Table of Contents

Short on time? Here’s what to expect from the article:

- Islamic banking returns are based on Shariah principles, which are without any interest (riba).

- Common contracts (Murabahah, Ijarah, Mudarabah, Musyarakah) mirror trade, leasing and partnerships.

- Conventional banking relies on interest and shifts most risks to customers.

The Islamic banking sector in Malaysia is steadily growing, with more and more people showing interest in Islamic finance practices. Most people know that Islamic banking is designed to adhere to Shariah law, but not as many may be familiar with its emphasis on transparency, fairness, and even profit and loss sharing. Explore the differences between Islamic and conventional banking principles and practices below.

What is Islamic banking?

Islamic banking refers to a system of banking that complies with Islamic law also known as Shariah law. The underlying principles that govern Islamic banking are mutual risk and profit sharing between parties, the assurance of fairness for all and that transactions are based on an underlying business activity or asset. Learn more on our Islamic banking guidelines page.

What is conventional banking?

This banking system is primarily based on the income generated from interest. The bank allows deposits from customers, provides loans, and earns profits based on the interest and fees charged. The focus is on profitability with fewer restrictions on investment activities.

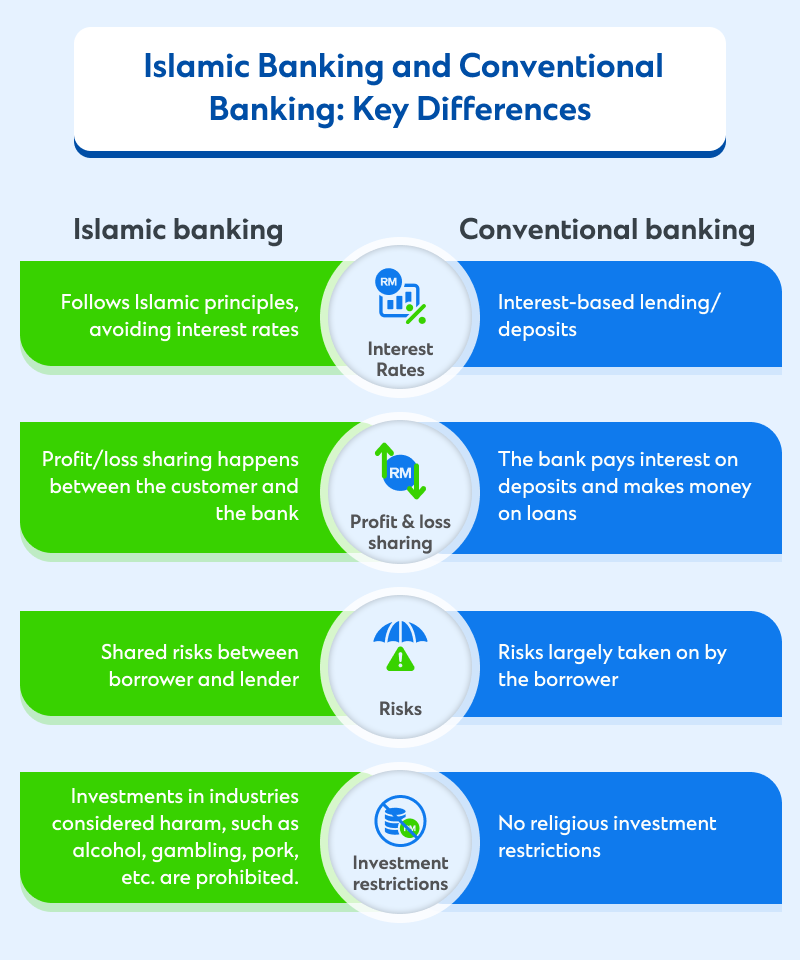

Key differences between Islamic and conventional banking

Here’s how the two approaches to banking differ.

| Theme | Islamic banking | Conventional banking |

| Interest | Interest charges are not allowed. Return based on profit | Interest-based lending/deposits |

| Profit and loss | Fund utilised in partnership which involves profit and loss sharing between the customer and the bank | The bank pays interest on deposits and charge interest on loans |

| Risks | Apply risk sharing element between bank and customer | Risks largely taken on by the borrower |

| Investment restrictions | Investments only in Shariah compliant industries and sector. | No investment restrictions |

Profit vs. interest

- Islamic banking: Relies on cost-plus selling, profit-and-loss sharing contracts and leasing agreements to earn profits. The bank makes a profit through mark-ups, rentals, or shared investment returns instead of charging interest.

- Conventional banking: Allows both lending and borrowing based on interest rates. Loans are issued with a fixed or floating interest rate. Banks earn income from interest charged on borrowings.

Risk sharing

- Islamic banking: Both the bank and the customer share in potential risks and rewards. For instance, in musyarakah (joint ventures), profits and losses are shared proportionally to investments.

- Conventional banking: Customers agree to take on the risks associated with loans and investments. They typically repay both principal and interest on loans, irrespective of their personal finances.

Asset-backed financing

- Islamic banking: Based on trading using real assets such as commodity for Commodity Murabahah (CM) or property for Ijarah (lease). As an example, Ijarah (lease) contract allows banks to rent out assets and earn rental payment as income.

- Conventional banking: loans are purely based on monetary exchange and interest charge without trading activity in real assets.

Ethical investment

- Islamic banking: Islamic banks follow the practice of investing in businesses that do not promote Shariah non-compliant activities/products such as alcohol, pork, gambling, tobacco, military equipment (arms) and more.

- Conventional banking: There are no restrictions; investments are made based on profitability, legal compliance, and risk-return profiles.

The benefits of Islamic and conventional banking

Each approach has advantages worth noting. Conventional banking is more popular as it is profit-focused, however Islamic banking offer customers ethical banking with transparency. The latter focuses on socially responsible finance and practicing Muslims get peace of mind as their banking practices are in-line with Shariah laws as all products and services follow Shariah principles, which prohibit interest and unethical industries.

Conventional banking offers an array of financial and investment products, from credits to loans and savings accounts. Experienced investors can even opt for high-risk, high-profit investment opportunities which is not available in Shariah-compliant banking.

In Islamic banking, however, financing contracts like mudarabah (profit-sharing) and musharakah (partnership) ensure that risks are proportionately spread between the bank and the customer. This reduces the financial burden on borrowers compared to conventional loans, where repayment is required regardless of outcomes.

While conventional banking offers customers flexibility in borrowing, Islamic financing is relied on real trading activity using real assets. Customers benefit from safer, more transparent structures that avoid speculation, and more stable and expect sustainable returns.

How to choose between Islamic and conventional banking

The decision between Islamic banking and conventional banking ultimately depends on an individual’s preference such as personal views, faith values and consideration towards financial appetite and risks. Islamic banking is a perfect solution to those who concerns on following their faith; however, it may also be the preferred choice for individuals who have a strong focus on ethical investments and prefer greater transparency but still earn the desired returns.

On the other hand, conventional banking may be well suited to people who are looking for higher returns without worries to any restrictions or want more opportunities to access conventional loans and credit.

To get started, kindly leave your contact information on the lead form and one of our Relationship Managers will get in touch with you.