Table of Contents

In a hurry? Read this summary:

- Recurring deposits are schemes offered by banks wherein one earns a fixed interest on periodic deposits made into them via their accounts in the same bank.

- Systematic Investment Plans refer to investing pre-determined amounts of one’s choosing into mutual fund schemes at a set frequency. They focus on wealth creation by leveraging the power of compounding and rupee cost averaging.

- Choosing between the two requires one to factor in the flexibility they offer, one’s liquidity preferences, risk profiles as well as investment horizon.

Attaining financial security is not just about having a stable income. It is also about developing a habit of consistently saving and investing your money over time, to take care of long-term financial goals such as your children’s education, buying a home, or planning for retirement such that they do not prove to be a burden later.

For this, two tools can make all the difference. Namely, recurring deposits and systematic investment plans. In this article, we will take you through how they aid financial security, their benefits, and how they support different kinds of financial goals.

An overview of what Recurring Deposits are and how they work

Recurring deposits (RDs) are savings schemes offered by banks, wherein one can make periodic deposits (usually monthly) and earn interest on them. RDs are linked to one’s savings account in the same bank, for these deposits to be debited automatically from a specific date of each month.

Interest rates are fixed at the time of opening one’s RD account and remain unchanged throughout the tenure of one’s investment. This interest is compounded quarterly and paid back to investors along with their principal amount at the time of maturity.

However, bear in mind that while RDs may provide stable returns, owing to the fixed interest rate, they may be unable to provide inflation-beating returns over time.

Exploring Systematic Investment Plans (SIP)

Systematic investment plans (SIPs) refers to investing a specific amount into mutual fund schemes of your choice, at a pre-determined frequency. They focus on wealth creation through disciplined investing with minimum investment thresholds of as little as ₹500 per month. Moreover, they help with long-term capital appreciation via compounding and can help protect your portfolio against volatility and diminished returns through rupee cost averaging.

Compounding refers to when one consistently invests and reinvests their capital, as well as its returns, which generates increased returns subsequently. This snowball-like growth helps consistent contributions potentially grow at an accelerated pace in the long run.

Rupee cost averaging refers to investing fixed amounts in an SIP, regardless of market conditions. In essence, when the net asset value (NAV) of a fund rises, one gets fewer units; and when it falls, one gets more. This helps lower the average cost per unit over time and helps cushion your portfolio against volatility.

SIP vs Recurring deposits: Key differences

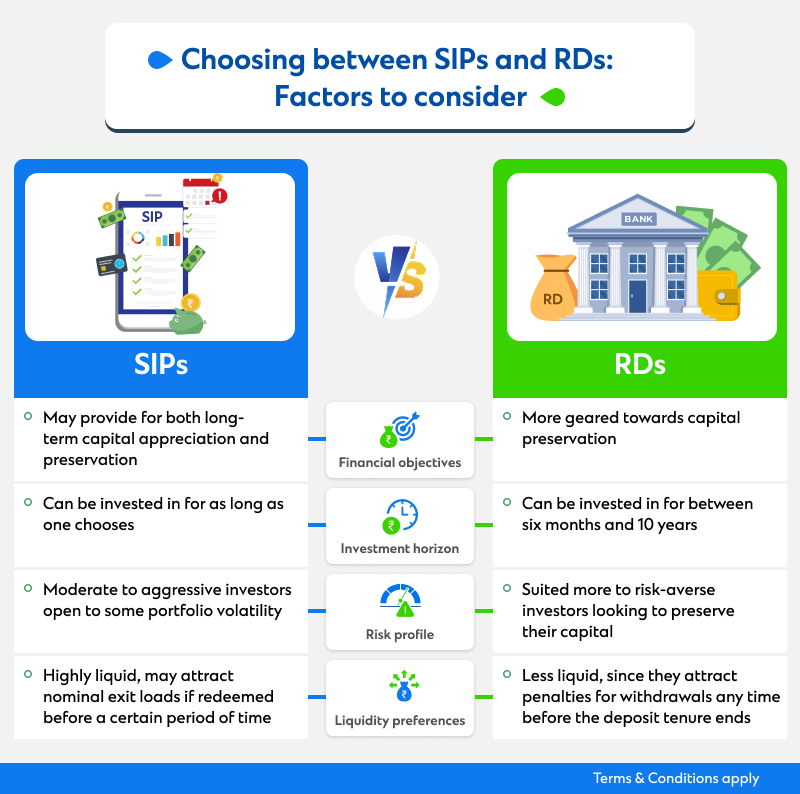

While both RDs and SIPs play a role in long-term wealth creation, providing for both capital appreciation and preservation, there are also several differences between the two. Understanding each of these is crucial to finding the better fit for one’s investment portfolio.

Flexibility

With SIPs, investors can make contributions at a frequency of their choosing — whether monthly, quarterly, or annually. They can also start, stop, or restart their investments anytime.

In contrast, one can make only fixed monthly deposits into an RD. Missed installments attract penalties, and in the case of over three to six payments being skipped, a bank reserves the right to close one’s account.

Liquidity

SIPs allow one to close their account and sell their holdings at any point in time. One can also make full or partial withdrawals, based on their requirements. They attract exit loads (capped at 3% by SEBI) only if one chooses to dissolve their investments before a certain period.

RDs allow for premature withdrawals as well. However, one can typically only make a full withdrawal. Moreover, premature withdrawals incur penalties ranging between 0.5% and 1%.

Risk-return profile

SIP returns are market-linked, which gives them the potential to provide higher returns in the long run, making them more geared towards capital appreciation. At the same time, however, they are also prone to higher volatility levels, depending on the assets they invest in. They are therefore suited to more aggressive investors.

More risk-averse and conservative investors who prioritise capital preservation can consider investing in RDs. This is because RD returns are determined by the interest rates fixed while opening one’s account. These interest rates remain unchanged throughout the RD’s tenure and are not market-linked.

Investment horizon

SIPs have no fixed tenure, and one can choose to invest in mutual funds via them for as long as they like. Investors with both a short and/or long-term investment horizon can invest in them,

RDs have fixed tenures typically ranging between six months and 10 years. They are suited to short, medium or long-term financial goals depending upon the tenure for which one chooses to invest in them.

Regardless of the differences between SIPs and RDs, investment instruments are powerful tools that help one develop patience, discipline, and consistency, when it comes to their savings and investments.