Table of Contents

- What is a hybrid fund and why it matters

- Different types of hybrid funds

- Hybrid funds vs. debt funds vs. equity fund: Which one fits your goals?

- How hybrid mutual funds adapt through market cycles

- What to think about before you invest in a hybrid fund

- Who should opt for hybrid funds?

- Blending strategies: How hybrid funds fit into a diversified portfolio

- Ready to shape your portfolio with balance and growth?

What is a hybrid fund and why it matters

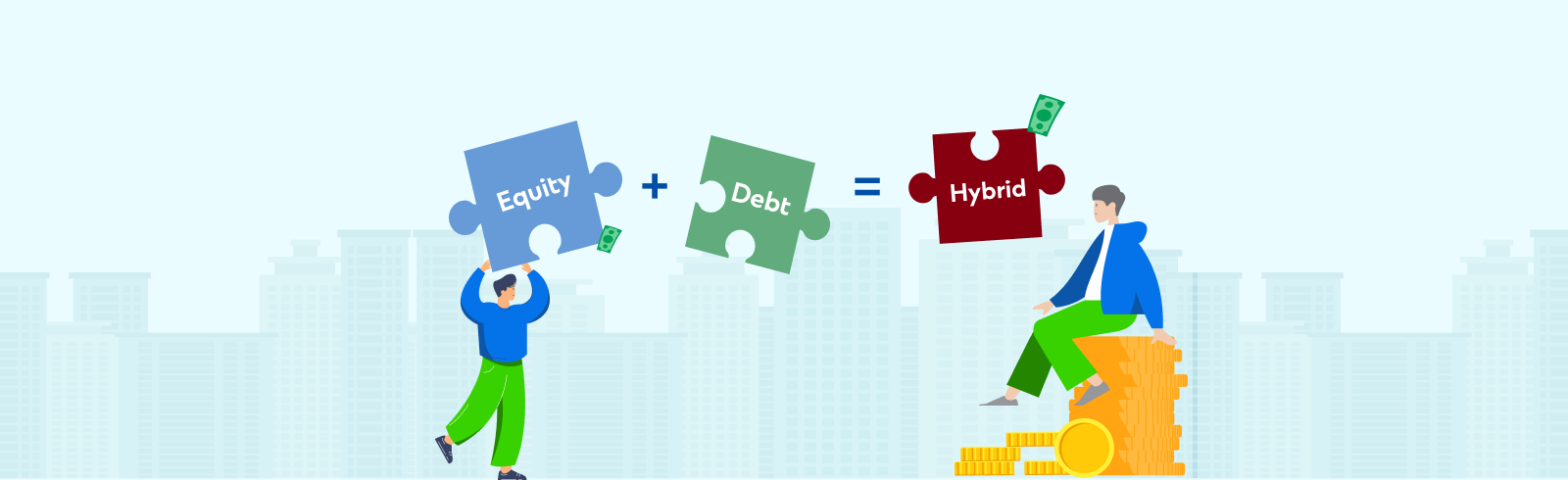

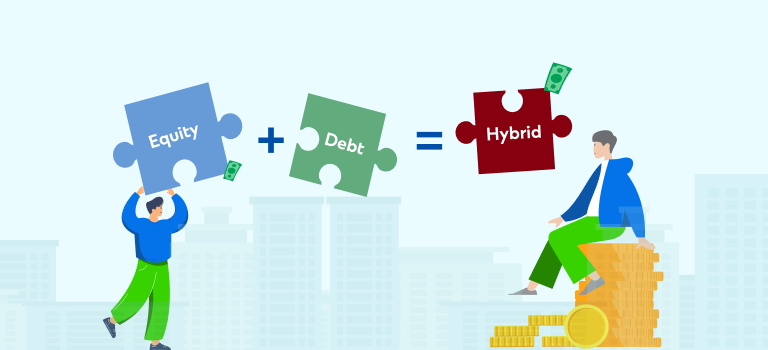

A hybrid mutual fund allocates investor capital between equities (for capital appreciation) and debt instruments (for regular income and lower volatility). This mix helps create more resilient portfolios, reducing stress during market swings. Hybrid funds appeal to investors who prefer a balanced but simplified investment route—without juggling distinct equity and debt allocations.

Different types of hybrid funds

SEBI classifies hybrid funds into distinct categories based on their asset allocation strategies. Each type serves a specific investor need and risk profile. Here’s a breakdown of the most prominent hybrid fund categories and what sets them apart:

Conservative hybrid fund

- Allocation: Typically 75% to 90% in debt and 10% to 25% in equity

- Feature: Prioritises capital preservation with mild equity participation for modest growth

- Best for: Retirees or risk-averse investors seeking steady income with minimal volatility

Balanced hybrid funds

- Allocation: Roughly equal allocation—40% to 60% in both equity and debt

- Feature: Offers a true blend of growth and stability; risk is moderate and returns can be balanced

- Best for: Investors aiming for consistent returns without taking an aggressive stance

Aggressive hybrid funds

- Allocation: Around 65% to 80% in equity, the remainder in debt

- Feature: Designed for long-term wealth creation with lower volatility than pure equity funds

- Best for: Moderately aggressive investors comfortable with market-linked risk

Dynamic asset allocation / balanced advantage funds

- Allocation: No fixed ratio; equity and debt allocations are adjusted dynamically

- Feature: Fund managers shift allocation based on market conditions using valuation models

- Best for: Investors who want professional asset rebalancing and automatic risk moderation

Equity savings funds

- Allocation: Mix of equity, arbitrage, and debt with at least 65% of assets allocated to equity oriented securities (including arbitrage), and a maximum of 10% to debt securities

- Feature: Aims to deliver low volatility returns by leveraging arbitrage opportunities

- Best for: Investors seeking returns with a better risk reward

Aggressive hybrid fund spotlight: Where risk meets reward

Also known as aggressive hybrid funds, these schemes typically invest 65% to 80% in equities and the remainder in debt instruments . The goal is to generate equity-like growth while using the debt portion to moderate short-term market volatility.

What sets them apart is the balance they offer:

- The equity component drives long-term capital appreciation

- The debt buffer lends a level of stability and downside protection, especially during market corrections

For investors who are not ready for the full risk exposure of equity mutual funds , aggressive hybrid funds serve as a practical middle ground. They provide:

- Lower volatility than pure equity funds

- More consistent performance during turbulent market cycles

- Asset-class diversification in a single product, reducing the need for manual rebalancing

Aggressive hybrid funds are well-suited for long-term financial goals such as retirement planning, children’s education, or wealth accumulation over 5 to 10+ years. Their built-in balance makes them particularly attractive for moderately risk-tolerant investors seeking to grow their capital while sleeping peacefully at night.

Hybrid funds vs. debt funds vs. equity fund: Which one fits your goals?

| Feature | Hybrid Funds | Debt Funds | Equity Funds |

| Risk & volatility | Moderate (due to equity-debt mix) | Low (interest-driven stability) | High (market-linked fluctuations) |

| Return potential | Higher than debt; lower than equity | Stable but generally lower than hybrids | Highest long-term potential, but with interim volatility and market-linked losses |

| Ideal time horizon | Medium to long-term (3-7+ years) | Short to medium (1-5 years) | Long-term (5-10+ years) |

| Investor profile | Moderate risk-takers seeking balanced exposure | Conservative investors prioritising capital safety | Aggressive investors seeking long-term capital growth |

How hybrid mutual funds adapt through market cycles

Hybrid mutual funds are designed to manage risk across changing market conditions. During uncertain times—like interest rate spikes or pandemic-led market shocks—their built-in asset mix allows for smoother returns compared to pure equity schemes.

Dynamic asset allocation funds stand out for their ability to adjust equity and debt exposure automatically. This flexibility can help mitigate losses during downturns and capture opportunities during rebounds—making them ideal for investors who prefer a hands-off, balanced strategy.

To explore live data, fund categories, and updated performance metrics, visit our mutual fund platform and browse our range of hybrid schemes.

What to think about before you invest in a hybrid fund

Ask yourself:

- Risk appetite – Can you tolerate moderate swings in equity markets?

- Time horizon – Are you comfortable being invested for 3+ years?

- Objective – Do you need income, growth, or both?

- Preference – Active rebalancing (dynamic funds) or steady autopilot (static hybrids)?

Consider hybrid funds as core portfolio holdings—especially for medium-risk profiles—while complementing them with pure equity or debt schemes.

Who should opt for hybrid funds?

Hybrid funds fit diverse investor profiles. Based on the asset allocation mix of the individual hybrid fund categories, the following investors can consider investing in hybrid funds:

- New investors wary of equity volatility

- Retirees seeking stable income with growth potential

- Goal-oriented investors hesitant about full equity allocation

Choosing the right type:

- Conservative funds if you prefer stability

- Balanced funds for balanced growth-income mix

- Aggressive funds if you lean growth and can tolerate volatility

Blending strategies: How hybrid funds fit into a diversified portfolio

After identifying the hybrid fund that fits your risk appetite and investment goals, the next step is optimising how it sits within your broader portfolio. Hybrid funds aren’t just simplified all-in-one solutions — they can also play a strategic role in achieving asset diversification and long-term balance.

Ready to shape your portfolio with balance and growth?

Hybrid mutual funds can be a powerful yet simplified investment tool—offering a blend of equity upside and fixed-income stability. They are well-suited for diverse goals and risk appetites.

Explore hybrid fund options on SC Invest —our open-architecture platform offering expert-curated hybrid funds, real-time trackability, and seamless transactions.