Short on time? Here’s what to expect from the article:

- The securitisation process aggregates and converts underlying assets, such as housing loans, hire purchase receivables, or other cash flow-generating contracts, into tradable asset-backed securities (ABS).

- Malaysia’s dual financial system permits both conventional securitisation and Shariah-compliant Sukuk, making it a diverse bond market.

- Securitised credit offers investors potential yield pick-up and diversification, enhanced by protective features such as over collateralisation.

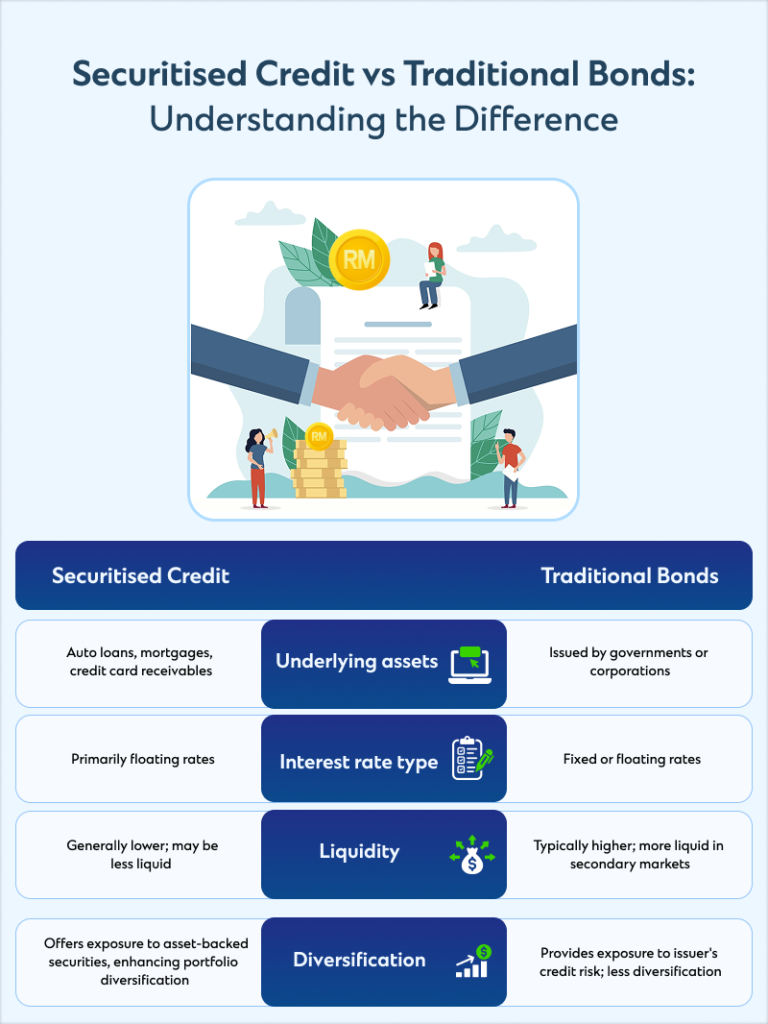

Securitised credit refers to fixed income investments comprising publicly traded bonds or instruments backed by pools of cash-flow-generating contracts, including auto loans, residential and commercial mortgage loans, and credit card loans. These underlying assets are typically aggregated and converted into tradable securities through a process known as securitisation. As a specialised component of fixed income, securitised credit has developed within the broader structure of the Malaysian capital market.

The Malaysian capital market comprises several asset classes, including debt securities, the bond market, the equity market, and financial derivative markets. The securitisation process was introduced in Malaysia in 2001, following the guidelines of the Securities Commission Malaysia (SC) on the offering of asset-backed securities (generated through a securitisation transaction) to strengthen the Malaysian capital market.

Types of securitised credit

The Malaysian bond market offers a range of debt security products, including floating-rate bonds, straight or fixed-rate bonds, asset-backed securities, convertible bonds, and exchangeable bonds. Malaysia is also a key Islamic financial centre that offers a wide variety of Islamic capital market securities, including Shariah-compliant Sukuk.

- Collateralised Loan Obligations (CLOs) are debt securities backed by a pool of corporate loans that are actively managed by professional CLO managers who adjust the portfolio to optimise returns and manage risks.

- Asset Backed Securities (ABS) are debt securities created when the cash flows are derived from a pool of underlying assets, including credit card receivables, auto loans, and other personal loans.

- Mortgage-Backed Securities (MBS) are securities backed by a pool of commercial mortgage loans. The cash flow comes from the payments from the commercial property owners. It is segmented into a few key types.

- Residential Mortgage-Backed Securities (RMBS) are a significant type of MBS, backed explicitly by pools of mortgages on residential properties, such as housing loans, credit card receivables, higher purchase loans, loan receivables, billing materials, etc.

- Commercial Mortgage-Backed Securities (CMBS) are financial instruments backed by mortgages on commercial properties. Investors seeking returns from the commercial real estate sector typically invest in it.

- Collateralised Debt Obligations (CDOs) are a unique and more intricate type of asset-backed securities in which new pools of debt are formed by reconstructing and restructuring existing loans.

- Asset Backed Commercial Paper (ABCP) is a short-term ABS with a maturity of one year or less. These are backed by various assets, including leases, margin loans, and short-term trade receivables.

Reasons to choose securitised credit investments

Yield pick-up

Securitised credit often provides a higher yield compared to conventional bond instruments of similar credit quality.

Exposure to floating rates

Due to their floating-rate nature, securitised credit instruments typically provide a spread above a short-term reference interest rate, which allows the yield to track changes in market interest rates.

Space for price appreciation

As a credit instrument, when interest rates decline, Securitised Credit spreads tend to benefit, leading to tighter spreads. Since the 2020 COVID period, these spreads have remained relatively wider than those of traditional fixed-income instruments, creating potential for further price gains.

Credit enhancement

Securitised Credit structures include protective features such as stricter covenants and overcollateralisation and serve as a buffer against potential collateral losses.

Diversification advantages

Securitised Credit has little correlation with other bonds and can enhance portfolio diversification within the bond allocation.

Overall, while securitised credit provides potential for returns and portfolio diversification benefits, investors should keep in mind that it is not risk-free. Interest rate volatility, credit default, liquidity shortages, and structural complexity are factors that can influence performance. A profound understanding of these risks is essential for making informed investment decisions related to asset class.

To get started, kindly leave your contact information here and one of our Relationship Managers will get in touch with you.