Table of Contents

- SWP vs SIP: Which Mutual Fund Strategy Serves You Better Based on Your Needs?

- SIP vs SWP: Foundational roles in wealth creation and distribution

- What is SWP in mutual funds and how does it work?

- When to use SIP vs when to use SWP

- Integrating SIP and SWP into a long-term investment strategy

- Using an SWP mutual fund calculator

SWP vs SIP: Which Mutual Fund Strategy Serves You Better Based on Your Needs?

In a hurry? Read this summary:

- SIP (systematic investment plan) builds wealth over time. It is best for salaried, goal-focused investors with 5+ year investment horizons.

- SWP (systematic withdrawal plan) provides regular income post-retirement with steady cash flow.

- It’s important to consider your personal finance goals and needs before making a choice.

SIP (systematic investment plan) is a wealth accumulation and creation strategy where the investor makes a recurring payment that goes into a mutual fund. This involves cash outflows.

However, SWP (systematic withdrawal plan) is a facility given to the investor to regularly withdraw funds from mutual fund. This involves cash inflow.

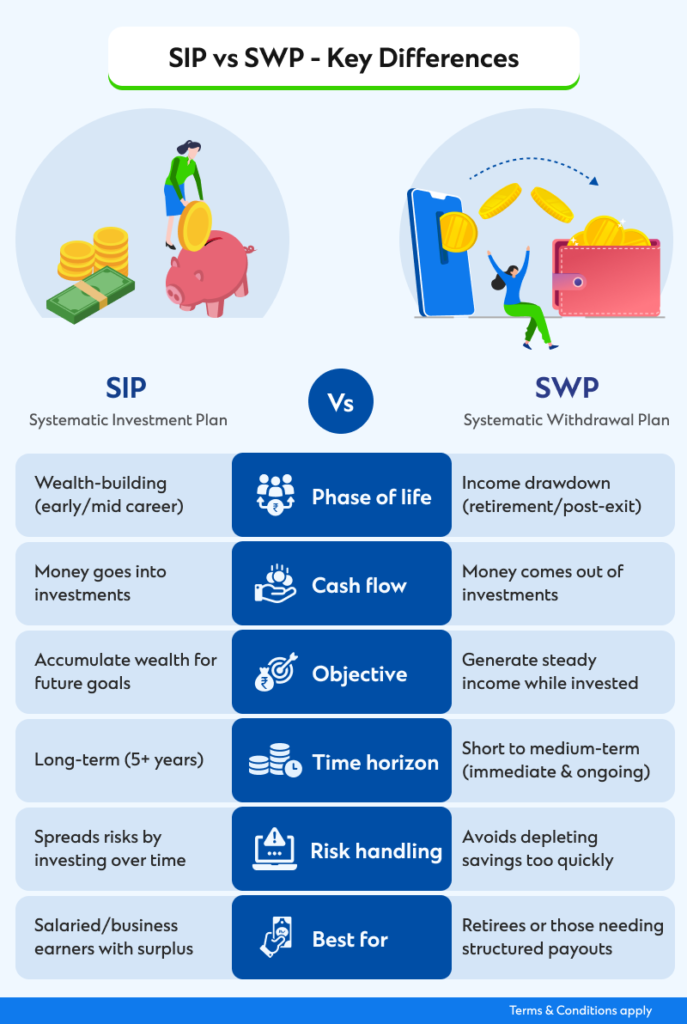

SIP vs SWP: Foundational roles in wealth creation and distribution

SIP and SWP in mutual funds are functionally poles apart. Let’s look at the differences between SIP and SWP.

| Feature | SIP | SWP |

| Purpose | Wealth accumulation | Income generation |

| Cash flow | Cash flows into mutual funds | Cash flows out of mutual funds |

| Suited for | Salaried individuals or goal-based investors | Retirees, passive income seekers, or high-net-worth Individuals |

| Tax impact | Long-term capital gains/Short-term capital gains on fund growth at redemption | Capital gains taxed on each withdrawal |

| Discipline factor | One needs to be highly disciplined financially to make timely SIP payments. | Controlled, predictable drawdown |

What is SWP in mutual funds and how does it work?

A systematic withdrawal plan helps investors withdraw funds regularly in a planned manner. Investors can decide how much money and how frequently they want to withdraw (usually monthly). Once the SWP is set up, the platform owner redeems the required units from the mutual fund holdings and credit the funds in the bank account.

For example, if you’ve accumulated ₹1 crore in a debt mutual fund, you can set up an SWP of ₹50,000 per month. That amount is credited to your account, while the rest continues to generate returns.

Important traits:

- SWPs are not dividends; rather, they are partial redemptions of invested funds

- Investors control the frequency and amount of withdrawals

- Withdrawals can be changed or halted; and depending on the fund type and holding duration

- Each withdrawal is liable to capital gains tax.

Use case:

SWP is perfect for managing cash flow for family-owned businesses, producing income after retirement, and progressively reducing portfolio risk.

When to use SIP vs when to use SWP

Where you are in your financial path determines whether you should use SIP or SWP when it comes to mutual funds.

The best investors for SIP are those who:

- Are in the early stages of accumulating wealth.

- Have extra money each month to invest.

- Set financial objectives for your legacy, education, and housing that are more than five years away.

SWP is most suited for those who:

- Are in the phase following retirement.

- Desire steady income while holding onto your investments.

- Desire to tailor rewards to family requirements or lifestyle.

Integrating SIP and SWP into a long-term investment strategy

Wealth experts frequently advise structuring investment flows across several fund categories using both SIPs and SWPs.

You can use equity mutual funds for SIP. This offers a long investment horizon, significant growth potential, and benefits wealth accumulation.

SWP is applicable to debt and arbitration funds. It is appropriate for consistent income, reduces volatility, and allows for tax-efficient withdrawals.

STPs (Systematic Transfer Plans) are another option for advanced high-net-worth individuals who want to bridge the gap. They put a lump sum in a low-risk fund and then use SIPs to move that money into stocks before switching to SWP in later years.

Lump sum → SIP (via STP) → SWP is a three-step process that guarantees cash flow efficiency, tax optimisation, and long-term continuation.

Using an SWP mutual fund calculator

The following factors are used by an SWP mutual fund calculator to determine how long your corpus can withstand withdrawals:

- The amount of the withdrawal

- The anticipated rate of return

- Duration of investment

- The size of the first corpus

For example, an investor with ₹2 crore invested in a debt fund earning 7% p.a. and withdrawing ₹1 lakh monthly will see the corpus last over 25 years. However, inflation and tax impact must be factored in for realistic planning.

Recommended tool: SC SIP Calculator – while primarily SIP-focused, this can help reverse-engineer corpus planning for future SWPs.

To learn more, connect with our relationship managers or visit SC Investvv and start building your portfolio.