Liquid Funds 101: What they are and how they work

Learn More Learn More

In a hurry? Read this summary:

In an ever-evolving and dynamic capital market landscape, stability and flexibility have emerged to be just as important as returns for investors. Liquid funds offer one precisely that. These short-term investment instruments offer one a place to productively park and preserve their idle funds while also giving them seamless access to their capital, as and when they require, making them an integral part of investor portfolios the world over today.

In the following sections, we will explore what a liquid fund is, its advantages, and how to invest in one.

Liquid funds are a sub-category of debt mutual funds that invest in a diversified mix of fixed-income instruments such as government and corporate bonds, commercial papers, certificates of deposit, treasury bills, and other such money market instruments. These instruments however, have very short maturities – typically no longer than 91 days. Their main objective is to achieve capital preservation and a stable income, rather than capital appreciation.

Liquid funds have several advantages that align with an investor’s short, as well as long-term needs.

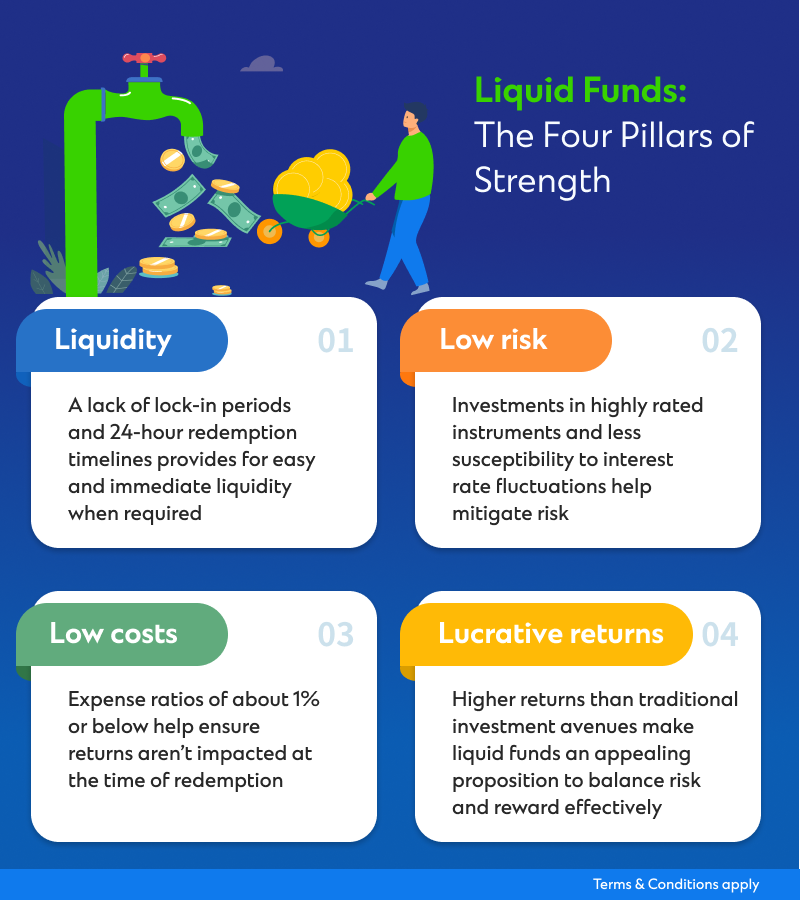

Seamless liquidity

Most liquid funds have no lock-in periods. This ensures quick access to one’s capital, anytime one needs it. Furthermore, redemption timelines on liquid funds are as low as 24 hours in most cases, making them ideal for parking funds for unforeseen contingencies.

Lower risk levels

Liquid funds invest in high-quality debt instruments, often rated A1 or A2 by credit rating agencies such as ICRA (Investment Information and Credit Rating Agency) or CRISIL (Credit Rating Information Services of India Limited). A lack of susceptibility to credit rating changes ensures their portfolio remains protected against major against net asset value (NAV) fluctuations, whereas a short investment horizon also ensures reduced susceptibility to interest rate fluctuations, making them a suited to conservative investors.

Expense ratios and exit loads

As per the rules of the Securities and Exchange Board of India (SEBI), expense ratios on liquid funds are capped at 1.05% of their daily NAV. This ensures that returns aren’t significantly diminished when one chooses to redeem their investments. Additionally, exit loads on liquid funds are also capped at just 0.0070% by SEBI, further enhancing capital preservation.

Potentially higher returns than savings accounts

Liquid funds’ performance is market linked. With changes in interest rates, their NAVs see an increase as well. This allows them to potentially provide one with higher returns as compared to savings accounts or fixed deposits. Bear in mind however, they are also susceptible to negative credit rating and interest rate fluctuations, which may impact returns.

How to Choose Mutual Funds: Insights for Savvy Investors

Standard Chartered Bank, India (‘Bank’) is an AMFI-registered distributor of mutual funds and referrer of other third-party investment products and does not provide any investment advisory services as defined under the SEBI (Investment Advisers) Regulations, 2013. Mutual fund investments are subject to market risks, please read scheme related documents carefully before investing. Past performance is not indicative of future returns. Apart from the RM-assisted journey, SC Invest is an EXECUTION-ONLY platform. The Bank does not provide any investment advice or investment recommendations in respect of any transaction effected through the SC Invest platform.

The contents on this webpage are for general information only and does not constitute an offer, recommendation or solicitation of an offer to enter into a transaction or adopt any hedging, trading or investment strategy, nor does it constitute any prediction of likely future movements in rates or prices or any representation that any such future movements will not exceed those shown in any illustration. You are fully responsible for your investment decision, including whether the product or service described here is suitable for you. Standard Chartered Bank will not accept any responsibility or liability of any kind, with respect to the accuracy or completeness of the information in this webpage. The contents herein are for general evaluation only and has not been prepared to be suitable for any particular person or class of persons. Standard Chartered Bank makes no representation or warranty of any kind, express, implied or statutory regarding the contents on this webpage or any information contained or referred to herein. This webpage is distributed on the express understanding that, whilst the information in it is believed to be reliable, it has not been independently verified by us.

This communication has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. Standard Chartered Bank India (“SCB/ Bank”) does not warrant its completeness and accuracy. This information is not intended as an offer or solicitation for the purchase or sale of any financial instrument / units of Mutual Fund. Recipients of this information should rely on their own investigations and take their own professional advice. Neither SCB/Bank nor any of its employees shall be liable for any direct, indirect, special, incidental, consequential, punitive or exemplary damages, including lost profits arising in any way from the information contained in this material. SCB Bank and its affiliates, officers, directors, key managerial persons and employees, including persons involved in the preparation or issuance of this material may, from time to time, have investments / positions in Mutual Funds / schemes referred in the document.

Standard Chartered Bank (“SCB/ Bank”) is a AMFI-registered Mutual Fund Distributor & a Corporate Agent for Insurance products.