Table of Contents

Short on time? Here’s what to expect from the article:

• Islamic wealth management focuses on Shariah-compliant investments and avoid interest-based income.

• It promotes risk-sharing models that support responsible and transparent wealth growth.

• It also includes estate planning and charitable deeds like Zakat and Waqf that offer an ethical yet comprehensive avenue for wealth creation while staying true to one’s values.

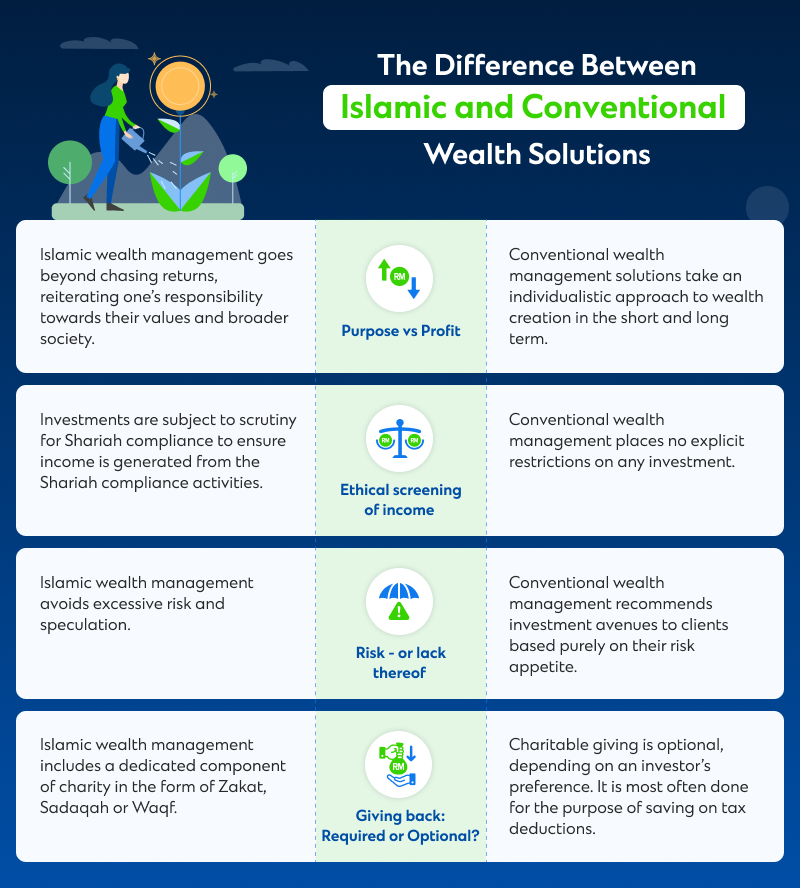

In a world driven by faith and ethical values as much as it is by money, wealth management has evolved beyond just chasing returns. It now also attempts to align one’s finances with impact and faith-based goals, and the greater good. In this context, Islamic wealth management has emerged as a compelling approach for individuals looking to grow and preserve their wealth ethically to reflect their values.

The key principles of Islamic wealth management

Rooted in the ethical frameworks of Shariah law, at the heart of Islamic wealth management are seven guiding principles designed to ensure wealth is grown, preserved and passed on with integrity.

Shariah compliance

Every investment made under the ambit of Islamic wealth management must comply with Shariah law. Therefore, investing in and/or financing activities in industries involved in alcohol, gambling, entertainment, tobacco, pork, or even the production of munition is not permitted.

Avoidance of interest income

Interest refers to an excess amount derived from lending or borrowing transactions. The interest returns not tied to risk, labour, or productivity. This can include interest on loans or return in deposits wherein money yields more money with the passage of time. Any such investments are prohibited as they benefit the lender at the expense of the borrower, allowing for income without any effort.

Risk sharing

Islamic wealth management accentuates profit-and-loss-sharing arrangements between partners, such as Mudarabah (Profit-sharing) and Musyarakah (Partnership).

Mudarabah refers to a contract between a capital provider (rabbul mal) and an entrepreneur (mudarib), wherein profit is shared between the two parties according to a mutually agreed-upon profit-sharing ratio (PSR). The capital provider bears losses as long as they are not caused by misconduct or negligence on the part of the entrepreneur.

Musyarakah refers to a partnership between two or more parties, whereby all parties will share the profit and bear the loss from the partnership.

Ethical investments

Emphasis is placed on tangible investments in sectors mutually beneficial to the investor and the larger society. Shariah-compliant investments cover a wide range of sectors and industries such as healthcare, technology, education, renewable energy, and the like.

Giving back

Zakat, one of the five pillars of Islam, aims to purify one’s wealth and become mandatory to individual who met the zakat requirement to pay the zakat through zakat institutions or specific eligible recipient (asnaf). It becomes mandatory only when the value of one’s assets exceeds a threshold known as Nisab.

Another form of charity prevalent in Islam is referred to as Sadaqah. These donations, unlike Zakat, are entirely voluntary and can be made at any point in a financial year, as and when one chooses to do so.

Charity can also be done in the form of Waqf, which involves donating assets to a charitable cause. These assets are held in trust and cannot be sold or transferred again. Instead, they’re used to benefiting society or generating income for charitable purposes in perpetuity. This may include cash Waqf that can later be used for projects such as the construction of schools, hospitals, community centers and commercial buildings to generate return, as well as Waqf in the form of fix assets such as land, property and the like.

Takaful coverage

Takaful (also known as Islamic Insurance or Takaful Insurance), refers to a coverage benefit for any misfortunes based on cooperation and mutual assistance. In essence, participants contribute their funds in a pool that is managed by a Takaful operator under the contract of Wakalah (agency) and Tabarru (donation) for the purpose providing assistance to other participants in need.

This arrangement is free from Riba (Interest), Gharar (Uncertainty), and Maisir (Gambling). The funds are also then invested in Shariah-compliant businesses to grow and provide financial assistance to anyone who may require it, whether due to accidents, illnesses, natural disasters, or otherwise.

Estate planning

Islamic wealth management accords great importance to estate planning via Wasiat (last will and testament) to ensure equitable distribution of wealth amongst one’s kin after one’s passing.

This can also be done via Hibah or gift giving, which involves voluntarily transferring ownership of one’s assets to recipients without consideration to ensure smooth asset transfer and avoid dispute in wealth’s distribution.

These instruments allow one to safeguard their assets and ensure their wishes are honoured after their passing, preserving harmony and financial stability in the family aross generations.

Standard Chartered bank and Islamic banking: A 32-year-long legacy

Standard Chartered Bank offers you over three decades of expertise with Islamic Banking products, with integration of Standard Chartered Sadiq Berhad in 2008 as a full-fledged Islamic banking subsidiary. Our services are open to all who seek ethical, transparent, and value-driven financial solutions, regardless of their faith.

Some of our Islamic personal banking products include Shariah-compliant home financing plans like Saadiq My HomeOne‑i (a diminishing partnership home financing solution) as well as deposit products like Term Deposit‑i (a Shariah-compliant fixed deposit).

Islamic wealth management is a comprehensive wealth solution that offers a value-driven approach to growing, preserving, and passing on wealth, grounded in the moral and ethical frameworks of Shariah. It can provide for both capital appreciation and a stable income; while helping one fulfill one’s obligations towards society as a whole.

To get started, leave your contact information on the lead form and one of our Relationship Managers will get in touch with you.