27 March 2026

Weekly Market View

Getting closer, but not all clear

As the Middle East conflict enters its fifth week, the outlines of a potential resolution are beginning to emerge. The US has initiated ceasefire proposals, signalling that Washington is approaching its political and economic pain threshold.

However, Iran has publicly resisted these overtures, maintaining its blockade of the Strait of Hormuz and keeping energy prices elevated. In our view, a ceasefire and quasi-normalisation of traffic through the strait remains weeks away.

Given this, we remain invested in a well-diversified portfolio, while selectively capitalising on dislocations created by market volatility.

We would lean into the latest bond yield surge and average into bonds, especially in the US, where the Fed is likely to cut rates in H2 to revive a weak job market. We also see an opportunity to average into gold after the liquidity-driven sell-off.

Bullish global ex-US buyback equity theme – outperforms during rising stagflation risks

Bearish USD/JPY – strong wage negotiation outcome raises chance of BoJ rate hike

Add gold on dips – gold sales by some central banks likely temporary

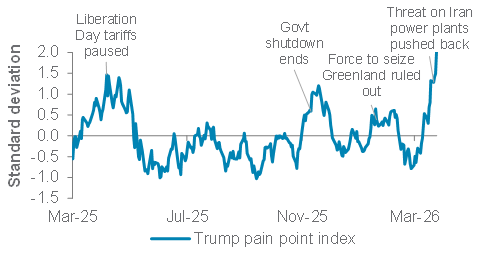

Charts of the week: Pain threshold

Our US ‘pain indicator’ has soared above levels that has previously led to a reversal in unpopular positions

US ‘pain indicator’*

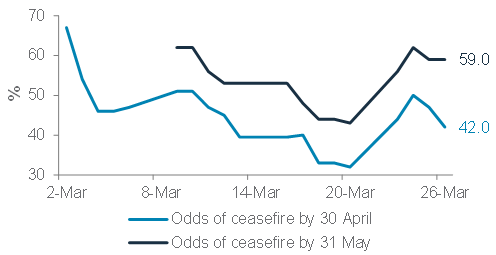

Polymarket odds of a US-Iran ceasefire by 30 April and 31 May

Source: Bloomberg, Standard Chartered

Editorial

Getting closer, but not all clear

Strategy summary: As the Middle East conflict enters its fifth week, the outlines of a potential resolution are beginning to emerge. The US has initiated ceasefire proposals, signalling that Washington is approaching its political and economic pain threshold. However, Iran has publicly resisted these overtures, maintaining its blockade of the Strait of Hormuz and keeping energy prices elevated. In our view, a ceasefire and quasi-normalisation of traffic through the strait remains weeks away.

Given this, we remain invested in a well-diversified portfolio, while selectively capitalising on dislocations created by market volatility. We would lean into the latest bond yield surge and average into bonds, especially in the US, where the Fed is likely to cut rates in H2 to revive a weak job market. We also see an opportunity to average into gold after the liquidity-driven sell-off.

The road to de-escalation: The emergence of the so-called “Trump put”, the propensity to reverse course when domestic pressures reach critical levels, has become apparent. President Trump’s approval ratings have fallen to their lowest point in his second term, while equity and bond markets have continued to deteriorate. Historically, the administration has reversed unpopular positions, including Liberation Day tariffs and threatening force to control Greenland, at pain indicator levels considerably below those seen today. The current trajectory makes a policy shift toward de-escalation arguably inevitable.

Depleted military capacity: On the military front, the capacity of both parties to sustain the conflict has been materially diminished. Iran’s conventional capabilities have been severely degraded, compelling a shift toward unconventional means, most notably drone operations, the frequency of which has declined markedly over the past week. Meanwhile, the US has reportedly exhausted several years’ worth of missile interceptor production within the opening days of the conflict, while its most advanced aircraft carrier has been withdrawn for repairs.

Global strain and the limits of Iranian leverage: While the global economy is beginning to exhibit signs of stress, the pressure has not yet reached the threshold required to compel Iran to the negotiating table. The ongoing release of 400mn barrels of oil reserves by developed economies and lifting of sanctions on some Russian/Iranian oil has relieved pressure for a few weeks. However, the OECD raised its inflation estimate for Group of 20 economies this year to 4%, while some energy-importing Emerging Markets have begun rationing energy supplies and curtailing activity. Iran is aware that its ability to sustain the blockade is finite. The prospect of global powers applying concerted pressure to reopen the strait is rising.

The principal downside risks to our base scenario remain: i) a near-term escalation, with the US reportedly considering sending another 10,000 troops to the Middle East, and ii) the possibility of intra-Iranian factional conflict, which could complicate safe passage through the strait even after a formal ceasefire. For the present, the latter risk appears contained.

Attractive risk-reward trade-off in bonds: The hawkish repricing of central bank rate expectations, driven by oil prices, has been excessive, in our view. Markets have largely priced in the near-term inflationary impact of higher energy costs, while under-estimating the medium-term drag on growth. The US job market is more fragile today than it was following the 2022 Ukraine conflict (US jobs report for March due next week). We expect the Fed to cut rates in the H2 this year. Thus, the risk profile for bonds is asymmetric: the US 10-year yield may rise a further 50-60bps in a near-term inflation spike, but could fall 200–300bps should job markets deteriorate sharply. Given this, we prefer to average into bonds with maturities of 5-7 years.

Adding gold on dips: The sharp sell-off in gold since the onset of the conflict, driven primarily by a dash for liquidity and profit-taking, has created a compelling entry point for medium-term investors. Gold has since rebounded from its 200-day moving average around USD 4,100/oz. Structural demand from central banks and investors should sustain, given rising geopolitical risks. We retain our 12-month price target of USD 5,750/oz.

— Rajat Bhattacharya

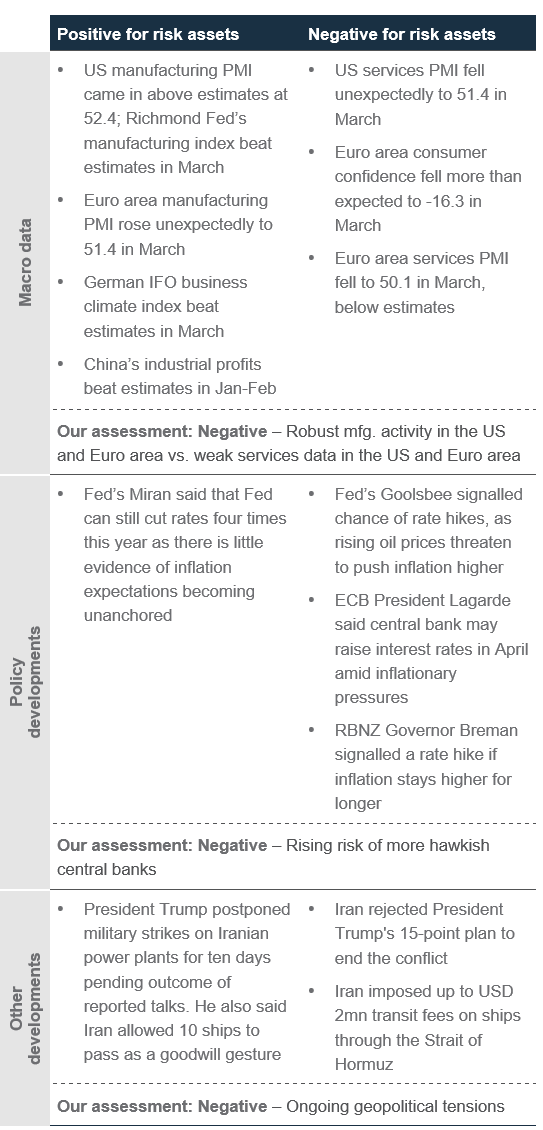

The weekly macro balance sheet

Our weekly net assessment: On balance, we see the past week’s data and policy as negative for risk assets in the near-term

(+) factors: Robust manufacturing activity in the US and Euro area

(-) factors: Weak services data in the US and Euro area; hawkish central banks; elevated geopolitical tensions

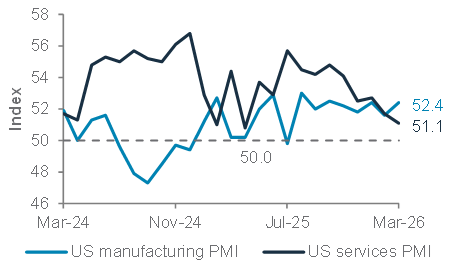

US manufacturing PMI rose to 52.4, marking an eighth straight month of improvement while the services’ PMI dropped to an 11-month low

US S&P manufacturing and services’ PMIs

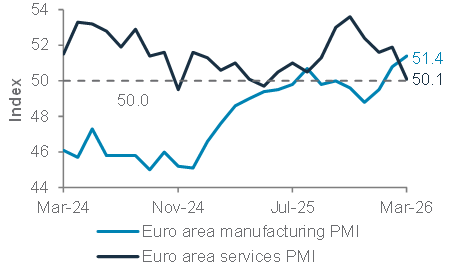

Euro area manufacturing PMI rose to a 45-month high, but the services sector PMI slowed sharply

Euro area S&P manufacturing and services’ PMIs

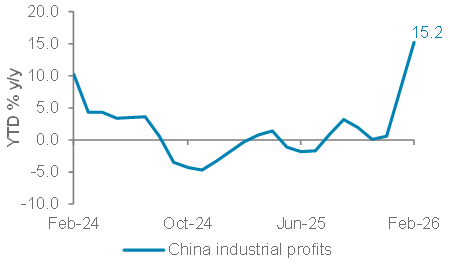

China industrial profits rose 15.2% in the first two months of 2026, significantly above the consensus of 0.6%

China industrial profit growth

Top client questions

Do you believe central banks will still be net buyers of gold?

Our view: While there are signs of some central bank gold sales recently, we believe these are temporary in nature. We expect Emerging Market (EM) central bank demand to still help push gold prices higher. We retain our 12-month USD 5,750 forecast.

Rationale: We have seen huge gold price volatility, in both directions, in 2026. After rallying almost 30% in January, it fell over 20% in two days and then almost 25% in three weeks in March, after the Middle East crisis began. Gold is now up about 2% year to date.

There is a lot of speculation that gold’s decline is due to central bank sales. Regular readers will be aware our bullish gold thesis is premised largely on the outlook for strong EM central bank demand. So, have things changed?

We believe this has been a perfect temporary storm for gold. First, we saw excessive positioning in gold, and then came the Middle East conflict, which led to significant portfolio losses and some margin calls.

For individual investors who needed to sell assets to create liquidity, gold could provide it while not crystalising a loss. This fits with the view that when people are worried about the future, they buy gold; when they are worried about the present, they sell gold.

The Middle East crisis, via higher oil prices, also increased currency and fiscal pressures in many countries. This likely led some countries to sell gold to prop up their own currencies and help protect economies and fiscal positions from sharply higher oil prices.

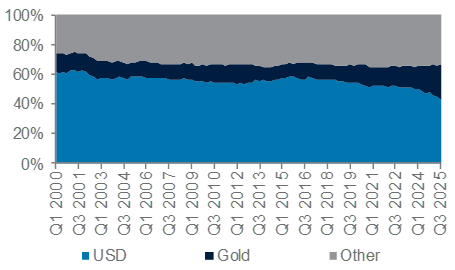

Finally, central banks with purchasing capacity were likely dissuaded from continued purchases by the sharp rise in prices in January. Of course, it is possible that some central banks will look at gold’s volatility and recalibrate long-term gold allocation targets. However, we see the EM central bank demand for alternatives to Developed Market (DM) bond markets generally, and USD assets in particular, as being undimmed, and maybe even increased, following the Middle East conflict.

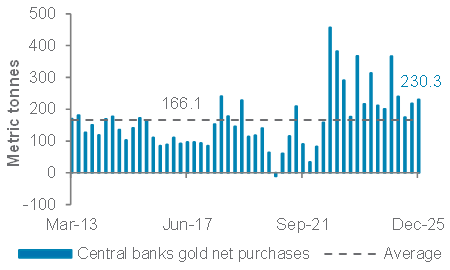

So far, the numbers of central bank gold liquidation being touted look small relative to the net 250 tonnes being bought on average every quarter by central banks since the Russian central bank was sanctioned in 2022. Therefore, we continue to expect this to drive gold prices higher in the coming months and years. We have a 12-month target of USD 5,750/oz.

However, the path is likely to be volatile and the World Gold Council’s quarterly demand data, likely out in April, will be interesting reading. We expect USD 4,100/oz to hold on the downside.

— Steve Brice, Global Chief Investment Officer

Central banks have dramatically accelerated gold purchases since the Russian central banks were sanctioned in 2022

Global central bank demand, net quarterly purchases

Central banks still keen to diversify away from USD assets in their reserves

Gold as a percentage of central bank reserves

Top client questions (cont’d)

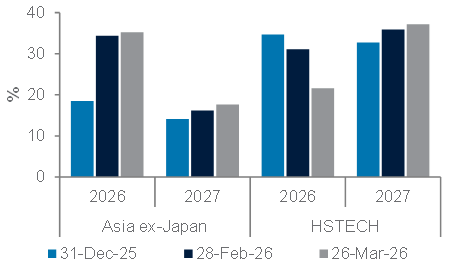

What is the impact of the Middle East conflict and China’s tech earnings on Asia ex-Japan (AxJ) equities?

Our view: AxJ earnings trend remains strong. We are Overweight AxJ, especially Taiwan equities. Hang Seng Tech Index (HSTECH) earnings face near-term weakness, but we remain positive on its growth outlook.

Rationale: AxJ equities’ earnings growth estimates rose strongly in early 2026. Since the Middle East conflict began, 2026 growth expectations have stalled (from 34.3% to 35.2%), while 2027 growth estimates have continued to rise (from 16.2% to 17.6%). Although AxJ relies heavily on Middle Eastern oil supply, the earnings impact remains limited. Positive growth trend remains, led by semiconductor and memory chips amid strong AI capital expenditure (capex). We’re Overweight Taiwan equities, mostly due to the chip industry.

Major Chinese internet and tech firms’ earnings show heavy AI investment, eroding near-term profits. High memory chip prices have raised tech hardware costs. 2026 HSTECH index earnings growth has fallen from 34.7% to 21.5%. However, monetisation efforts could materialise in 2027, with growth expected to rise from 32.7% to 37.2%. We have a positive HSTECH growth outlook, given reasonable valuations.

— Fook Hien Yap, Senior Investment Strategist

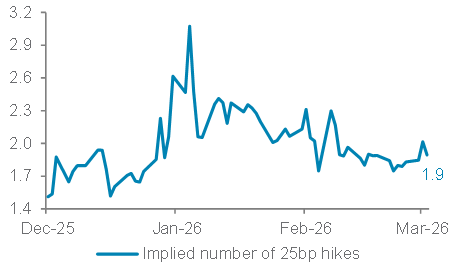

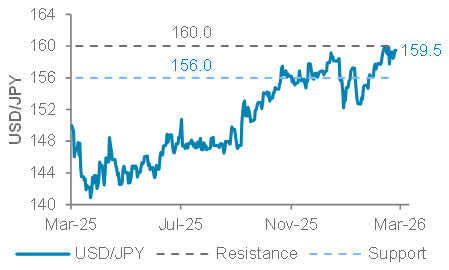

How might Japan’s ‘Shunto’ results and inflation affect the Bank of Japan’s (BoJ’s) rate path, the JPY and Japan equities?

Our view: Strong ‘Shunto’ wage outcomes increase likelihood of an early BoJ rate hike. USD/JPY outlook remains bearish. We recommend maintaining a core allocation to Japan equities.

Rationale: Stronger-than-expected January ‘Shunto’ (Japan’s annual spring wage negotiations) wage gains reinforce the BoJ’s assessment that the wage-price inflation cycle is gaining traction. Concurrently, the Iran crisis is adding inflationary pressure. These factors increase the risk of a BoJ rate hike before H2 2026. However, oil prices will stabilise if crisis ends, containing inflationary impact.

Despite robust wage growth, we believe the BoJ prefers a sustained domestic consumption recovery before further policy normalisation. USD/JPY upside seems limited around 160 due to FX intervention risk. We expect the pair to test support at 156. Wage gains and reflation are likely to support Japan equities earnings growth. High energy prices are a near-term headwind, but manageable if the conflict eases soon. Thereafter, the Takaichi government’s fiscal stimulus should be positive for corporate Japan.

— Ray Heung, Senior Investment Strategist

— Iris Yuen, Investment Strategist

AxJ earnings growth revised higher since the start of 2026. Meanwhile, HSTECH has seen 2026 growth estimates cut, 2027 estimates upgraded

Consensus earnings growth for MSCI AxJ and Hang Seng Tech indices on various dates

Markets expect two 25bps BoJ rate hikes by end- 2026 – in line with our expectations

Market-implied number of 25bps hikes by year-end

USD/JPY is exposed to downside risk

USD/JPY and technicals

Top client questions (cont’d)

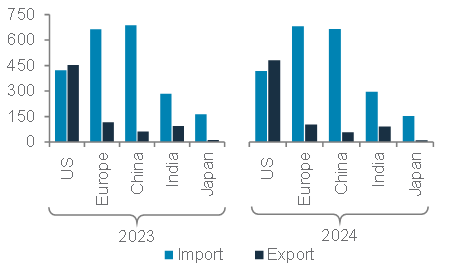

How would damages to oil and gas (O&G) infrastructure change your long-term view on oil and economic growth, especially of the net importing regions?

Our view: Persistent damage to infrastructure, not temporary disruptions, drives a ‘higher-for-longer’ oil regime, creating an asymmetric growth impact for import-dependent economies.

Rationale: The Strait of Hormuz closure – removing c.16mb/d of crude flows – represents a supply shock. However, historically, it is not the disruption itself, but the persistence of supply impairment that drives long-term macro-outcomes. Temporary shocks are absorbed through inventories and policy responses, but damage to O&G infrastructure raises the marginal cost of supply and reduces spare capacity, reinforcing a ‘higher-for-longer’ oil price environment.

The macro impact is highly asymmetric. Net energy importers, especially in Asia and Europe, face significant trade shock risk, with higher oil prices feeding into inflation, currency pressure and growth. Asia’s exposure is structural, given its reliance on imported crude, while Europe’s vulnerability is compounded by limited domestic energy capacity, as seen during the 2022 energy crisis.

The US, while historically very sensitive to oil shocks, has seen reduced energy intensity and now benefits from its net petroleum exporter status. This provides a partial offset through the domestic energy sector, although higher fuel costs still weigh on consumption and financial conditions. We recommend inflation hedges, such as US Treasury Inflation-Protected Securities (TIPS), which offset upside inflation risks driven by sustained oil price pressures

— Anthony Naab, CFA, Investment Strategist

Elevated oil prices would lead to asymmetric growth impact, disproportionately weighing on import-dependent economies relative to the US

Oil trade (mn tonnes), 2023 – 2024

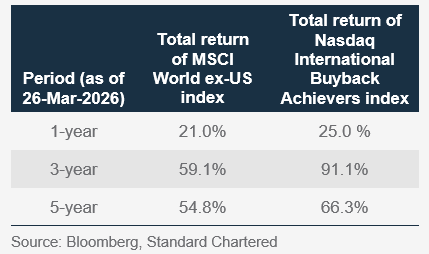

Has the ‘buyback’ equity theme proven to outperform at times of stagflation and/or recession? What is the rationale of excluding the US from this theme?

Our view: Global ex-US buyback outperforms at times of rising stagflation risk.

Rationale: There is no clear evidence the ‘buyback’ theme consistently outperforms the MSCI ACWI ex‑USA Index during recessions, based on the sole post‑2008 Global Financial Crisis 2020 pandemic episode. That said, the theme has delivered superior performance over the past one, three and five years – periods that broadly coincided with elevated stagflation concerns. Our base case remains a ‘soft landing’, with recession risks contained despite ongoing geopolitical uncertainties. Resilient economic growth should continue to support shareholder returns.

Beyond signalling management confidence, buybacks help cushion portfolios against volatility by reducing share supply, offering a stabilising and defensive exposure to portfolios while retaining participation in equity upside.

Global ex-US buyback equity theme outperforms at times of elevated stagflation risk

1-, 3- and 5-year performance of MSCI World ex-US vs Nasdaq International Buyback Achievers Net Total Return indices

The strategy focuses on companies that have reduced shares outstanding by at least 5% over the past year.

We favour non‑US regions, given more pronounced corporate activity. In Europe (c.52% of the theme), members of the Stoxx Europe 600 Index announced a record EUR 85.7bn in share repurchases in January-February 2026 (source: Barclays). A sizeable pipeline of approved buyback programmes yet to be executed should continue to support the theme’s upside in Q2 and beyond. This contrasts with the US, where corporate cash flows are increasingly directed towards AI‑related capital expenditure (capex), limiting near‑term buyback momentum.

— Michelle Kam, CFA, Investment Strategist

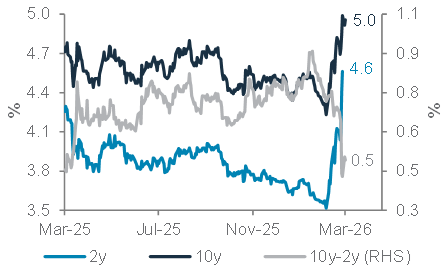

The UK 10-year government bond (gilt) yield hit the highest level since Q3 2008. Will this bond market sell-off continue? What are the implications for the GBP?

Our view: GBP-based investors can consider gradually scaling into UK gilts, focusing on 5-7-year maturities. Our negative GBP/USD view means gilts are still unattractive for USD-based investors. GBP/USD faces downside risk, with support at 1.3220

Rationale: The UK imports over 40% of its energy needs. The Middle East conflict is thus expected to add to inflationary pressures. 10-year gilt yields briefly breached 5% before paring gains and have since settled below 5%. Our base case of a conflict de‑escalation in the coming weeks – supported by reports of US-Iran ceasefire talks – implies the inflationary impact is likely to be more transient.

While the UK has one of the highest government debt‑to‑GDP ratios, last autumn’s fiscal budget provided reassurance around fiscal discipline. This should help anchor long‑end yield expectations. Market volatility is likely to persist until geopolitical risks subside, reinforcing our preference for GBP-based investors to scale into gilts, rather than adopt a fully front‑loaded approach. We emphasise maintaining exposure in the 5-7-year maturity bucket, which we believe offers the most attractive risk‑reward for GBP-based investors.

UK inflation stands at 3% y/y, remaining above the Bank of England’s (BoE’s) 2% target, but is relatively stable, likely reducing the urgency for immediate interest-rate adjustments. We see renewed GBP/USD selling pressure emerging amid concerns around growth and consumption, as recent data indicates a surge in input prices.

— Ray Heung, Senior Investment Strategist

— Iris Yuen, Investment Strategist

UK bond volatility to persist but yields to decline as Middle East conflict de-escalates. Short-end yields are likely to fall more than long-end yields

UK 10- and 2-year government bond yields and their interest rate differential

We are bearish GBP/USD, with support at 1.3220

GBP/USD and technicals

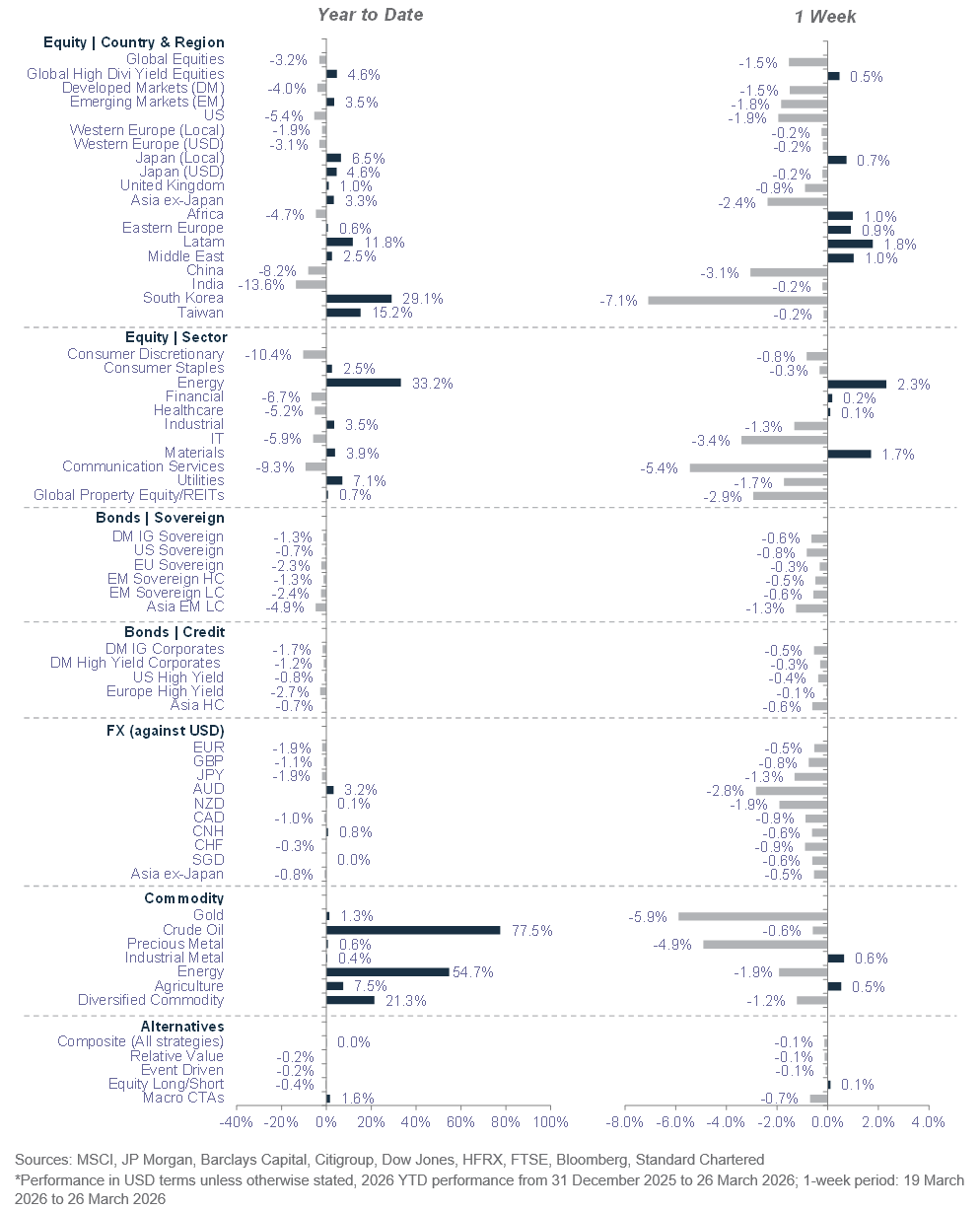

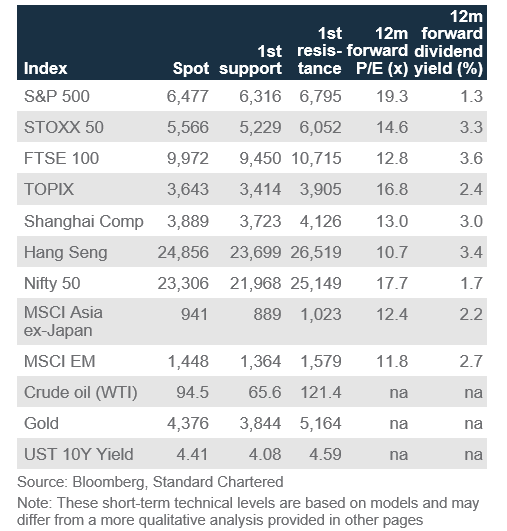

Market performance summary*

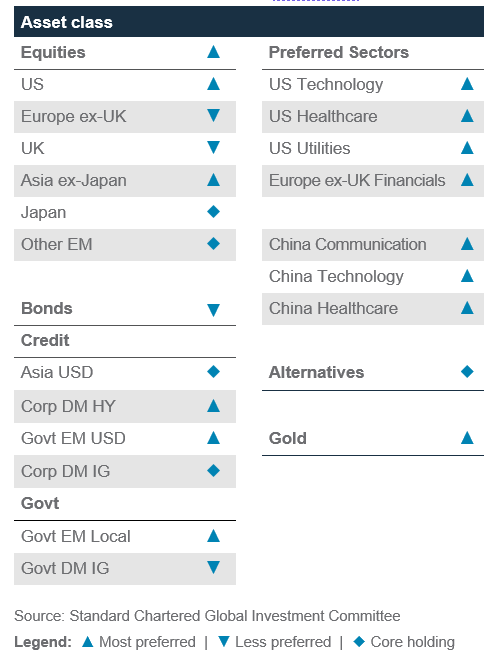

Our 12-month asset class views at a glance

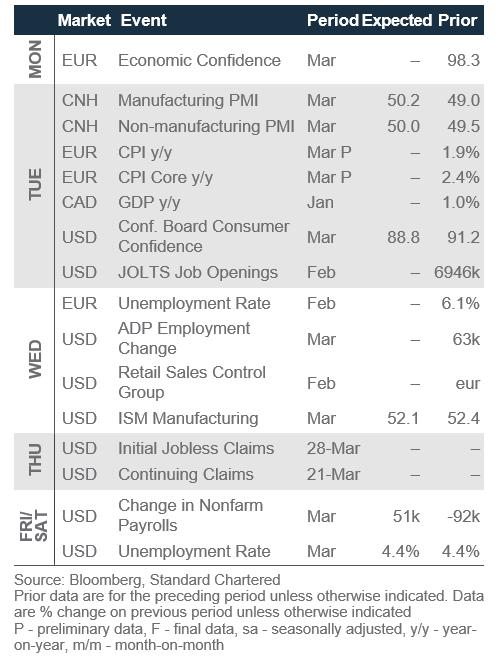

Economic and market calendar

The S&P500 has next interim resistance at 6,795

Technical indicators for key markets as of 26 Mar close

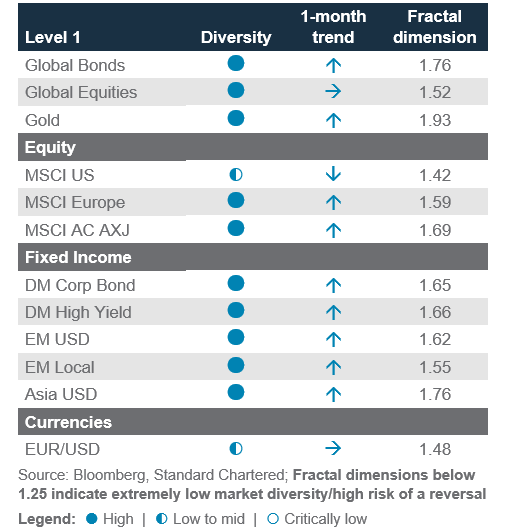

Investor diversity has normalised across asset classes

Our proprietary market diversity indicators as of 26 Mar close

Disclosure

This document is confidential and may also be privileged. If you are not the intended recipient, please destroy all copies and notify the sender immediately. This document is being distributed for general information only and is subject to the relevant disclaimers available at our Standard Chartered website under Regulatory disclosures. It is not and does not constitute research material, independent research, an offer, recommendation or solicitation to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments. This document is for general evaluation only. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person or class of persons and it has not been prepared for any particular person or class of persons. You should not rely on any contents of this document in making any investment decisions. Before making any investment, you should carefully read the relevant offering documents and seek independent legal, tax and regulatory advice. In particular, we recommend you to seek advice regarding the suitability of the investment product, taking into account your specific investment objectives, financial situation or particular needs, before you make a commitment to purchase the investment product. Opinions, projections and estimates are solely those of SC at the date of this document and subject to change without notice. Past performance is not indicative of future results and no representation or warranty is made regarding future performance. The value of investments, and the income from them, can go down as well as up, and you may not recover the amount of your original investment. You are not certain to make a profit and may lose money. Any forecast contained herein as to likely future movements in rates or prices or likely future events or occurrences constitutes an opinion only and is not indicative of actual future movements in rates or prices or actual future events or occurrences (as the case may be). This document must not be forwarded or otherwise made available to any other person without the express written consent of the Standard Chartered Group (as defined below). Standard Chartered Bank is incorporated in England with limited liability by Royal Charter 1853 Reference Number ZC18. The Principal Office of the Company is situated in England at 1 Basinghall Avenue, London, EC2V 5DD. Standard Chartered Bank is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and Prudential Regulation Authority. Standard Chartered PLC, the ultimate parent company of Standard Chartered Bank, together with its subsidiaries and affiliates (including each branch or representative office), form the Standard Chartered Group. Standard Chartered Private Bank is the private banking division of Standard Chartered. Private banking activities may be carried out internationally by different legal entities and affiliates within the Standard Chartered Group (each an “SC Group Entity”) according to local regulatory requirements. Not all products and services are provided by all branches, subsidiaries and affiliates within the Standard Chartered Group. Some of the SC Group Entities only act as representatives of Standard Chartered Private Bank and may not be able to offer products and services or offer advice to clients.

Copyright © 2026, Accounting Research & Analytics, LLC d/b/a CFRA (and its affiliates, as applicable). Reproduction of content provided by CFRA in any form is prohibited except with the prior written permission of CFRA. CFRA content is not investment advice and a reference to or observation concerning a security or investment provided in the CFRA SERVICES is not a recommendation to buy, sell or hold such investment or security or make any other investment decisions. The CFRA content contains opinions of CFRA based upon publicly-available information that CFRA believes to be reliable and the opinions are subject to change without notice. This analysis has not been submitted to, nor received approval from, the United States Securities and Exchange Commission or any other regulatory body. While CFRA exercised due care in compiling this analysis, CFRA, ITS THIRD-PARTY SUPPLIERS, AND ALL RELATED ENTITIES SPECIFICALLY DISCLAIM ALL WARRANTIES, EXPRESS OR IMPLIED, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE, to the full extent permitted by law, regarding the accuracy, completeness, or usefulness of this information and assumes no liability with respect to the consequences of relying on this information for investment or other purposes. No content provided by CFRA (including ratings, credit-related analyses and data, valuations, model, software or other application or output therefrom) or any part thereof may be modified, reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval system, without the prior written permission of CFRA, and such content shall not be used for any unlawful or unauthorized purposes. CFRA and any third-party providers, as well as their directors, officers, shareholders, employees or agents do not guarantee the accuracy, completeness, timeliness or availability of such content. In no event shall CFRA, its affiliates, or their third-party suppliers be liable for any direct, indirect, special, or consequential damages, costs, expenses, legal fees, or losses (including lost income or lost profit and opportunity costs) in connection with a subscriber’s, subscriber’s customer’s, or other’s use of CFRA’s content.

Market Abuse Regulation (MAR) Disclaimer

Banking activities may be carried out internationally by different branches, subsidiaries and affiliates within the Standard Chartered Group according to local regulatory requirements. Opinions may contain outright “buy”, “sell”, “hold” or other opinions. The time horizon of this opinion is dependent on prevailing market conditions and there is no planned frequency for updates to the opinion. This opinion is not independent of Standard Chartered Group’s trading strategies or positions. Standard Chartered Group and/or its affiliates or its respective officers, directors, employee benefit programmes or employees, including persons involved in the preparation or issuance of this document may at any time, to the extent permitted by applicable law and/or regulation, be long or short any securities or financial instruments referred to in this document or have material interest in any such securities or related investments. Therefore, it is possible, and you should assume, that Standard Chartered Group has a material interest in one or more of the financial instruments mentioned herein. Please refer to our Standard Chartered website under Regulatory disclosures for more detailed disclosures, including past opinions/ recommendations in the last 12 months and conflict of interests, as well as disclaimers. A covering strategist may have a financial interest in the debt or equity securities of this company/issuer. All covering strategist are licensed to provide investment recommendations under Monetary Authority of Singapore or Hong Kong Monetary Authority. This document must not be forwarded or otherwise made available to any other person without the express written consent of Standard Chartered Group.

Sustainable Investments

Any ESG data used or referred to has been provided by Morningstar, Sustainalytics, MSCI or Bloomberg. Refer to 1) Morningstar website under Sustainable Investing, 2) Sustainalytics website under ESG Risk Ratings, 3) MCSI website under ESG Business Involvement Screening Research and 4) Bloomberg green, social & sustainability bonds guide for more information. The ESG data is as at the date of publication based on data provided, is for informational purpose only and is not warranted to be complete, timely, accurate or suitable for a particular purpose, and it may be subject to change. Sustainable Investments (SI): This refers to funds that have been classified as ‘ESG Intentional Investments – Overall’ by Morningstar. SI funds have explicitly stated in their prospectus and regulatory filings that they either incorporate ESG factors into the investment process or have a thematic focus on the environment, gender diversity, low carbon, renewable energy, water or community development. For equity, it refers to shares/stocks issued by companies with Sustainalytics ESG Risk Rating of Low/Negligible. For bonds, it refers to debt instruments issued by issuers with Sustainalytics ESG Risk Rating of Low/Negligible, and/or those being certified green, social, sustainable bonds by Bloomberg. For structured products, it refers to products that are issued by any issuer who has a Sustainable Finance framework that aligns with Standard Chartered’s Green and Sustainable Product Framework, with underlying assets that are part of the Sustainable Investment universe or separately approved by Standard Chartered’s Sustainable Finance Governance Committee. Sustainalytics ESG risk ratings shown are factual and are not an indicator that the product is classified or marketed as “green”, “sustainable” or similar under any particular classification system or framework.

Country/Market Specific Disclosures

Bahrain: This document is being distributed in Bahrain by Standard Chartered Bank, Bahrain Branch, having its address at P.O. 29, Manama, Kingdom of Bahrain, is a branch of Standard Chartered Bank and is licensed by the Central Bank of Bahrain as a conventional retail bank. Botswana: This document is being distributed in Botswana by, and is attributable to, Standard Chartered Bank Botswana Limited which is a financial institution licensed under the Section 6 of the Banking Act CAP 46.04 and is listed in the Botswana Stock Exchange. Brunei Darussalam: This document is being distributed in Brunei Darussalam by, and is attributable to, Standard Chartered Bank (Brunei Branch) | Registration Number RFC/61 and Standard Chartered Securities (B) Sdn Bhd | Registration Number RC20001003. Standard Chartered Bank is incorporated in England with limited liability by Royal Charter 1853 Reference Number ZC18. Standard Chartered Securities (B) Sdn Bhd is a limited liability company registered with the Registry of Companies with Registration Number RC20001003 and licensed by Brunei Darussalam Central Bank as a Capital Markets Service License Holder with License Number BDCB/R/CMU/S3-CL and it is authorised to conduct Islamic investment business through an Islamic window. China Mainland: This document is being distributed in China by, and is attributable to, Standard Chartered Bank (China) Limited which is mainly regulated by National Financial Regulatory Administration (NFRA), State Administration of Foreign Exchange (SAFE), and People’s Bank of China (PBOC). Hong Kong: In Hong Kong, this document, except for any portion advising on or facilitating any decision on futures contracts trading, is distributed by Standard Chartered Bank (Hong Kong) Limited (“SCBHK”), a subsidiary of Standard Chartered PLC. SCBHK has its registered address at 32/F, Standard Chartered Bank Building, 4-4A Des Voeux Road Central, Hong Kong and is regulated by the Hong Kong Monetary Authority and registered with the Securities and Futures Commission (“SFC”) to carry on Type 1 (dealing in securities), Type 4 (advising on securities), Type 6 (advising on corporate finance) and Type 9 (asset management) regulated activity under the Securities and Futures Ordinance (Cap. 571) (“SFO”) (CE No. AJI614). The contents of this document have not been reviewed by any regulatory authority in Hong Kong and you are advised to exercise caution in relation to any offer set out herein. If you are in doubt about any of the contents of this document, you should obtain independent professional advice. Any product named herein may not be offered or sold in Hong Kong by means of any document at any time other than to “professional investors” as defined in the SFO and any rules made under that ordinance. In addition, this document may not be issued or possessed for the purposes of issue, whether in Hong Kong or elsewhere, and any interests may not be disposed of, to any person unless such person is outside Hong Kong or is a “professional investor” as defined in the SFO and any rules made under that ordinance, or as otherwise may be permitted by that ordinance. In Hong Kong, Standard Chartered Private Bank is the private banking division of SCBHK, a subsidiary of Standard Chartered PLC. Ghana: Standard Chartered Bank Ghana Limited accepts no liability and will not be liable for any loss or damage arising directly or indirectly (including special, incidental or consequential loss or damage) from your use of these documents. Past performance is not indicative of future results and no representation or warranty is made regarding future performance. You should seek advice from a financial adviser on the suitability of an investment for you, taking into account these factors before making a commitment to invest in an investment. To unsubscribe from receiving further updates, please send an email to feedback.ghana@sc.com. Please do not reply to this email. Call our Priority Banking on 0302610750 for any questions or service queries. You are advised not to send any confidential and/or important information to Standard Chartered via e-mail, as Standard Chartered makes no representations or warranties as to the security or accuracy of any information transmitted via e-mail. Standard Chartered shall not be responsible for any loss or damage suffered by you arising from your decision to use e-mail to communicate with the Bank. India: This document is being distributed in India by Standard Chartered in its capacity as a distributor of mutual funds and referrer of any other third party financial products. Standard Chartered does not offer any ‘Investment Advice’ as defined in the Securities and Exchange Board of India (Investment Advisers) Regulations, 2013 or otherwise. Services/products related securities business offered by Standard Charted are not intended for any person, who is a resident of any jurisdiction, the laws of which imposes prohibition on soliciting the securities business in that jurisdiction without going through the registration requirements and/or prohibit the use of any information contained in this document. Indonesia: This document is being distributed in Indonesia by Standard Chartered Bank, Indonesia branch, which is a financial institution licensed and supervised by Otoritas Jasa Keuangan (Financial Service Authority) and Bank Indonesia. Jersey: In Jersey, Standard Chartered Private Bank is the Registered Business Name of the Jersey Branch of Standard Chartered Bank. The Jersey Branch of Standard Chartered Bank is regulated by the Jersey Financial Services Commission. Copies of the latest audited accounts of Standard Chartered Bank are available from its principal place of business in Jersey: PO Box 80, 15 Castle Street, St Helier, Jersey JE4 8PT. Standard Chartered Bank is incorporated in England with limited liability by Royal Charter in 1853 Reference Number ZC 18. The Principal Office of the Company is situated in England at 1 Basinghall Avenue, London, EC2V 5DD. Standard Chartered Bank is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and Prudential Regulation Authority. The Jersey Branch of Standard Chartered Bank is also an authorised financial services provider under license number 44946 issued by the Financial Sector Conduct Authority of the Republic of South Africa. Jersey is not part of the United Kingdom and all business transacted with Standard Chartered Bank, Jersey Branch and other SC Group Entity outside of the United Kingdom, are not subject to some or any of the investor protection and compensation schemes available under United Kingdom law. Kenya: This document is being distributed in Kenya by and is attributable to Standard Chartered Bank Kenya Limited. Investment Products and Services are distributed by Standard Chartered Investment Services Limited, a wholly owned subsidiary of Standard Chartered Bank Kenya Limited that is licensed by the Capital Markets Authority in Kenya, as a Fund Manager. Standard Chartered Bank Kenya Limited is regulated by the Central Bank of Kenya. Malaysia: This document is being distributed in Malaysia by Standard Chartered Bank Malaysia Berhad (“SCBMB”). Recipients in Malaysia should contact SCBMB in relation to any matters arising from, or in connection with, this document. This document has not been reviewed by the Securities Commission Malaysia. The product lodgement, registration, submission or approval by the Securities Commission of Malaysia does not amount to nor indicate recommendation or endorsement of the product, service or promotional activity. Investment products are not deposits and are not obligations of, not guaranteed by, and not protected by SCBMB or any of the affiliates or subsidiaries, or by Perbadanan Insurans Deposit Malaysia, any government or insurance agency. Investment products are subject to investment risks, including the possible loss of the principal amount invested. SCBMB expressly disclaim any liability and responsibility for any loss arising directly or indirectly (including special, incidental or consequential loss or damage) arising from the financial losses of the Investment Products due to market condition. Nigeria: This document is being distributed in Nigeria by Standard Chartered Bank Nigeria Limited (SCB Nigeria), a bank duly licensed and regulated by the Central Bank of Nigeria. SCB Nigeria accepts no liability for any loss or damage arising directly or indirectly (including special, incidental or consequential loss or damage) from your use of these documents. You should seek advice from a financial adviser on the suitability of an investment for you, taking into account these factors before making a commitment to invest in an investment. To unsubscribe from receiving further updates, please send an email to clientcare.ng@sc.com requesting to be removed from our mailing list. Please do not reply to this email. Call our Priority Banking on 02 012772514 for any questions or service queries. SCB Nigeria shall not be responsible for any loss or damage arising from your decision to send confidential and/or important information to Standard Chartered via e-mail. SCB Nigeria makes no representations or warranties as to the security or accuracy of any information transmitted via e-mail. Pakistan: This document is being distributed in Pakistan by, and attributable to Standard Chartered Bank (Pakistan) Limited having its registered office at PO Box 5556, I.I Chundrigar Road Karachi, which is a banking company registered with State Bank of Pakistan under Banking Companies Ordinance 1962 and is also having licensed issued by Securities & Exchange Commission of Pakistan for Security Advisors. Standard Chartered Bank (Pakistan) Limited acts as a distributor of mutual funds and referrer of other third-party financial products. Singapore: This document is being distributed in Singapore by, and is attributable to, Standard Chartered Bank (Singapore) Limited (Registration No. 201224747C/ GST Group Registration No. MR-8500053-0, “SCBSL”). Recipients in Singapore should contact SCBSL in relation to any matters arising from, or in connection with, this document. SCBSL is an indirect wholly owned subsidiary of Standard Chartered Bank and is licensed to conduct banking business in Singapore under the Singapore Banking Act, 1970. Standard Chartered Private Bank is the private banking division of SCBSL. IN RELATION TO ANY SECURITY OR SECURITIES-BASED DERIVATIVES CONTRACT REFERRED TO IN THIS DOCUMENT, THIS DOCUMENT, TOGETHER WITH THE ISSUER DOCUMENTATION, SHALL BE DEEMED AN INFORMATION MEMORANDUM (AS DEFINED IN SECTION 275 OF THE SECURITIES AND FUTURES ACT, 2001 (“SFA”)). THIS DOCUMENT IS INTENDED FOR DISTRIBUTION TO ACCREDITED INVESTORS, AS DEFINED IN SECTION 4A(1)(a) OF THE SFA, OR ON THE BASIS THAT THE SECURITY OR SECURITIES-BASED DERIVATIVES CONTRACT MAY ONLY BE ACQUIRED AT A CONSIDERATION OF NOT LESS THAN S$200,000 (OR ITS EQUIVALENT IN A FOREIGN CURRENCY) FOR EACH TRANSACTION. Further, in relation to any security or securities-based derivatives contract, neither this document nor the Issuer Documentation has been registered as a prospectus with the Monetary Authority of Singapore under the SFA. Accordingly, this document and any other document or material in connection with the offer or sale, or invitation for subscription or purchase, of the product may not be circulated or distributed, nor may the product be offered or sold, or be made the subject of an invitation for subscription or purchase, whether directly or indirectly, to persons other than a relevant person pursuant to section 275(1) of the SFA, or any person pursuant to section 275(1A) of the SFA, and in accordance with the conditions specified in section 275 of the SFA, or pursuant to, and in accordance with the conditions of, any other applicable provision of the SFA. In relation to any collective investment schemes referred to in this document, this document is for general information purposes only and is not an offering document or prospectus (as defined in the SFA). This document is not, nor is it intended to be (i) an offer or solicitation of an offer to buy or sell any capital markets product; or (ii) an advertisement of an offer or intended offer of any capital markets product. Deposit Insurance Scheme: Singapore dollar deposits of non-bank depositors are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured. This advertisement has not been reviewed by the Monetary Authority of Singapore. Taiwan: SC Group Entity or Standard Chartered Bank (Taiwan) Limited (“SCB (Taiwan)”) may be involved in the financial instruments contained herein or other related financial instruments. The author of this document may have discussed the information contained herein with other employees or agents of SC or SCB (Taiwan). The author and the above-mentioned employees of SC or SCB (Taiwan) may have taken related actions in respect of the information involved (including communication with customers of SC or SCB (Taiwan) as to the information contained herein). The opinions contained in this document may change, or differ from the opinions of employees of SC or SCB (Taiwan). SC and SCB (Taiwan) will not provide any notice of any changes to or differences between the above-mentioned opinions. This document may cover companies with which SC or SCB (Taiwan) seeks to do business at times and issuers of financial instruments. Therefore, investors should understand that the information contained herein may serve as specific purposes as a result of conflict of interests of SC or SCB (Taiwan). SC, SCB (Taiwan), the employees (including those who have discussions with the author) or customers of SC or SCB (Taiwan) may have an interest in the products, related financial instruments or related derivative financial products contained herein; invest in those products at various prices and on different market conditions; have different or conflicting interests in those products. The potential impacts include market makers’ related activities, such as dealing, investment, acting as agents, or performing financial or consulting services in relation to any of the products referred to in this document. UAE: DIFC – Standard Chartered Bank is incorporated in England with limited liability by Royal Charter 1853 Reference Number ZC18.The Principal Office of the Company is situated in England at 1 Basinghall Avenue, London, EC2V 5DD. Standard Chartered Bank is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and Prudential Regulation Authority. Standard Chartered Bank, Dubai International Financial Centre having its offices at Dubai International Financial Centre, Building 1, Gate Precinct, P.O. Box 999, Dubai, UAE is a branch of Standard Chartered Bank and is regulated by the Dubai Financial Services Authority (“DFSA”). This document is intended for use only by Professional Clients and is not directed at Retail Clients as defined by the DFSA Rulebook. In the DIFC we are authorised to provide financial services only to clients who qualify as Professional Clients and Market Counterparties and not to Retail Clients. As a Professional Client you will not be given the higher retail client protection and compensation rights and if you use your right to be classified as a Retail Client we will be unable to provide financial services and products to you as we do not hold the required license to undertake such activities. For Islamic transactions, we are acting under the supervision of our Shariah Supervisory Committee. Relevant information on our Shariah Supervisory Committee is currently available on the Standard Chartered Bank website in the Islamic banking section. For residents of the UAE – Standard Chartered UAE (“SC UAE”) is licensed by the Central Bank of the U.A.E. SC UAE is licensed by Securities and Commodities Authority to practice Promotion Activity. SC UAE does not provide financial analysis or consultation services in or into the UAE within the meaning of UAE Securities and Commodities Authority Decision No. 48/r of 2008 concerning financial consultation and financial analysis. Uganda: Our Investment products and services are distributed by Standard Chartered Bank Uganda Limited, which is licensed by the Capital Markets Authority as an investment adviser. United Kingdom: In the UK, Standard Chartered Bank is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and Prudential Regulation Authority. This communication has been approved by Standard Chartered Bank for the purposes of Section 21 (2) (b) of the United Kingdom’s Financial Services and Markets Act 2000 (“FSMA”) as amended in 2010 and 2012 only. Standard Chartered Bank (trading as Standard Chartered Private Bank) is also an authorised financial services provider (license number 45747) in terms of the South African Financial Advisory and Intermediary Services Act, 2002. The Materials have not been prepared in accordance with UK legal requirements designed to promote the independence of investment research, and that it is not subject to any prohibition on dealing ahead of the dissemination of investment research. Vietnam: This document is being distributed in Vietnam by, and is attributable to, Standard Chartered Bank (Vietnam) Limited which is mainly regulated by State Bank of Vietnam (SBV). Recipients in Vietnam should contact Standard Chartered Bank (Vietnam) Limited for any queries regarding any content of this document. Zambia: This document is distributed by Standard Chartered Bank Zambia Plc, a company incorporated in Zambia and registered as a commercial bank and licensed by the Bank of Zambia under the Banking and Financial Services Act Chapter 387 of the Laws of Zambia.