2 December 2022

Weekly Market View

Santa Claus rally?

The last quarter of the calendar year is historically one of the strongest quarters for risk assets. This year, global stocks have already rallied around 15% from the start of the quarter on expectations of a peak in Fed rates in H1 2023 and a faster relaxation of mobility restrictions in China.

The S&P500 index now faces major resistance. A break higher is possible if inflation slows. However, we believe fundamentals do not support chasing the rally into 2023. Records show none of the US bear markets in the past 100 years ended before the associated recession has begun.

We expect a recession to start in the US and Euro area by mid-2023. More indicators are flashing warnings. The evolving scenario calls for a defensive allocation. In the following pages, we discuss some of the cyclical and tactical opportunities.

Should we chase the rally in Hong Kong and Mainland China equities?

Is credit risk in Developed Markets likely to escalate given rising recession risks?

What are the tactical opportunities arising from the recent USD slump?

Charts of the week: Challenging technicals and fundamentals

The US equity rally is facing technical resistance, while bond markets are signalling heightened risk of a global recession

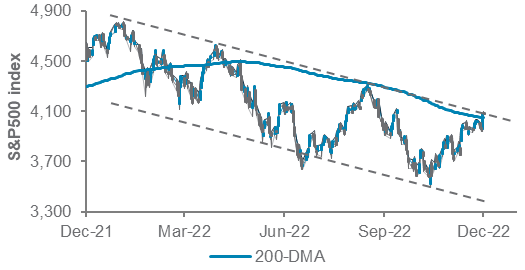

S&P500 index, with 200-day moving average (DMA)

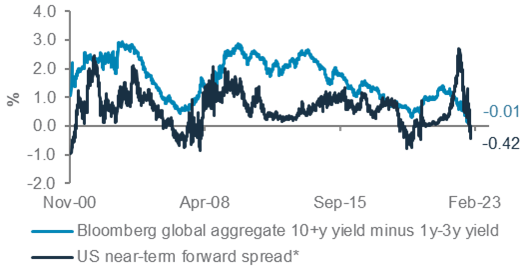

Global and US government bond yield curves

Source: Bloomberg, Standard Chartered; *Fed’s preferred recession indicator: implied yield on 3m T-bills in 18 months minus 3m T-bill yield

Editorial

Santa Claus rally?

The last quarter of the calendar year is historically one of the strongest quarters for risk assets, with global equities delivering an average 3.6% return since the turn of the century. This year, global stocks have already rallied around 15% from the start of the quarter on expectations of a peak in Fed rates in H1 2023 and a faster relaxation of mobility restrictions in China. The rally has helped investors recover some of this year’s losses. The S&P500 index now faces major resistance around 4120 (top of a downtrend channel since January). It could potentially break higher if we see signs of inflation slowing. However, we believe fundamentals do not support chasing the rally into 2023. Records show none of the US bear markets in the past 100 years ended before the associated recession has begun.

We expect a recession to start in the US and Euro area by mid-2023. More indicators are flashing warnings. This week the global bond yield curve inverted for the first time in 20 years. This follows inversions of several US government bond yield curves (see chart). In November, the US ISM Manufacturing index fell into contractionary territory (below 50) for the first time since the depths of the pandemic, and the forward-looking ISM New Orders PMI remained below 50 for the third straight month. Moreover, the Chicago PMI plunged below the critical 40 level which has historically signalled an imminent recession. In Europe, the German government bond yield curve inverted from one year out, a rare occurrence which has historically led to a recession in Europe’s largest economy.

The deterioration in activity data signals pain ahead for US and European corporate earnings and, by extension, equities, since earnings estimates in these markets have not yet factored in a recession, in our opinion. Central banks are unlikely to come to the rescue soon enough. This week, Fed Chair Powell did signal a likely slowdown in the pace of rate hikes from this month but hastened to add that there is still “a long way to go” to restore price stability (US core PCE deflator rose 5% y/y in

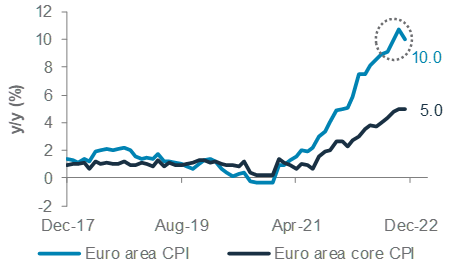

October). He also reiterated that the Fed terminal rate will likely be “somewhat above” the 4.75% projection in September. This implies that the Fed is likely to keep hiking rates into 2023 after possibly delivering a 50bps hike to 4.5% on 14 December. Meanwhile, ECB President Christine Lagarde warned that the central bank must continue to hike even as the economy weakens into 2023 as inflation remains well above its 2% target (Euro area core inflation was 5% y/y in October).

Investment conclusions: The evolving scenario calls for a defensive allocation. This involves, among others:

- Fading any US and European equity rally going into Christmas and rebalancing into Investment Grade bonds and other income assets. Bond yields at multi-decade highs offer attractive income as investors wait out the coming downturn.

- Within equities, rebalance into Asia ex-Japan equities, which are still inexpensive and have the tailwind of China’s sustained policy stimulus and a gradual normalisation of economic activity (see page 4). Major Mainland China cities including Guangzhou this week relaxed mobility restrictions after authorities unveiled a plan to accelerate vaccinations. The USD’s 9% decline since its 20-year peak in September amid lower US government bond yields is also likely to revive flows back into Emerging Markets.

- In the US, rotate into more defensive equity sectors, such as healthcare; the energy sector remains preferred in the US and Europe given the sector’s strong earnings outlook.

- With increased recession risks, we see tactical opportunities in FX: we expect EUR/JPY and GBP/USD to weaken (page 5).

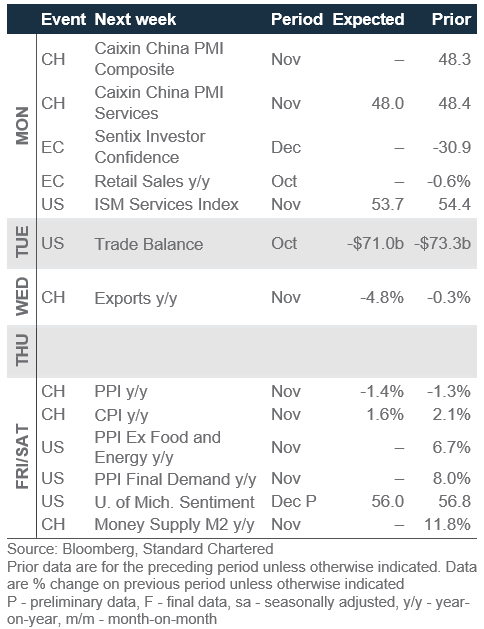

What we are watching: US payrolls (consensus: 200,000 jobs); OPEC+ meeting on Sunday to decide whether to cut output; EU agreement on the price cap on Russian oil exports before embargo starts 5 Dec; US Services PMI (consensus: 53.5); Euro area retail sales; and China exports (-4.8% y/y).

— Rajat Bhattacharya

The weekly macro balance sheet

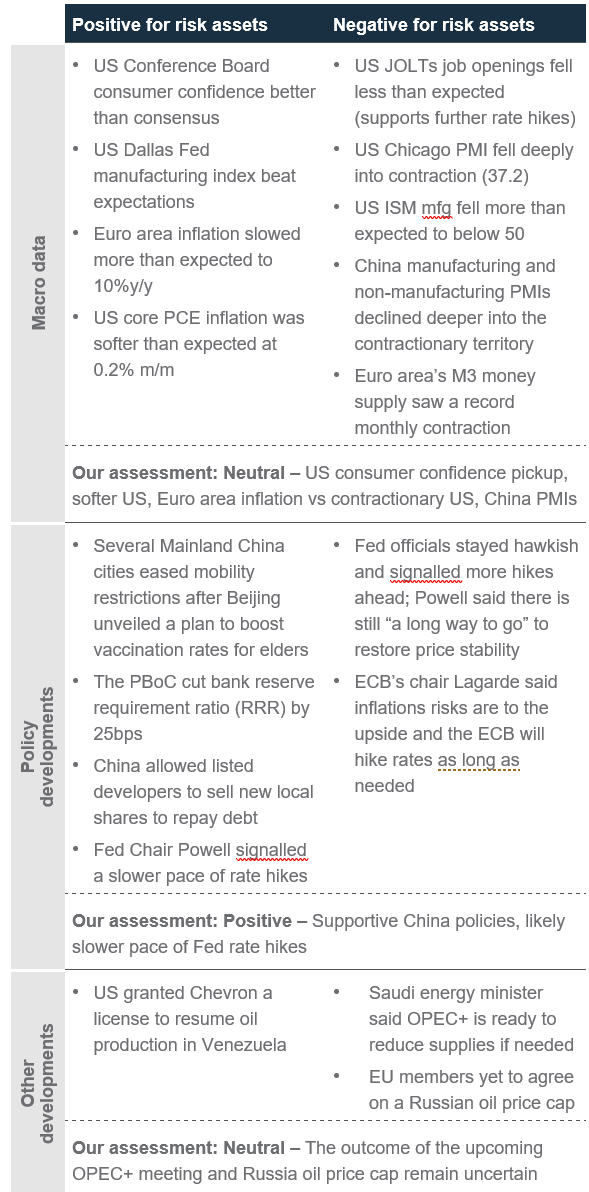

Our weekly net assessment: On balance, we see the past week’s data and policy as neutral for risk assets in the near term.

(+) factor: China reopening, slower US rate hike signal, softer inflation

(-) factor: Contractionary China, US PMIs, strong US job openings

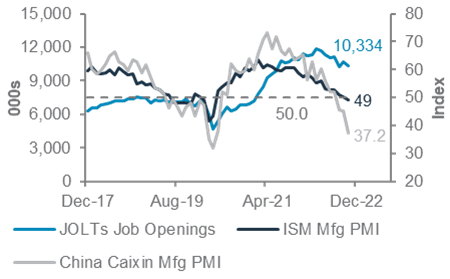

The Fed is likely to keep hiking until US job openings decline significantly, even if activity indicators point to increased risk of a recession

US job openings (JOLTS), ISM Manufacturing and Chicago PMI

Euro area consumer inflation appears to have peaked, although still-elevated core inflation means the ECB is likely to continue hiking rates

Euro area headline and core consumer inflation

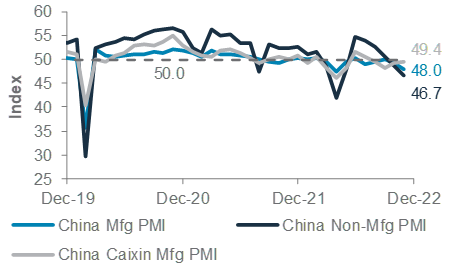

We expect China’s economy to recover in 2023 as easing mobility restrictions and easier credit policies revive consumption and business activity

China’s manufacturing and non-manufacturing PMIs

Top client questions

Should we chase the rally in Hong Kong and Mainland China equities?

After dipping briefly at the start of the week, Chinese equities saw strong buying interest in recent days, as seen by the volume in the Hang Seng index this week being 2.5x the average daily volume in H2 22. The easing of mobility restrictions in key Mainland China cities such as Guangzhou and the central government’s plans to boost the vaccination rate among elders have fuelled expectations of further relaxations. These moves, coupled with the “third arrow” to support the property sector, allowing Chinese developers to raise equity to repay debt and fund acquisitions, propelled the Hang Seng index to break key technical resistance levels of 18,400 and 19,200.

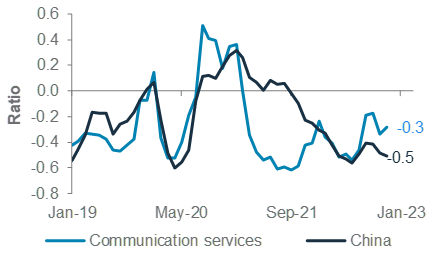

We believe further economic reopening would favour sectors that benefit from a rebound in consumption. The Communications Services sector, in our opinion, offers attractive risk-reward in this regard. The sector’s earnings have beaten expectations, and positioning in the sector remains relatively less crowded, based on our measures of investor diversity.

We would consider averaging into Chinese equities on pullbacks. Key support levels for the Hang Seng Index are at 17,400 and 18,100, representing the 61% and 76% Fibonacci retracement levels for the trading range since the end of October (14,600 to 19,200), while 3,767 is a key level of support for the CSI 300 index.

— Daniel Lam, CFA, Head, Equity Strategy

The Communications Services sector in China may benefit from easing mobility restrictions

Earnings revisions* for MSCI China Communication Services and MSCI China indices

Earnings revision = 3 months moving average of (number of earnings upgrades / number of earnings downgrades – 1)

Is credit risk in Developed Markets likely to escalate given the elevated recession risk in the US?

With the Fed policy arguably already at restrictive levels, we believe the recession risk has surged amid tight financial conditions. We observe the corporate bond market is also starting to price recession risk, as illustrated by some portions of the global bond yield curve turning negative (inverting), with investors likely starting to add more longer maturity bonds to lock in long-term yields.

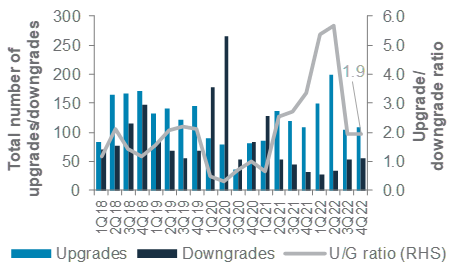

Against this recessionary outlook, corporate credit quality is likely to deteriorate as corporate earnings growth slows and interest burden piles up, resulting in a widening of corporate bond yield premiums (spreads over government bonds). However, we expect this impact to vary considerably across different types of corporate bonds. For Developed Markets (US/Europe) Investment Grade (IG) corporate bonds, we expect the impact to be contained for two reasons. First, credit rating upgrades of IG bonds continue to outpace downgrades, which, in our view, reflects their relatively strong balance sheets and resilient business profiles to weather a recession. In addition, most issuers have pre-funded and strengthened their capitalisation in previous years of low interest rate environment. Hence, despite the possible risks from a recession, we retain our preference for DM IG corporate bonds.

— Cedric Lam, Senior Investment Strategist

Credit rating upgrades in DM IG bonds continue to outpace downgrades, albeit at a slower pace

Credit ratings 1Q 2018 to QTD 4Q 2022

Top client questions (cont’d)

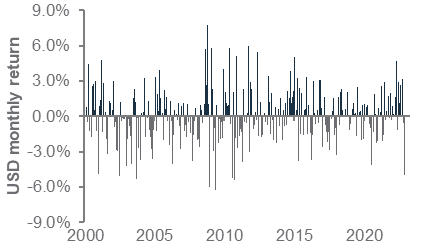

What are the tactical opportunities arising from the recent USD slump?

Fed Chair Powell’s comments this week, where he guided markets towards a slower pace of rate hikes than before amid signs of softness in the job market and elevated recession risks, pushed US government bond yields and the USD index (DXY) lower. As a result, November was the worst month for the USD since 2010. Given this rapid adjustment over the past month, we see a high likelihood of a period of consolidation for the USD, with the 200-dma at 105.50 and Fibonacci retracement at 104.70 acting as key supports.

On a tactical (2-4 week) basis, we see two opportunities in FX markets:

- With most major G10 central banks (with the notable exception of RBNZ) softening their rate hike stance modestly, we see scope for the JPY to extend recent gains as markets start to price in a narrowing of interest rate differentials. In particular, we expect EUR/JPY to head down towards the 141.00-141.50 range.

- GBP/USD is starting to look stretched after the nearly 17% bounce from the September 2022 lows. With the UK’s challenging growth outlook, we see elevated risk of an incrementally more dovish BoE as well. This means GBP/USD could decline to retest the 1.1700-1.1790 support in the next few weeks

— Abhilash Narayan, Senior Investment Strategist

The USD delivered in November the worst monthly return since 2010

Monthly return for the USD (DXY) index

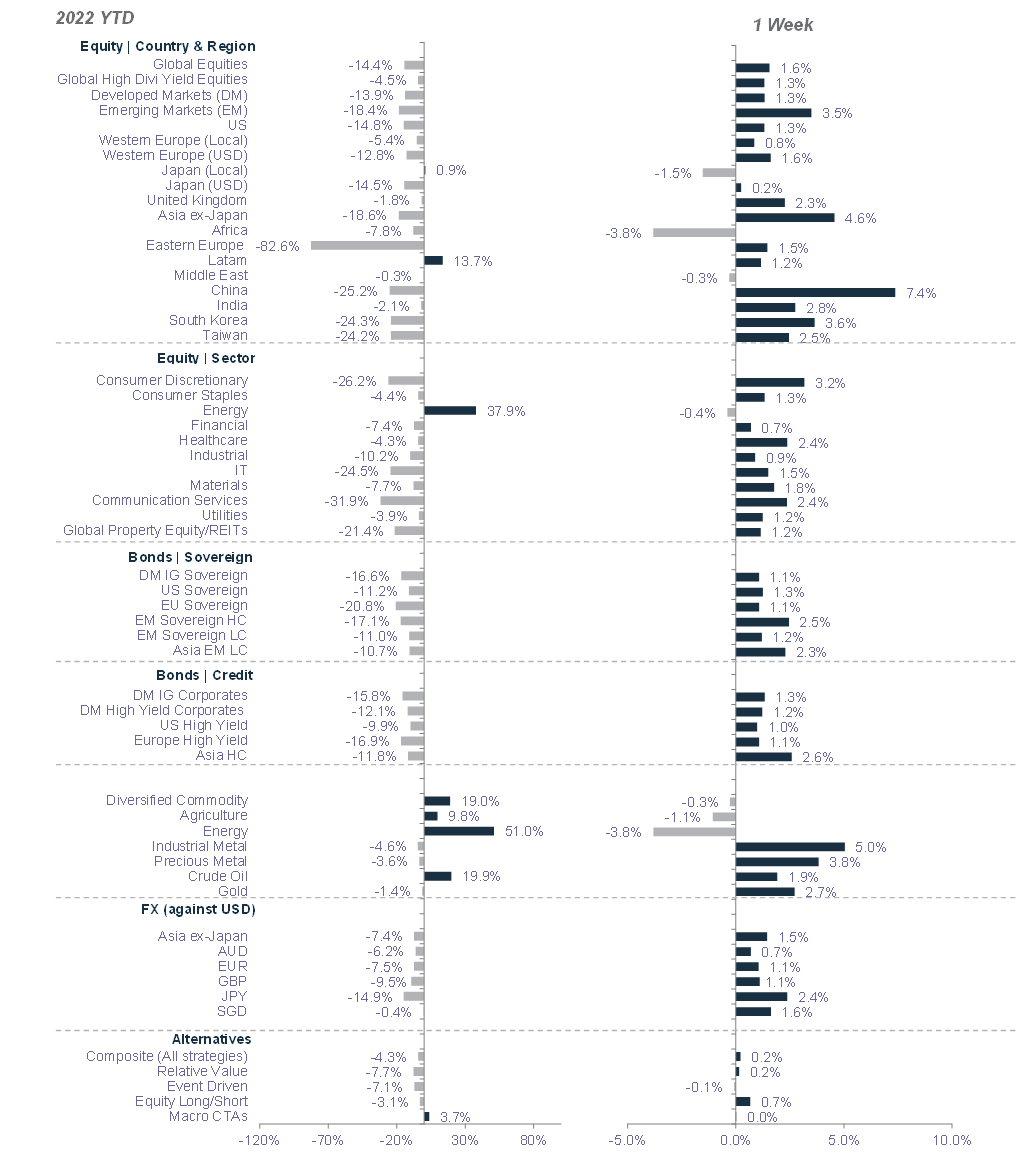

Market performance summary*

*Performance in USD terms unless otherwise stated, 2022 YTD performance from 31 December 2021 to 01 December 2022; 1-week period: 24 November 2022 to 1 December 2022

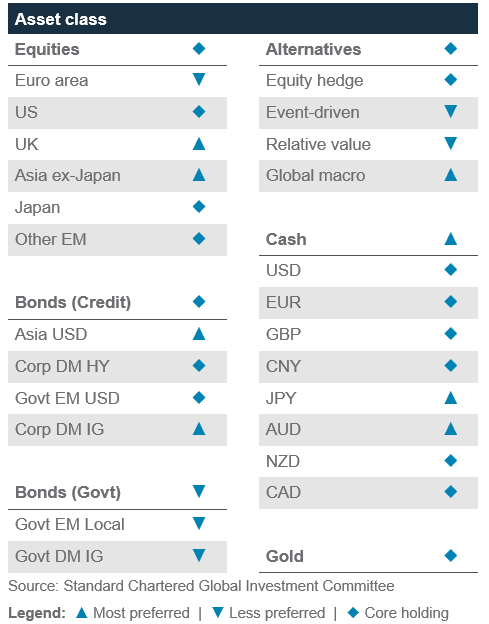

Our 12-month asset class views at a glance

Economic and market calendar

The S&P500 index faces resistance around 4,119

Technical indicators for key markets as of 01 December close

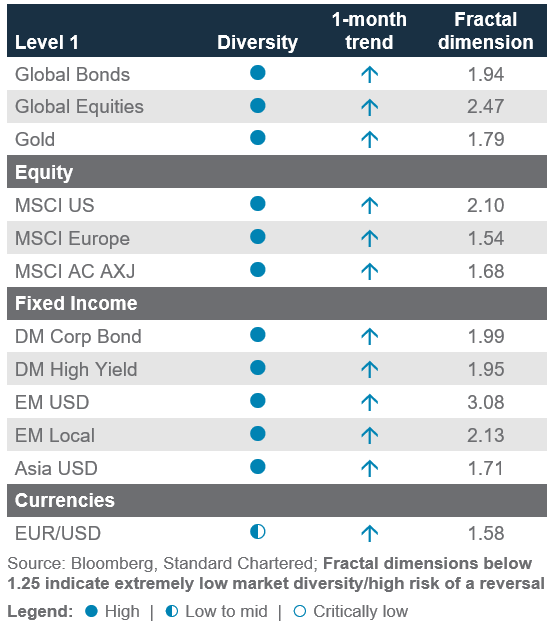

Investor diversity has improved for gold in the past month

Our proprietary market diversity indicators as of 01 December

Disclosure

This document is confidential and may also be privileged. If you are not the intended recipient, please destroy all copies and notify the sender immediately. This document is being distributed for general information only and is subject to the relevant disclaimers available at our Standard Chartered website under Regulatory disclosures. It is not and does not constitute research material, independent research, an offer, recommendation or solicitation to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments. This document is for general evaluation only. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person or class of persons and it has not been prepared for any particular person or class of persons. You should not rely on any contents of this document in making any investment decisions. Before making any investment, you should carefully read the relevant offering documents and seek independent legal, tax and regulatory advice. In particular, we recommend you to seek advice regarding the suitability of the investment product, taking into account your specific investment objectives, financial situation or particular needs, before you make a commitment to purchase the investment product. Opinions, projections and estimates are solely those of SC at the date of this document and subject to change without notice. Past performance is not indicative of future results and no representation or warranty is made regarding future performance. The value of investments, and the income from them, can go down as well as up, and you may not recover the amount of your original investment. You are not certain to make a profit and may lose money. Any forecast contained herein as to likely future movements in rates or prices or likely future events or occurrences constitutes an opinion only and is not indicative of actual future movements in rates or prices or actual future events or occurrences (as the case may be). This document must not be forwarded or otherwise made available to any other person without the express written consent of the Standard Chartered Group (as defined below). Standard Chartered Bank is incorporated in England with limited liability by Royal Charter 1853 Reference Number ZC18. The Principal Office of the Company is situated in England at 1 Basinghall Avenue, London, EC2V 5DD. Standard Chartered Bank is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and Prudential Regulation Authority. Standard Chartered PLC, the ultimate parent company of Standard Chartered Bank, together with its subsidiaries and affiliates (including each branch or representative office), form the Standard Chartered Group. Standard Chartered Private Bank is the private banking division of Standard Chartered. Private banking activities may be carried out internationally by different legal entities and affiliates within the Standard Chartered Group (each an “SC Group Entity”) according to local regulatory requirements. Not all products and services are provided by all branches, subsidiaries and affiliates within the Standard Chartered Group. Some of the SC Group Entities only act as representatives of Standard Chartered Private Bank and may not be able to offer products and services or offer advice to clients.

Copyright © 2024, Accounting Research & Analytics, LLC d/b/a CFRA (and its affiliates, as applicable). Reproduction of content provided by CFRA in any form is prohibited except with the prior written permission of CFRA. CFRA content is not investment advice and a reference to or observation concerning a security or investment provided in the CFRA SERVICES is not a recommendation to buy, sell or hold such investment or security or make any other investment decisions. The CFRA content contains opinions of CFRA based upon publicly-available information that CFRA believes to be reliable and the opinions are subject to change without notice. This analysis has not been submitted to, nor received approval from, the United States Securities and Exchange Commission or any other regulatory body. While CFRA exercised due care in compiling this analysis, CFRA, ITS THIRD-PARTY SUPPLIERS, AND ALL RELATED ENTITIES SPECIFICALLY DISCLAIM ALL WARRANTIES, EXPRESS OR IMPLIED, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE, to the full extent permitted by law, regarding the accuracy, completeness, or usefulness of this information and assumes no liability with respect to the consequences of relying on this information for investment or other purposes. No content provided by CFRA (including ratings, credit-related analyses and data, valuations, model, software or other application or output therefrom) or any part thereof may be modified, reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval system, without the prior written permission of CFRA, and such content shall not be used for any unlawful or unauthorized purposes. CFRA and any third-party providers, as well as their directors, officers, shareholders, employees or agents do not guarantee the accuracy, completeness, timeliness or availability of such content. In no event shall CFRA, its affiliates, or their third-party suppliers be liable for any direct, indirect, special, or consequential damages, costs, expenses, legal fees, or losses (including lost income or lost profit and opportunity costs) in connection with a subscriber’s, subscriber’s customer’s, or other’s use of CFRA’s content.

Market Abuse Regulation (MAR) Disclaimer

Banking activities may be carried out internationally by different branches, subsidiaries and affiliates within the Standard Chartered Group according to local regulatory requirements. Opinions may contain outright “buy”, “sell”, “hold” or other opinions. The time horizon of this opinion is dependent on prevailing market conditions and there is no planned frequency for updates to the opinion. This opinion is not independent of Standard Chartered Group’s trading strategies or positions. Standard Chartered Group and/or its affiliates or its respective officers, directors, employee benefit programmes or employees, including persons involved in the preparation or issuance of this document may at any time, to the extent permitted by applicable law and/or regulation, be long or short any securities or financial instruments referred to in this document or have material interest in any such securities or related investments. Therefore, it is possible, and you should assume, that Standard Chartered Group has a material interest in one or more of the financial instruments mentioned herein. Please refer to our Standard Chartered website under Regulatory disclosures for more detailed disclosures, including past opinions/ recommendations in the last 12 months and conflict of interests, as well as disclaimers. A covering strategist may have a financial interest in the debt or equity securities of this company/issuer. This document must not be forwarded or otherwise made available to any other person without the express written consent of Standard Chartered Group.

Sustainable Investments

Any ESG data used or referred to has been provided by Morningstar, Sustainalytics, MSCI or Bloomberg. Refer to 1) Morningstar website under Sustainable Investing, 2) Sustainalytics website under ESG Risk Ratings, 3) MCSI website under ESG Business Involvement Screening Research for more information. The ESG data is as at the date of publication based on data provided, is for informational purpose only and is not warranted to be complete, timely, accurate or suitable for a particular purpose, and it may be subject to change. Sustainable Investments (SI): This refers to funds that have been classified as ‘Sustainable Investments’ by Morningstar. SI funds have explicitly stated in their prospectus and regulatory filings that they either incorporate ESG factors into the investment process or have a thematic focus on the environment, gender diversity, low carbon, renewable energy, water or community development. For equity, it refers to shares/stocks issued by companies with Sustainalytics ESG Risk Rating of Low/Negligible. For bonds, it refers to debt instruments issued by issuers with Sustainalytics ESG Risk Rating of Low/Negligible, and/or those being certified green, social, sustainable bonds. For structured products, it refers to products that are issued by any issuer who has a Sustainable Finance framework that aligns with Standard Chartered’s Green and Sustainable Product Framework, with underlying assets that are part of the Sustainable Investment universe or separately approved by Standard Chartered’s Sustainable Finance Governance Committee.

Country/Market Specific Disclosures

Botswana: This document is being distributed in Botswana by, and is attributable to, Standard Chartered Bank Botswana Limited which is a financial institution licensed under the Section 6 of the Banking Act CAP 46.04 and is listed in the Botswana Stock Exchange. Brunei Darussalam: This document is being distributed in Brunei Darussalam by, and is attributable to, Standard Chartered Bank (Brunei Branch) | Registration Number RFC/61 and Standard Chartered Securities (B) Sdn Bhd | Registration Number RC20001003. Standard Chartered Bank is incorporated in England with limited liability by Royal Charter 1853 Reference Number ZC18. Standard Chartered Securities (B) Sdn Bhd is a limited liability company registered with the Registry of Companies with Registration Number RC20001003 and licensed by Brunei Darussalam Central Bank as a Capital Markets Service License Holder with License Number BDCB/R/CMU/S3-CL and it is authorised to conduct Islamic investment business through an Islamic window. China Mainland: This document is being distributed in China by, and is attributable to, Standard Chartered Bank (China) Limited which is mainly regulated by National Financial Regulatory Administration (NFRA), State Administration of Foreign Exchange (SAFE), and People’s Bank of China (PBOC). Hong Kong: In Hong Kong, this document, except for any portion advising on or facilitating any decision on futures contracts trading, is distributed by Standard Chartered Bank (Hong Kong) Limited (“SCBHK”), a subsidiary of Standard Chartered PLC. SCBHK has its registered address at 32/F, Standard Chartered Bank Building, 4-4A Des Voeux Road Central, Hong Kong and is regulated by the Hong Kong Monetary Authority and registered with the Securities and Futures Commission (“SFC”) to carry on Type 1 (dealing in securities), Type 4 (advising on securities), Type 6 (advising on corporate finance) and Type 9 (asset management) regulated activity under the Securities and Futures Ordinance (Cap. 571) (“SFO”) (CE No. AJI614). The contents of this document have not been reviewed by any regulatory authority in Hong Kong and you are advised to exercise caution in relation to any offer set out herein. If you are in doubt about any of the contents of this document, you should obtain independent professional advice. Any product named herein may not be offered or sold in Hong Kong by means of any document at any time other than to “professional investors” as defined in the SFO and any rules made under that ordinance. In addition, this document may not be issued or possessed for the purposes of issue, whether in Hong Kong or elsewhere, and any interests may not be disposed of, to any person unless such person is outside Hong Kong or is a “professional investor” as defined in the SFO and any rules made under that ordinance, or as otherwise may be permitted by that ordinance. In Hong Kong, Standard Chartered Private Bank is the private banking division of SCBHK, a subsidiary of Standard Chartered PLC. Ghana: Standard Chartered Bank Ghana Limited accepts no liability and will not be liable for any loss or damage arising directly or indirectly (including special, incidental or consequential loss or damage) from your use of these documents. Past performance is not indicative of future results and no representation or warranty is made regarding future performance. You should seek advice from a financial adviser on the suitability of an investment for you, taking into account these factors before making a commitment to invest in an investment. To unsubscribe from receiving further updates, please send an email to feedback.ghana@sc.com. Please do not reply to this email. Call our Priority Banking on 0302610750 for any questions or service queries. You are advised not to send any confidential and/or important information to Standard Chartered via e-mail, as Standard Chartered makes no representations or warranties as to the security or accuracy of any information transmitted via e-mail. Standard Chartered shall not be responsible for any loss or damage suffered by you arising from your decision to use e-mail to communicate with the Bank. India: This document is being distributed in India by Standard Chartered in its capacity as a distributor of mutual funds and referrer of any other third party financial products. Standard Chartered does not offer any ‘Investment Advice’ as defined in the Securities and Exchange Board of India (Investment Advisers) Regulations, 2013 or otherwise. Services/products related securities business offered by Standard Charted are not intended for any person, who is a resident of any jurisdiction, the laws of which imposes prohibition on soliciting the securities business in that jurisdiction without going through the registration requirements and/or prohibit the use of any information contained in this document. Indonesia: This document is being distributed in Indonesia by Standard Chartered Bank, Indonesia branch, which is a financial institution licensed, registered and supervised by Otoritas Jasa Keuangan (Financial Service Authority). Jersey: In Jersey, Standard Chartered Private Bank is the Registered Business Name of the Jersey Branch of Standard Chartered Bank. The Jersey Branch of Standard Chartered Bank is regulated by the Jersey Financial Services Commission. Copies of the latest audited accounts of Standard Chartered Bank are available from its principal place of business in Jersey: PO Box 80, 15 Castle Street, St Helier, Jersey JE4 8PT. Standard Chartered Bank is incorporated in England with limited liability by Royal Charter in 1853 Reference Number ZC 18. The Principal Office of the Company is situated in England at 1 Basinghall Avenue, London, EC2V 5DD. Standard Chartered Bank is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and Prudential Regulation Authority. The Jersey Branch of Standard Chartered Bank is also an authorised financial services provider under license number 44946 issued by the Financial Sector Conduct Authority of the Republic of South Africa. Jersey is not part of the United Kingdom and all business transacted with Standard Chartered Bank, Jersey Branch and other SC Group Entity outside of the United Kingdom, are not subject to some or any of the investor protection and compensation schemes available under United Kingdom law. Kenya: This document is being distributed in Kenya by, and is attributable to Standard Chartered Bank Kenya Limited. Investment Products and Services are distributed by Standard Chartered Investment Services Limited, a wholly owned subsidiary of Standard Chartered Bank Kenya Limited that is licensed by the Capital Markets Authority as a Fund Manager. Standard Chartered Bank Kenya Limited is regulated by the Central Bank of Kenya. Malaysia: This document is being distributed in Malaysia by Standard Chartered Bank Malaysia Berhad. Recipients in Malaysia should contact Standard Chartered Bank Malaysia Berhad in relation to any matters arising from, or in connection with, this document. Nigeria: This document is being distributed in Nigeria by Standard Chartered Bank Nigeria Limited, a bank duly licensed and regulated by the Central Bank of Nigeria. Standard Chartered accepts no liability for any loss or damage arising directly or indirectly (including special, incidental or consequential loss or damage) from your use of these documents. You should seek advice from a financial adviser on the suitability of an investment for you, taking into account these factors before making a commitment to invest in an investment. To unsubscribe from receiving further updates, please send an email to clientcare.ng@sc.com requesting to be removed from our mailing list. Please do not reply to this email. Call our Priority Banking on 01-2772514 for any questions or service queries. Standard Chartered shall not be responsible for any loss or damage arising from your decision to send confidential and/or important information to Standard Chartered via e-mail, as Standard Chartered makes no representations or warranties as to the security or accuracy of any information transmitted via e-mail. Pakistan: This document is being distributed in Pakistan by, and attributable to Standard Chartered Bank (Pakistan) Limited having its registered office at PO Box 5556, I.I Chundrigar Road Karachi, which is a banking company registered with State Bank of Pakistan under Banking Companies Ordinance 1962 and is also having licensed issued by Securities & Exchange Commission of Pakistan for Security Advisors. Standard Chartered Bank (Pakistan) Limited acts as a distributor of mutual funds and referrer of other third-party financial products. Singapore: This document is being distributed in Singapore by, and is attributable to, Standard Chartered Bank (Singapore) Limited (Registration No. 201224747C/ GST Group Registration No. MR-8500053-0, “SCBSL”). Recipients in Singapore should contact SCBSL in relation to any matters arising from, or in connection with, this document. SCBSL is an indirect wholly owned subsidiary of Standard Chartered Bank and is licensed to conduct banking business in Singapore under the Singapore Banking Act, 1970. Standard Chartered Private Bank is the private banking division of SCBSL. IN RELATION TO ANY SECURITY OR SECURITIES-BASED DERIVATIVES CONTRACT REFERRED TO IN THIS DOCUMENT, THIS DOCUMENT, TOGETHER WITH THE ISSUER DOCUMENTATION, SHALL BE DEEMED AN INFORMATION MEMORANDUM (AS DEFINED IN SECTION 275 OF THE SECURITIES AND FUTURES ACT, 2001 (“SFA”)). THIS DOCUMENT IS INTENDED FOR DISTRIBUTION TO ACCREDITED INVESTORS, AS DEFINED IN SECTION 4A(1)(a) OF THE SFA, OR ON THE BASIS THAT THE SECURITY OR SECURITIES-BASED DERIVATIVES CONTRACT MAY ONLY BE ACQUIRED AT A CONSIDERATION OF NOT LESS THAN S$200,000 (OR ITS EQUIVALENT IN A FOREIGN CURRENCY) FOR EACH TRANSACTION. Further, in relation to any security or securities-based derivatives contract, neither this document nor the Issuer Documentation has been registered as a prospectus with the Monetary Authority of Singapore under the SFA. Accordingly, this document and any other document or material in connection with the offer or sale, or invitation for subscription or purchase, of the product may not be circulated or distributed, nor may the product be offered or sold, or be made the subject of an invitation for subscription or purchase, whether directly or indirectly, to persons other than a relevant person pursuant to section 275(1) of the SFA, or any person pursuant to section 275(1A) of the SFA, and in accordance with the conditions specified in section 275 of the SFA, or pursuant to, and in accordance with the conditions of, any other applicable provision of the SFA. In relation to any collective investment schemes referred to in this document, this document is for general information purposes only and is not an offering document or prospectus (as defined in the SFA). This document is not, nor is it intended to be (i) an offer or solicitation of an offer to buy or sell any capital markets product; or (ii) an advertisement of an offer or intended offer of any capital markets product. Deposit Insurance Scheme: Singapore dollar deposits of non-bank depositors are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured. This advertisement has not been reviewed by the Monetary Authority of Singapore. Taiwan: SC Group Entity or Standard Chartered Bank (Taiwan) Limited (“SCB (Taiwan)”) may be involved in the financial instruments contained herein or other related financial instruments. The author of this document may have discussed the information contained herein with other employees or agents of SC or SCB (Taiwan). The author and the above-mentioned employees of SC or SCB (Taiwan) may have taken related actions in respect of the information involved (including communication with customers of SC or SCB (Taiwan) as to the information contained herein). The opinions contained in this document may change, or differ from the opinions of employees of SC or SCB (Taiwan). SC and SCB (Taiwan) will not provide any notice of any changes to or differences between the above-mentioned opinions. This document may cover companies with which SC or SCB (Taiwan) seeks to do business at times and issuers of financial instruments. Therefore, investors should understand that the information contained herein may serve as specific purposes as a result of conflict of interests of SC or SCB (Taiwan). SC, SCB (Taiwan), the employees (including those who have discussions with the author) or customers of SC or SCB (Taiwan) may have an interest in the products, related financial instruments or related derivative financial products contained herein; invest in those products at various prices and on different market conditions; have different or conflicting interests in those products. The potential impacts include market makers’ related activities, such as dealing, investment, acting as agents, or performing financial or consulting services in relation to any of the products referred to in this document. UAE: DIFC – Standard Chartered Bank is incorporated in England with limited liability by Royal Charter 1853 Reference Number ZC18.The Principal Office of the Company is situated in England at 1 Basinghall Avenue, London, EC2V 5DD. Standard Chartered Bank is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and Prudential Regulation Authority. Standard Chartered Bank, Dubai International Financial Centre having its offices at Dubai International Financial Centre, Building 1, Gate Precinct, P.O. Box 999, Dubai, UAE is a branch of Standard Chartered Bank and is regulated by the Dubai Financial Services Authority (“DFSA”). This document is intended for use only by Professional Clients and is not directed at Retail Clients as defined by the DFSA Rulebook. In the DIFC we are authorised to provide financial services only to clients who qualify as Professional Clients and Market Counterparties and not to Retail Clients. As a Professional Client you will not be given the higher retail client protection and compensation rights and if you use your right to be classified as a Retail Client we will be unable to provide financial services and products to you as we do not hold the required license to undertake such activities. For Islamic transactions, we are acting under the supervision of our Shariah Supervisory Committee. Relevant information on our Shariah Supervisory Committee is currently available on the Standard Chartered Bank website in the Islamic banking section For residents of the UAE – Standard Chartered Bank UAE does not provide financial analysis or consultation services in or into the UAE within the meaning of UAE Securities and Commodities Authority Decision No. 48/r of 2008 concerning financial consultation and financial analysis. Uganda: Our Investment products and services are distributed by Standard Chartered Bank Uganda Limited, which is licensed by the Capital Markets Authority as an investment adviser. United Kingdom: In the UK, Standard Chartered Bank is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and Prudential Regulation Authority. This communication has been approved by Standard Chartered Bank for the purposes of Section 21 (2) (b) of the United Kingdom’s Financial Services and Markets Act 2000 (“FSMA”) as amended in 2010 and 2012 only. Standard Chartered Bank (trading as Standard Chartered Private Bank) is an authorised financial services provider (license number 45747) in terms of the South African Financial Advisory and Intermediary Services Act, 2002. The Materials have not been prepared in accordance with UK legal requirements designed to promote the independence of investment research, and that it is not subject to any prohibition on dealing ahead of the dissemination of investment research. Vietnam: This document is being distributed in Vietnam by, and is attributable to, Standard Chartered Bank (Vietnam) Limited which is mainly regulated by State Bank of Vietnam (SBV). Recipients in Vietnam should contact Standard Chartered Bank (Vietnam) Limited for any queries regarding any content of this document. Zambia: This document is distributed by Standard Chartered Bank Zambia Plc, a company incorporated in Zambia and registered as a commercial bank and licensed by the Bank of Zambia under the Banking and Financial Services Act Chapter 387 of the Laws of Zambia.