Table of Contents

Medical treatment can cost a prohibitively large sum. Treating cancer or heart disease or dozens of other serious illnesses can involve hospital visits, tests and even surgery. The expenses can quickly add up. A critical illness plan can give you the money you need to bear these costs while you get back on your feet.

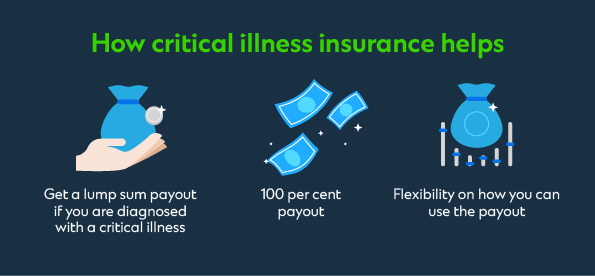

How a critical illness insurance can help

- Get a lump sum payout if you are diagnosed with a critical illness.

- There are 2 types of insurance cover under this category. One is a basic critical illness insurance which generally covers pre-defined critical illnesses. The other is early critical illness insurance, which may cover 100 medical conditions.

- Receive 100 percent payout

- The insurer can pay you the entire sum immediately after the critical illness is diagnosed.

- Flexibility on how you can use the payout

- You have the freedom to use the payout in the way you choose. The money can go towards paying for medical expenses, hospitalisation or alternative treatment expenses. You can even use the funds to pay for your day-to-day living costs.

Key points to consider when choosing a policy

Convinced that you need a critical illness insurance policy? Here are the points to consider when you choose one:

- Check if you are genetically disposed to any critical illnesses. Make sure that the policy you are buying covers these.

- Until what age are you allowed to renew the policy? It’s better to buy a policy that provides coverage for as long as you live.

- Don’t choose the cheapest policy. Strike a good balance between budget and coverage. While cost is a consideration, it shouldn’t be the only one.

- Is it a flexible plan? Some policies allow you to increase the coverage every year. Of course, you’ll have to pay a higher premium.

- What’s the coverage you’re looking for? The Life Insurance Association (LIA) 2022 Protection Gap Study suggested 4 times of your annual income based on a 5-year CI recovery period.

- What are the stages covered – from early to advanced? Some policies give you a lump sum as soon as the illness is diagnosed. Others wait until the disease reaches a ‘severe’ or ‘extremely severe’ stage.

- Death Benefit – Does the policy include a death benefit? What’s the amount that you’ll receive?

A critical illness can have a devastating effect on your life. It can also put a strain on the family’s finances. While nobody can guarantee that you’ll never get a serious disease, at least you can protect yourself from its financial consequences.

If you haven’t bought a critical illness insurance policy yet, maybe it’s time you did. The extra money it can provide could help you to meet new costs and provide a cash cushion for unforeseen expense.