Table of Contents

In a rush? Read the summary:

- While critical illness treatment can be expensive, a critical illness policyholder and the household receive financial protection during those challenging times.

- A critical illness plan can be tailored to the policyholder’s needs and cover a range of situations. By adding a critical illness plan as a rider to a life insurance policy, an individual can improve their current level of protection.

- Before taking a critical illness plan, an individual should consider key points, including the type of plan, the plan’s flexibility, and the stages covered.

Medical treatment can be costly. Treating cancer, heart disease, and numerous other severe conditions requires hospital visits, tests, and possible surgery. While these costs can accumulate rapidly, a critical illness insurance plan can provide the financial protection patients need during challenging times.

What is medical insurance?

Medical and health insurance policies in Malaysia cover the policyholder’s medical and healthcare expenses resulting from injury or illness, in exchange for a premium. These policies typically cover medical, surgical, and hospitalisation expenses, as well as doctor consultation fees, medications, and care providers. Coverages can vary by policy.

Critical illness insurance is designed to provide financial protection if the policyholder is diagnosed with a covered critical illness. These illnesses typically include cancer, stroke, and heart attack. Upon diagnosis, the insured receives a lump sum to cover day-to-day living expenses, like utility bills and mortgage payments, not just treatment costs.

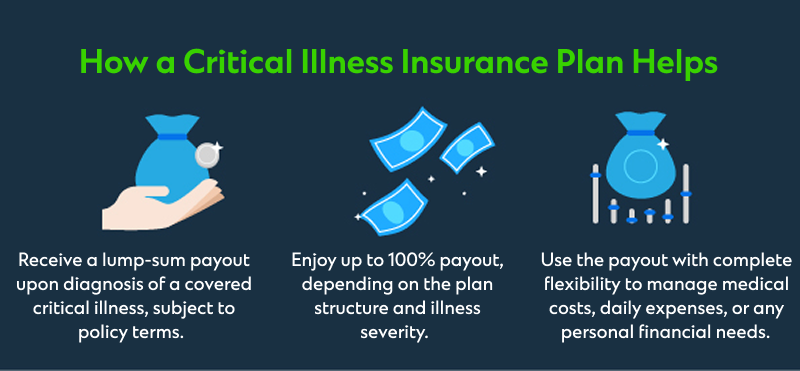

How can a critical illness insurance help the policy holder

Given the potential lifestyle and financial disruptions caused by critical illness and the high medical costs in Malaysia, a critical illness insurance can be a crucial safeguard. For instance, while cancer treatment in Malaysia can cost up to RM 395000, a single PET scan can be as high as RM 3000 per scan. A robust critical illness insurance plan can provide comprehensive financial protection for the household when the breadwinner faces a serious health challenge.

An integrated critical illness policy offers a lump-sum payout that is not restricted to medical bills. The policyholder can allocate these funds toward loss of income during recovery, necessary lifestyle changes, and covering daily living expenses.

A critical illness plan can cover a range of conditions, and it can be customised based on the policyholder’s needs. A person can enhance existing protection by adding a critical illness plan as a rider to a life insurance policy.

Selecting a health insurance policy: Key points to consider

- Genetic predisposition and family history: Before taking an insurance policy, individuals should check their family medical history and medical conditions to ensure the policy provides sufficient payout to cover living expenses, especially given any known familial health risks.

- Type of plan: The number of claims a policyholder is permitted to claim under a critical illness insurance policy depends on the particular type of plan. A policyholder can make only a single claim under a single-claim policy type. In contrast, a multiple-claim policy covers multiple illnesses and provides additional protection for medical emergencies.

- Balancing cost and coverage: While affordable premiums are important, cost should not be the sole consideration. The policyholder should strike a proper balance between the budget and the comprehensiveness of the coverage provided.

- Flexibility of a plan: Before buying a policy, individuals should find out if it allows for increasing coverage annually. A person can achieve flexibility by purchasing a new top-up or add-on policy or by increasing the sum assured during policy renewal, though this would increase premiums too.

- The stages covered: There are four types of critical illness insurance plans, namely, early-stage, basic, single-pay, and multi-pay plans. Early-stage plans allow policyholders to make a partial claim regardless of severity, while basic plans only offer coverage during the most severe (late) stages of illness. Single-pay plans offer a lump-sum payment upon diagnosis, while multi-pay plans offer multiple payouts upon diagnosis.

- Stipulating a waiting period: Many critical illness plans include a waiting period (a defined time after policy purchase before benefits are paid) and a survival period (a period the insured must survive after diagnosis to receive the payout), both subject to the specific terms of the plan.

- Death benefit inclusion: The policyholder should clarify whether the plan includes a death benefit and, if so, the payout structure.

A critical illness can have a devastating effect on anyone’s life and put a strain on the family’s finances. While no one can guarantee freedom from severe disease, a critical illness policy ensures the policyholder protects themselves and their loved ones from its devastating financial consequences.

To get started, kindly leave your contact information here and one of our Relationship Managers will get in touch with you.