This article is for informational purposes only.

Tax Deduction: 8 Items to Save

To reduce your tax in Hong Kong, it is important to understand the available deductions and allowances so you can minimise your chargeable income. This guide summarises 8 commonly used tax deductions and allowances, including eligibility criteria, deduction limits and frequently asked questions, helping you review each item more easily when completing your tax return.

Tax Deduction Method (1): The Three Tax Deductible Products

The Three Tax Deductible Products generally refer to three product types that can provide medical protection and retirement savings while offering tax deductions:

• Voluntary Health Insurance Scheme (VHIS)

• Qualifying Deferred Annuity Policy (QDAP)

• Tax Deductible Voluntary Contributions (TVC)

These products can enhance your protection and support your retirement planning while also allowing you to claim tax deductions, thereby reducing your chargeable income.

Voluntary Health Insurance Scheme (VHIS) Tax Deduction

Premiums paid for qualifying VHIS policies are deductible and can reduce your chargeable income:

• Maximum deduction: HKD8,000 for each insured person for each year of assessment¹.

• The premium must be paid by the taxpayer claiming the deduction.

• You may claim deductions for yourself and specified relatives

VHIS can provide long-term medical protection, and qualifying premiums may be claimed as deductions when filing your tax return.

Qualifying Deferred Annuity Policy (QDAP) Tax Deduction

Premiums paid for QDAP are deductible and are commonly used to support retirement income planning.

• Maximum deduction: HKD60,000 (combined limit for QDAP premiums and TVC) for each year of assessment.

• Each taxpayer can deduct a maximum of HKD60,000 per year of assessment²

• The policy must be a qualifying QDAP plan, and the premium must be paid by the taxpayer claiming the deduction.

Suitable for individuals who wish to receive a stable annuity income after retirement while using tax deductions to reduce their burden during their working years.

Tax Deductible Voluntary Contributions to MPF (TVC) Tax Deduction

TVC are voluntary contributions made to designated TVC accounts under MPF schemes, and may be claimed as deductions:

• Combined with QDAP, the annual limit is HKD60,000²

• Only contributions in designated TVC accounts are eligible for tax deduction

• Suitable for individuals who wish to accumulate retirement savings over the long term

Although TVC contributions have a lock-in period and withdrawal restrictions, you can enjoy the benefits of retirement savings and tax deductions at the same time.

How Much Tax Can the Three Tax-Deductible Products Actually Help You Save?

The potential tax savings can be estimated using a simple formula: “Total deductible amount × marginal tax rate = estimated tax savings”.

For example, if QDAP and TVC total HKD60,000 and qualifying VHIS premiums for family members total HKD24,000, the total deductible amount would be approximately HKD84,000. At a marginal tax rate of 17%, the estimated tax savings would be about HKD14,280 (HKD84,000 × 17%). The actual tax payable depends on your circumstances.

Tax Deduction Method (2): MPF Mandatory Contributions

Mandatory contributions to Mandatory Provident Fund (MPF) schemes are generally deductible. If you have made mandatory contributions to an approved retirement scheme, you may claim them as a deduction, subject to the maximum deduction of HKD18,0003 for each year of assessment.

Mandatory Contributions vs TVC

Many people confuse MPF mandatory contributions with Tax-Deductible Voluntary Contributions (TVC), thinking they share the same limit. In fact, they are separate tax-deductible items. Therefore, even if you have already used up the HKD18,000 limit for MPF mandatory contributions, you can still claim an additional deduction of up to HKD60,000 through TVC, subject to the combined cap with QDAP.

• Maximum deduction: HKD18,000 for mandatory contributions.

• Maximum deduction: HKD60,000 (combined limit for QDAP premiums and TVC).

Tax Deduction Method (3): Home Loan Interest

If you are an owner paying a mortgage for the residential property you occupy, the mortgage interest can be used as home loan interest for tax deduction, with an annual deduction limit of HKD100,0004.

Eligibility and Joint Tenant Allocation

To successfully claim home loan interest deduction, you must meet the following conditions:

• The property must be in Hong Kong and used wholly as your place of residence; if it is used partly, the amount of interest you can deduct will be reduced proportionally.

• You must be one of the borrowers on the loan and have actually paid interest.

If the property is jointly owned, interest expenses and deduction amounts are generally allocated among the co-owners equally, or in proportion to the tenant’s share of ownership in the dwelling (e.g., you own 60% and the other party owns 40%).

Tax Deduction Method (4): Deduction for Domestic Rent

Taxpayers who rent a domestic property and meet the IRD requirements may claim the domestic rent deduction for a qualifying tenancy. The maximum amount of rent deductible for each year of assessment is HKD100,000⁵.

What Constitutes a Qualifying Tenancy?

To successfully claim deduction for domestic rent, the tenancy and actual living arrangements must meet the following conditions.

Requirements for a qualifying tenancy generally include:

• You have signed a formal tenancy agreement (or sub-tenancy agreement) with the landlord.

• The premise is used as your principal place of residence during the relevant year of assessment.

Where a property is shared by multiple tenants:

• If you share the flat with others under the same tenancy, the rent paid will be split equally among all tenants. For example, if three people share a flat and the total annual rent is HKD300,000, the IRD will assume each person has paid HKD100,000 in rent, and each tenant may calculate their own rent deduction based on that amount.

Tax Deduction Method (5): Expenses of Self-Education

If you have taken approved courses related to your current employment or future earning capacity, the tuition fees paid can become a very practical tax-deductible item, with an annual deduction limit of HKD100,0006. These expenses are deductible expenses that will be directly deducted from your income, thereby lowering your chargeable income and helping to reduce your tax bill.

What Courses Qualify as "Qualifying Self-Education"?

The Inland Revenue Department requires that for self-education expenses to be tax-deductible, they must be incurred on studying a “prescribed course of education”, and that course must be reasonably related to your current employment or to an occupation you intend to take up in the future. Examples include a business executive taking a management course, or recognised examination fees paid to obtain professional qualifications such as those for accountants.

Tax Deduction Method (6): Approved Charitable Donations

Many people make charitable donations or have the habit of donating annually, but if they meet the conditions, these donations may be claimed as a deduction to reduce your chargeable income.

The total amount of approved charitable donations that can be used for tax deduction each year must be at least HKD100. If less than HKD100, no tax deduction can be claimed. The deduction is capped at 35% of your assessable income after allowable deductions (as specified by the IRD⁷).

What Donations Qualify as Approved Charitable Donations?

Approved charitable donations that can be used for tax deduction generally must meet the following conditions:

• Must be donated to charitable institutions or trusts of a public character that are recognised under the Inland Revenue Ordinance and enjoy profits tax exemption status.

• Donations are usually paid in monetary form, with donation receipts from the tax-exempt charity or the Government, and should retain the receipts for a period of 6 years after the expiration of the year of assessment in which the payments were made. You are required to produce receipts if your case is selected for review.

• Donations to un-recognised charitable institutions generally do not fall within the tax-deductible scope.

Tax Deduction Method (7): Dependent Parent/Grandparent Allowance

In recent years, more and more members of the sandwich-class have to simultaneously pay mortgages, raise children and care for elderly parents. They can receive certain tax relief through the government’s dependent parent/grandparent allowance.

If your parents or grandparents meet the age requirements and are regularly maintained by you, you can claim the Dependent Parent/Grandparent Allowance to reduce your chargeable income. Since this allowance is a fixed amount and does not need to be reimbursed based on actual expenditure, the application process is relatively easy.

Common Eligibility Conditions

When claiming dependent parent/grandparent allowance, the eligible elderly should8:

• Be your parents and grandparents, and your spouse’s parents and grandparents.

• The elderly person is aged 55 or more, or eligible to claim an allowance under the Government’s Disability Allowance Scheme.

• Resided with you/your spouse, without paying full cost, for a continuous period of not less than 6 months; or have received from you/your spouse not less than HKD12,000 in money towards his / her maintenance.

Amount of Allowable Deduction

The allowable deduction amount for dependent parents/grandparents is graded according to the elderly person’s age and whether they reside with you. According to the GovHK9

• For elderly persons aged 55 to under 60, the basic dependent allowance is HKD25,000

• For those aged 60 or above or eligible for government disability allowance, the basic allowance is HKD50,000.

If the elderly person normally resides with you throughout the year of assessment, you can receive an additional dependent allowance of the same amount, i.e., an additional HKD25,000 for ages 55-59, and an additional HKD50,000 for age 60 or above. Therefore, for a single elderly person meeting both age and co-residence conditions, the maximum total allowance can reach HKD50,000 or HKD100,000.

Tax Deduction Method (8): Deduction for Elderly Residential Care Expenses

This deduction covers qualifying residential care expenses (including residential and nursing fees) paid for eligible elderly persons.

The deduction limit for elderly residential care expenses per eligible elderly person per year of assessment is HKD100,00010 Assuming you are simultaneously paying care home fees for two elderly persons, theoretically you can claim separately for each elderly person.

Residential care fees generally include cost of care provided to a parent or grandparent who lives in a residential care home, like accommodation, food, nursing care and sundry expenses, while medical expenses and private expenses paid by the residential care home on the resident’s behalf and then recovered from any person are usually not within the tax-deductible scope.

Who Are Eligible Elderly Persons for Elderly Residential Care Expenses?

Eligible elderly persons generally refer to parents, grandparents, or maternal grandparents aged 60 or above, or designated elderly relatives who require long-term care due to permanent disability. As long as you or your spouse have actually paid the residential care fees for that elderly person in an eligible residential care home and have retained relevant receipts, you can claim the deduction on your tax return.

Dependent Parent/Grandparent Allowance vs Elderly Residential Care Expenses Deduction

Deduction for elderly residential care expenses and dependent parent/grandparent allowance cannot be claimed simultaneously for the same elderly person, so when filing tax returns, you should first compare which item can help save more tax.

If you have already claimed the dependent allowance for a certain elderly person, you generally cannot claim the elderly residential care expenses deduction for that same elderly person’s care home fees; conversely, if the elderly person is permanently residing in a care home with substantial facility fees, switching to claiming the residential care expenses deduction may sometimes be more advantageous than the dependent allowance.

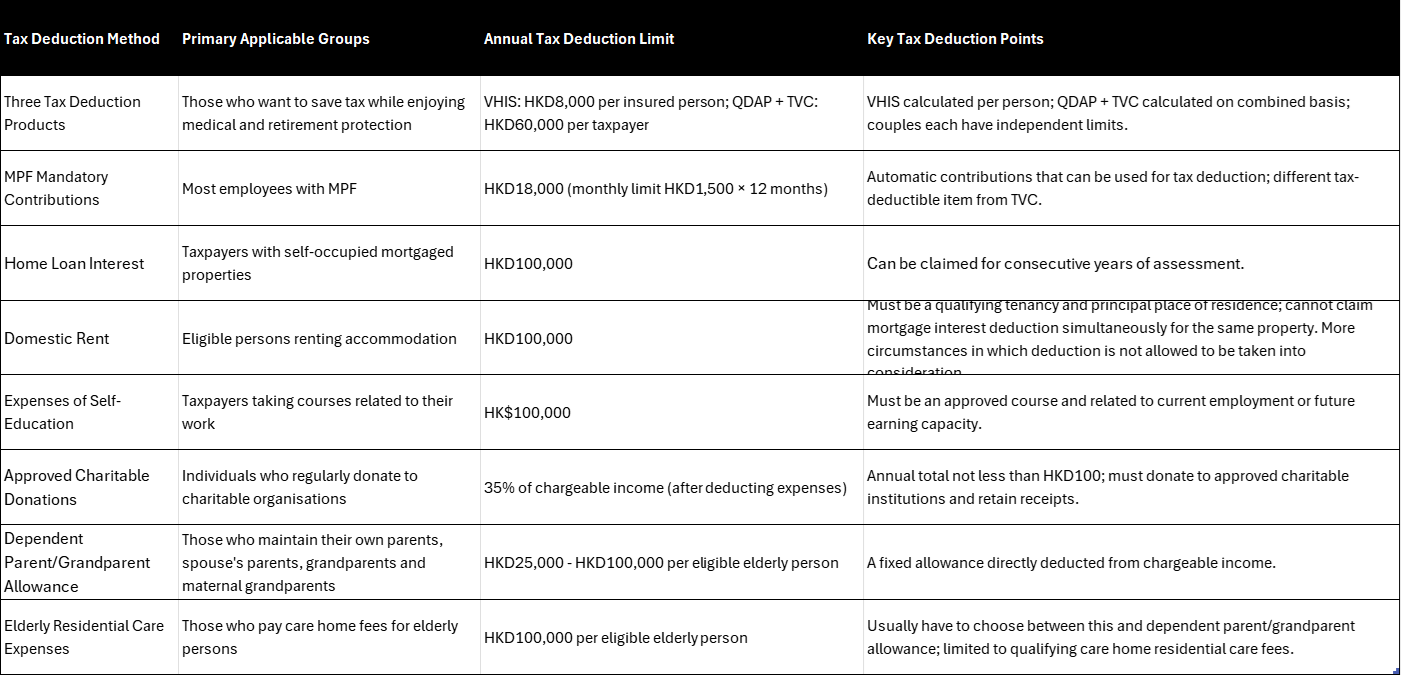

Summary of the 8 Major Tax Deduction Methods

Standard Chartered x Prudential Voluntary Health Insurance Scheme (VHIS) and Deferred Annuity Plans (QDAP)

Standard Chartered offers a series of Voluntary Health Insurance Schemes underwritten by Prudential, covering hospitalisation and surgical protection from standard to high-end premium levels, and also provides Qualifying Deferred Annuity Plans underwritten by Prudential, allowing customers to plan for long-term medical care and retirement while making good use of tax deductible solutions, managing protection needs, asset growth and tax deduction through the same banking platform.

By applying relevant products through Standard Chartered, you can not only select products that are certified under the Voluntary Health Insurance Scheme and Qualifying Deferred Annuity Policy and handle daily financial management, medical protection and retirement planning on the same platform, with more centralised and convenient account and premium payment management. You can also enjoy Standard Chartered’s one-on-one financial and insurance consultation services, easily helping you balance cash flow, protection coverage and long-term retirement income arrangements.

Prudential VHIS products are certified products under the government’s Voluntary Health Insurance Scheme, using standardised policy terms and conditions. Coverage may include hospitalisation and surgical fees, designated diagnostic testing, non-surgical cancer treatment, some psychiatric and rehabilitation treatments, and covers “unknown pre-existing conditions” and some unknown congenital conditions. Standard and flexi plans offer high or even unlimited lifetime benefit limits and provide guaranteed renewal to advanced ages, allowing you to continue protection even after changes in health status.

Prudential QDAP products are Qualifying Deferred Annuity Plans certified by the Insurance Authority, helping you establish predictable cash flow for retirement through stable annuity income and tax benefits. The plans offer multiple premium payment terms and annuity payout period options, with guaranteed monthly annuity, non-guaranteed monthly annuity and non-guaranteed terminal bonus, allowing you to adjust according to your personal risk appetite and retirement timeline, achieving a good balance between savings growth and stable income.

The qualifying premiums for both products can be used for tax deduction when filing tax returns per insured person per year. When combined with applying policies for multiple family members, this can strengthen the overall medical protection network while bringing flexibility to household cash flow in tax .

References:

1. Voluntary Health Insurance Scheme, Tax Deductiom

2. GovHK, Tax Deductions for Qualifying Annuity Premiums and Tax Deductible MPF Voluntary Contributions

4. GovHK, Deduction for Home Loan Interest

5. Inland Revenue Department, Tax Deduction for Domestic Rent

6. GovHK, Deduction for Expenses of Self-Education