A step-by-step guide to deciphering a Unit Trust factsheet

July 3, 2024

The information in a Unit Trust (UT) fund’s factsheet can be a powerful tool to help you assess the viability of investing in it.

Unit trusts are an attractive asset class for individual investors. They give retail investors exposure to a wide range of underlying assets with initial investment as little as S$1,000 while offering them the opportunity to spread out their investment risk.

Before investing in a UT, you should first study its factsheet. The factsheet reflects the personality of the UT – its objective, performance, risk profile and costs. The qualitative and quantitative data in factsheets can sometimes be overwhelming, so here are some key terms to look out for.

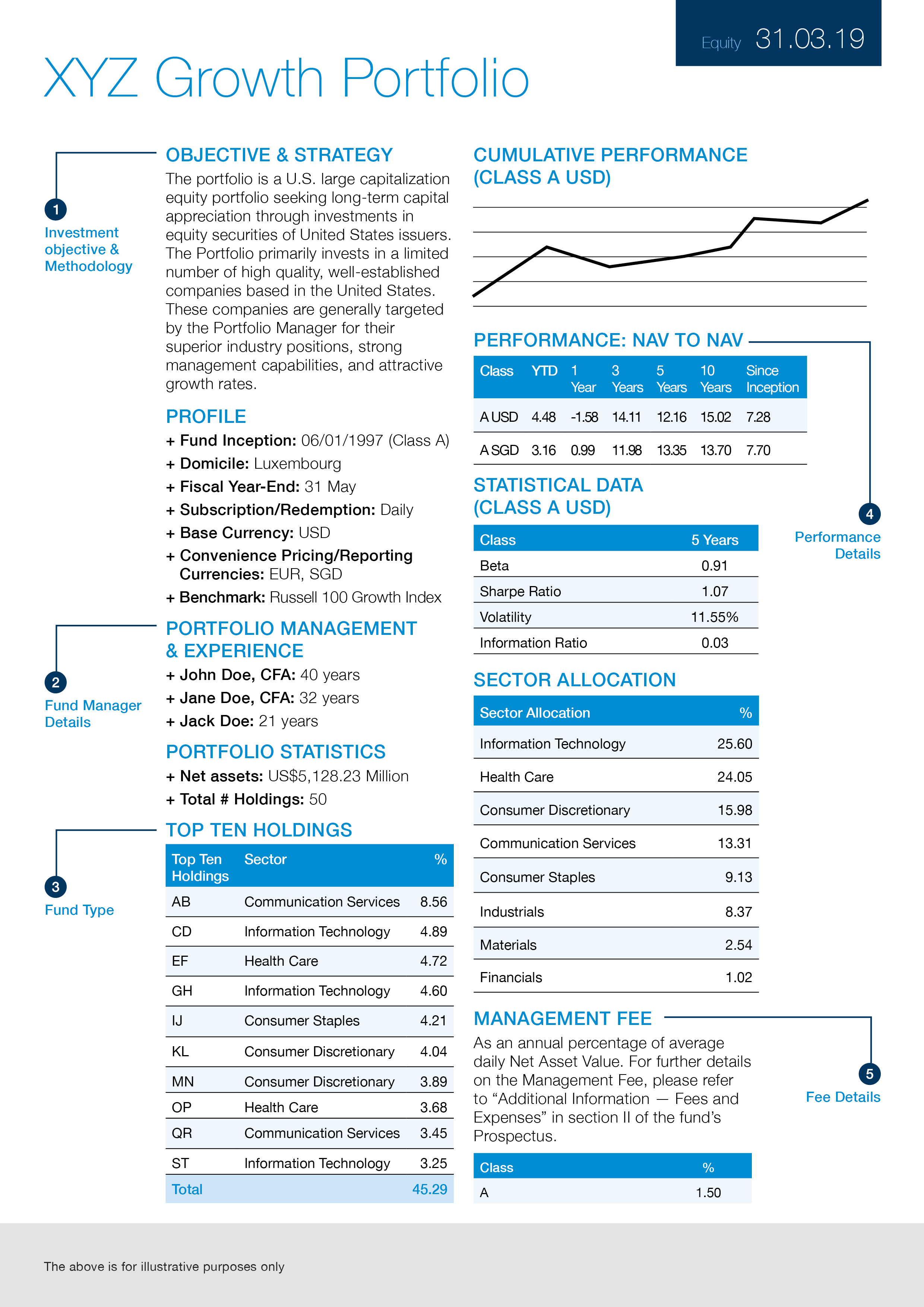

1. Investment objective and methodology

Get a better understanding of the UT’s characteristics, what it strives to achieve and the investment strategy it plans to adopt to meet its goals. Make sure the fund’s investment objective and methodology align with your risk appetite and desired return to avoid investing in a product that does not suit you.

2. Fund manager details

When you invest in a UT, you are essentially handing over your money to fund managers. Therefore, be sure to gather information about the credibility of the people who will be managing your hard-earned money, by studying the performance of past investments that the fund manager has run.

3. Fund type

Funds differ in the way they are invested into and the way they generate income.

Asset allocation: Certain UT invest exclusively in equity or only in debt while others may adopt a more balanced approach by having a mix of both equity and debt. Along with this information, the UT factsheet will also highlight the industry-wise breakdown of where your money is being invested and the fund’s top 10 holdings.

Income feature: The factsheet can also tell you whether the UT has an accumulation feature where the dividend/interest generated is reinvested, or a payout feature where this income is distributed to the investor.

4. Performance details

While past performance of a UT is no guarantee of its future performance, it is still useful to compare a fund’s performance with its peers’. Returns are typically shown over one-year, three-year, five-year and 10-year terms.

You can also look out for statistics such as Sharpe ratio and standard deviation. Sharpe ratio depicts risk-adjusted returns — the higher the ratio, the better. Standard deviation reflects the volatility of the fund over time — the lower the number, the better.

5. Fee details

When you purchase a UT, you accrue an annual fee that covers management charges, administrative charges and operating costs. This is commonly referred to as the Total Expense Ratio (TER). Funds with higher assets under management (AUM) tend to have a lower TER.

Other than the TER, you might also be subject to fees such as entry load when you purchase a UT and exit load when you sell it. These costs can eat into your investment returns so be fully aware of them.

Any retail investor who’s interested in UT as an investment avenue should familiarise themselves with the factsheets so as to make better informed investment decisions.

Disclaimer

This article is for general information only and it does not constitute an offer, recommendation or solicitation to enter into any transaction. This article has not been prepared for any particular person or class of persons and it has been prepared without regard to the specific investment or insurance objectives, financial situation or particular needs of any person. You should seek advice from a licensed or an exempt financial adviser on the suitability of a product for you, taking into account these factors before making a commitment to purchase any product. In the event that you choose not to seek advice from a licensed or an exempt financial adviser, you should carefully consider whether the product is suitable for you. You are fully responsible for your investment decision, including whether the unit trust is suitable for you. The products/services involved are not principal-protected and you may lose all or part of your original investment amount.

This article is brought to you by Standard Chartered Bank (Singapore) Limited. All information provided is for informational purposes only.