Table of Contents

- Investment grade vs high yield: Understanding risk classifications

- Investment-grade bonds vs junk bonds: Local & international agencies

- Investment grade versus high yield: Definition

- Government bonds investment grade

- Investing in investment-grade bonds and high-yield bonds: Economic insights

- Interest rate and its effects on a bond's rating

In a rush? Read the summary:

- Corporate bonds are categorised as investment grade or highly yield bonds. It offers the potential for higher returns but greater risk.

- High-yield bonds suit younger investors with longer time horizons, while investment-grade instruments are favoured by older investors.

- Investment-grade bonds generally have higher durations, making them more sensitive to interest rate changes.

Fixed-income investors usually aim to assess a bond’s risk profile. Corporate bonds typically fall into two primary risk classifications: investment-grade and high-yield.

Investment grade vs high yield: Understanding risk classifications

Since bonds are classified by risk, investment-grade bonds tend to be less risky than high-yield bonds and usually deliver lower returns. High-yield bonds may be riskier because the issuer is at an increased risk of default. As a result, companies usually pay higher coupons due to the uncertainty associated with their debt. For instance, bonds issued by an ambitious real estate developer, a relatively new technology company, or a start-up would probably be categorised as high yield.

Different types of bonds usually attract different investors. For example, investors in their 20s with a long-term investment horizon may include high-yield bonds in their diversified portfolio, while a low-risk investor nearing retirement would prefer to preserve capital and might invest in investment-grade bonds such as Malaysian Government Securities (MGS).

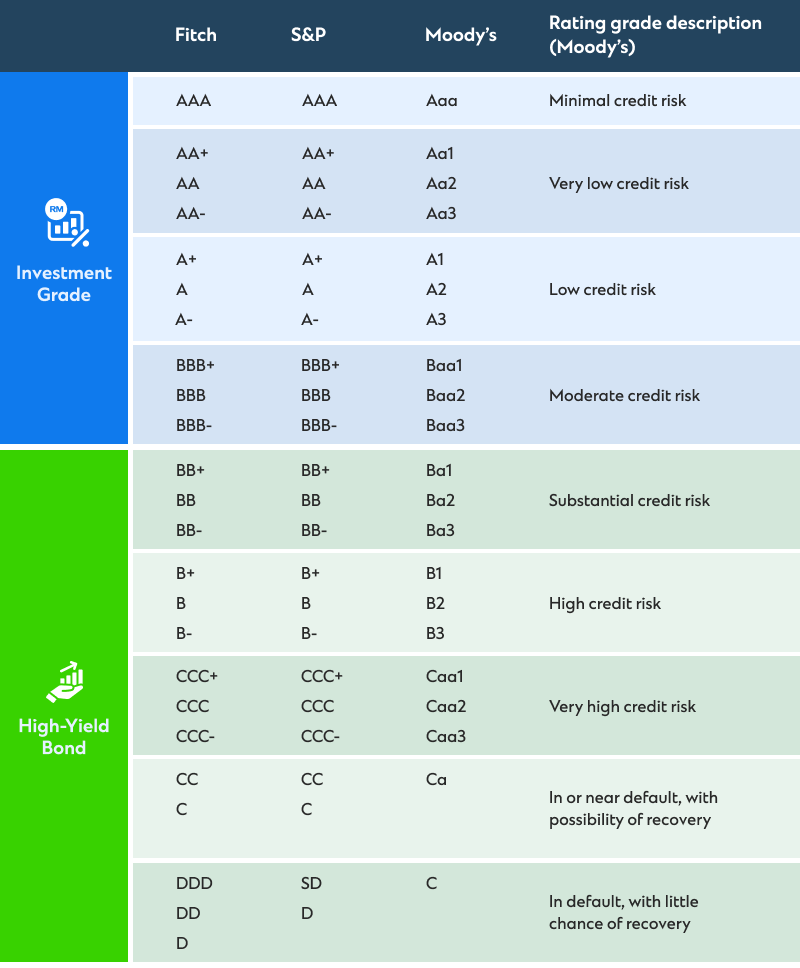

Investment-grade bonds vs junk bonds: Local & international agencies

Evaluating a bond’s risk profile is often straightforward, as external credit rating agencies typically conduct detailed research. In Malaysia, the three most significant international rating agencies are Moody’s, Fitch, and Standard & Poor’s (S&P). On the other hand, domestic investors usually rely on two security commissions (SC)-approved agencies: Malaysian Rating Corporation Bhd (MARC) and RAM Ratings. These agencies typically assess the bond market to determine which bonds can be classified as high yield or investment grade.

Investment grade versus high yield: Definition

According to S&P’s classification system, credit ratings are assigned based on the risk of default on capital repayments. Depending on one of the three letters, including ‘AAA’, ‘BB’, and ‘C’, the rating is given. It is further classified by ‘+’ and ‘-‘ signs.

While bonds with a good credit rating (at least BBB) are categorised as investment grade, bonds with ratings below BBB are referred to as high yield (also known as speculative or junk bonds). Investors should keep in mind that Moody’s rating system sometimes differs from those of S&P and Fitch. But generally, it is comparable.

Government bonds investment grade

Government bonds are also classified in much the same way. Therefore, depending on a country’s sovereign credit rating, Malaysian Government Securities can be rated investment grade, while debt from nations with greater default risk might be deemed high yield.

Some institutional investors, such as pension funds, are usually scale-bound when choosing bonds for their portfolios. Distinguishing between high-yield instruments and investment-grade bonds is crucial. For example, the employee provident fund (EPF) in Malaysia is subject to particular investment mandates.

To manage risk and return, EPF’s internal asset allocations and the funds available through the members’ investment scheme or i-invest hold a combination of lower-risk assets, such as government and investment-grade bonds, along with a proportionately large number of higher-risk assets, such as equity and high-yield instruments.

Remember, a bond’s credit rating may also be updated or downgraded over time. So, an investment rate can also become a high-yield bond.

Investing in investment-grade bonds and high-yield bonds: Economic insights

In a deteriorating economic environment, investment-grade bonds are usually favoured as investors seek safety. On the other hand, in a buoyant condition, bond demand usually rises. Additionally, high-yield bonds typically outperform low-yield bonds or investment-grade bonds amid stronger global growth.

Interest rate and its effects on a bond’s rating

Duration, typically expressed in years, is a time-weighted measure of a bond’s expected cash flows, including coupon payments and the return of principal at maturity. While bonds with longer duration usually exhibit greater sensitivity to actual or anticipated changes in interest rates, bonds with shorter duration act the opposite.

The largest share of investment-grade bonds’ total cash flow comes from the principal repayment at maturity. That is why these bonds usually carry a higher duration. The most attractive instruments resemble high-quality Government bonds and tend to have an average duration.

On the other hand, in the case of high-yield bonds with shorter maturities, the distributor receives a larger share of returns through coupons. As a result, these instruments are typically less affected by expected interest rate increases. However, when interest rates fall or are expected to decline, high-yield bond prices usually rise by a smaller margin than investment-grade bond prices.

To get started, kindly leave your contact information here and one of our Relationship Managers will get in touch with you.