Table of Contents

In a rush? Read the summary:

- Parents can offer guidance on financial habits to help their children transition into adulthood.

- Parents can provide their kids with the right financial education before letting them take charge of their future.

- Early planning for retirement is critical in ensuring that parents have the means to take care of their own well-being while their children advance towards achieving their milestones.

Teaching children the steps to financial security

As children enter the workforce and step into adulthood, many parents naturally wonder if they are financially prepared for this new chapter. Every parent wants to offer sound guidance and financial literacy tips, but knowing where to start can be tricky. Our guide covers a few basics that every parent should discuss with their children.

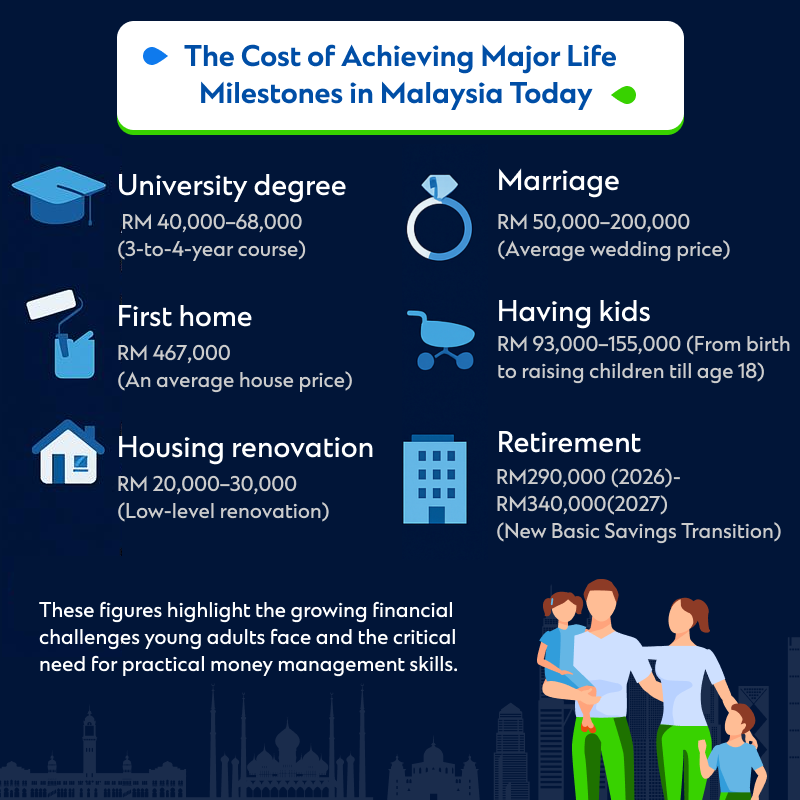

Financial planning for children: Making them aware of inflation

Consider how product prices rise and how everyday expenses have changed over the years. Inflation causes what was once affordable to cost significantly more, especially major life expenses and big-ticket items. Consequently, today’s generation might face greater pressure to save for the future. The following is an estimated overview of costs associated with key life stages in Malaysia today.

When it comes to money management, the most significant advantage is time. It is also a misconception that one should have a large cash surplus to start a financial journey. Uncertainty about where and how to begin is one of the most common reasons for inadequate financial planning. Young adults may face similar situations. Hence, parents should equip them with the right knowledge and preparation to secure their financial future.

Importance of money management for young adults

Parents care about their children’s future and ensure that they have the means to fund their future milestones. This is precisely why young working adults should design their own financial blueprint as soon as they begin their financial journey and start receiving regular income. Parents usually play a huge role in inculcating financial literacy in children and encouraging them to take their first step towards financial security.

Empowering children to take care of their finances

Encouraging children to practice proper money management before they enter the workforce is essential. Whether they are still in education or entering the job market, parents can speak to them about saving a portion of their pocket money or internship allowance for their future. Instilling the habit of saving a fixed portion first will better prepare young adults for their significant future financial milestones than relying on residual pocket money or internship allowances.

Creating a budget

Some children save first and spend the rest, while others spend first and save the balance. Parents usually encourage their children to save the remaining allowance for rainy days. Relying on leftover funds may reinforce the perception of spending first. Instead, by helping children prioritise savings first, they develop a stronger, more disciplined approach to managing their finances.

Maintaining an emergency fund

Setting aside 3 to 6 months’ worth of basic living expenses as contingency funds is a good practice to ensure children have enough money to cover unforeseen circumstances. For example, with a deposit account like PrivilegeSaver, one can earn up to 6.15% in interest per annum and enjoy banking convenience with unlimited free instant internet fund transfers.

Obtaining an insurance savings plan

Parents can purchase an insurance savings plan to give their children a head start, which will help them in the long run. Once they turn 21, parents can transfer their rights to them, while children can receive the cash benefit for life. The cash benefit can also kickstart their financial journey towards future needs, such as studies or marriage. For example, insurance savings plans like PRUSignatureBoost can help children reach new heights with savings.

Investing in unit trusts with a regular savings plan

Children can grow their savings more efficiently by investing in unit trusts via an online platform. A unit trust regular savings plan lets them start with a relatively low investment threshold and increase their contributions over time as their careers stabilize. With investment thresholds as low as MYR50 per month, it’s easy for young investors to make their money work for them. RSP offers the benefits of dollar cost averaging, where the average unit cost reduces over time. Therefore, even with price fluctuations, investors do not have to worry about timing risks.

Exploring the equities (stocks) market

For young adults with a longer time horizon and higher risk tolerance, investing in equities and blue-chip companies can strengthen their portfolio. While some companies pay dividends to their stockholders, the dividends can be reinvested to purchase additional stocks. Investing in different industries, countries, and asset classes helps diversify the portfolio. But before investing in stocks, one should know that returns are not guaranteed. Therefore, when the market is down, making rash decisions to sell stocks can result in losing money.

Parents can break the cycle of financial stress by prioritising their own retirement planning, which indirectly protects their children’s financial freedom by avoiding potential dependence. Ultimately, equipping young adults with financial knowledge is a key component of any parent’s journey. Remember that kids need more than just advice, they need parents to model positive financial habits daily.

Looking for reliable retirement planning strategies? Connect with one of our Relationship Managers today.