not accept any responsibility or liability of any kind, with respect to the accuracy or completeness of the information herein. The Bank makes no representation or warranty of any kind, express, implied or statutory regarding this article or any information contained or referred to in this article. This article is distributed on the express understanding that, whilst the information in it is believed to be reliable, it has not been independently verified by the Bank.

The named contributor to the article (the “Contributor”) does not assume any duty to update any opinions or forward-looking statements, which are based on certain assumptions of future events and information available on the date hereof. There can be no assurance that forward-looking statements, if any, will materialise or the intended objectives or targets can be achieved. Whilst great care has been taken to ensure that the information contained herein is accurate and the data or information supplied by outside sources are reliable, the Contributor does not accept any responsibility or liability of any kind, with respect to the accuracy or completeness of the information herein. The distribution/dissemination of this article in certain jurisdictions may be restricted by law. The Contributor shall not be held liable as to how and where the Bank chooses to distribute or disseminate the article, in the event that the Bank acts or omits to act in willful default of the Contributor’s written notice to the Bank regarding such distribution or dissemination. Persons into whose possession this article may come are required to inform themselves of and comply with any relevant restrictions. Receipt of this article does not constitute an offer or solicitation by the Contributor in any jurisdiction in which such an offer is not authorised or to any person to whom it is unlawful to make such an offer or solicitation. The Contributor does not purport that it is duly licensed or registered to offer financial services of any kind in such jurisdictions.