Table of Contents

Short on time? Here’s what to expect from the article:

- The US dollar remains strong due to its extensive investment opportunities and prominence in global trade.

- A weakening dollar can impact how the Malaysian ringgit performs, affecting import costs and the competitiveness of exports.

- Malaysian investors should focus on managing true currency risk through diversification,dollar-costaveraging, and careful analysis.

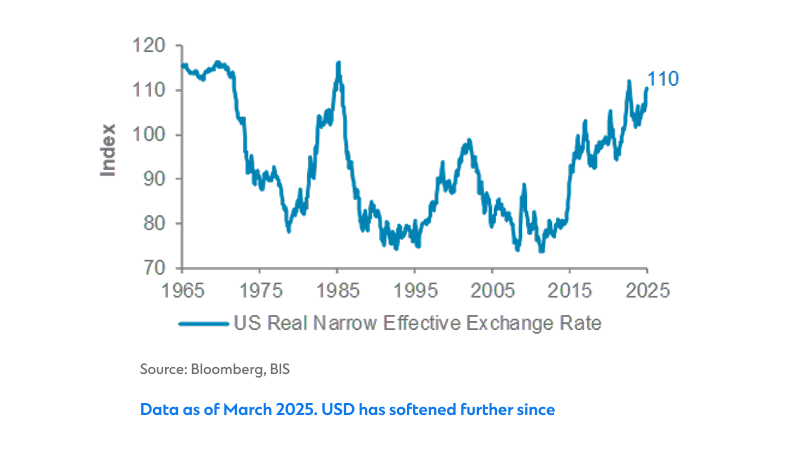

The US dollar remains at a relatively high value by several metrics, owing to the breadth of investment opportunities the currency offers. Investors prefer the US dollar for potential capital appreciation, with instruments such as equities and high-yield bonds, or even to ensure capital preservation by parking their money in high-quality assets such as government bonds. This is owing to the free movement of capital offered by the US, making the Dollar the dominant currency in payments for trade and as a vehicle to hold reserves globally.

That said, however, amidst constant fluctuation in capital and foreign exchange markets, will the US dollar continue to be the most dominant and highly valued currency? With the ongoing geopolitical and economic uncertainty, the world over, many investors, especially in emerging markets such as Malaysia, are now paying attention to how the fluctuation of the US dollar impacts other currencies and shapes their portfolios. There is, therefore, a growing interest in scenarios wherein the Malaysian ringgit strengthens as US dollar weakens.

Dollar fluctuation: Its global role vs its value

Separating the dollar’s structural role from its valuation cycles helps make sense of what the weakening dollar could mean for your investments and savings. The US dollar is prominent in global trading and as a store of value and reserve currency. Malaysian investors often hold US dollar assets for global exposure, stability, and access to extensive financial markets. The US dollar’s dominance for local investors is not expected to change anytime soon.

But this does not imply that it is immune to cycles. Valuations tend to shift over multi-year horizons, and they impact how the Malaysian ringgit trades. A weakening dollar often lifts the ringgit, though the actual impact depends on Malaysia’s economic conditions.

What a weakening dollar means for the Malaysian ringgit

The weakening of the US Dollar and the subsequent strengthening of the Malaysian ringgit may have mixed effects. A softer dollar can help the US reduce its trade deficits, but it could make exports more expensive in Malaysia. However, a stronger ringgit could also lower the cost of imported raw materials, which are vital to many Malaysian manufacturers, helping reduce production costs.

The strengthening of the ringgit against the US dollar has been influenced by several factors, including fed rate cuts, shifts in US monetary policy, foreign purchase of Malaysian securities, and investment incentives. As a result, economists have predicted the ringgit to maintain its upswing. As the ringgit’s value rises, Malaysian investors face opportunities for capital gains in local bonds and export-oriented stocks.

How to navigate currency fluctuations: A primer for the Malaysian investor

When things get uncertain, it is natural for investors to want to take some action. But before you jump in, it helps to pause and get some perspective.

When you look at your investments, what really matters is the true currency risk, the risk that your returns could change simply because one currency rises or falls. For instance, many Malaysian investors hold US stocks. Even though these stocks are priced in US dollars, nearly 40% of S&P 500 revenues come from non-US sources. This offers a natural hedge for local portfolios. To further cushion yourself against sudden swings, consider the following strategies:

Dollar-cost averaging

This means you invest a fixed amount regularly, irrespective of market fluctuations.

Diversification

It is not recommended to rely solely on the US dollar. One may consider spreading investments across different currencies to reduce overall risk.

It is crucial to look beyond the surface level of fixed income. Although products like bonds may be dollar-denominated, a thorough analysis of the true exposure is essential, as the underlying income streams are often non-USD or internationally diversified.

For example, a USD-denominated bond might pay returns sourced from multiple international markets, not just the US. One of the best ways to protect yourself from sudden currency fluctuations is simply to keep your money invested across a variety of assets.

Currency fluctuation is part of global forex trading. The strengthening of the Malaysian ringgit can create both opportunities and uncertainty. It is therefore essential to understand the impact of these shifts on your investment portfolio.

One must focus less on chasing short-term currency trends and more on building a diversified portfolio that can withstand market cycles and provide for long-term value creation. Whether the dollar rises or falls in value, a steady investment regime, diversification, and an understanding of true currency risks help your portfolio’s weather volatility.