Table of Contents

In a rush? Read this summary:

- A Regular Savings Plan (RSP) enables investors to contribute fixed amounts at regular intervals, thereby averaging out market volatility.

- Lump sum investments can deliver higher long-term returns in rising markets due to the compounding effect.

- Both strategies can be effective depending on investors’ goals and market conditions; diversification, consistency, and a long-term perspective remain essential for wealth creation.

Regular saving plan (RSP) vs. lump sum investment: Investors with a large amount of excess cash may wonder if it’s better to invest a large sum into the market at once or put a certain amount away over time through a regular saving plan or dollar cost averaging (DCA). During periods of heightened uncertainty, it’s essential to evaluate the risk capacity, timeline and investment strategy before making any decision

Regular saving plan vs lump sum: How do this investment vehicles work?

RSP is an investment strategy through which investors invest a fixed amount of money over a period of time. If the market declines, investors typically buy more shares with their investment amount, thereby benefiting more from the eventual recovery.

RSP is an investment strategy through which investors invest a fixed amount of money over a period of time. If the market declines, investors typically buy more shares with their investment amount, thereby benefiting more from the eventual recovery.

A lump sum investment refers to investing the entire amount in the market immediately, rather than investing it over a period of time. In a rising market, a lump sum works better than DCA at that time because early investment gives compound growth more time to work.

The benefits of DCA

During uncertain economic times, the volatile market can be intimidating for emotional investors, as stock prices tend to fluctuate and fall. This is when investors can achieve more price stability by investing through DCA and spreading their investments over fixed intervals, rather than investing their entire amount at once.

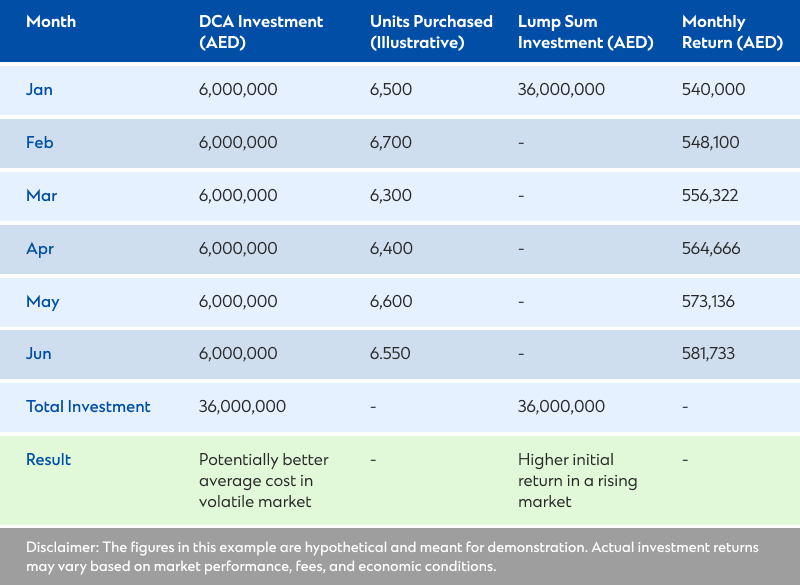

For example, an investor decides to invest AED 36,000,000 over 6 months by investing AED 6,000,000 at the end of every month.

If the market prices fall during this time, the investors will be able to buy more units each month with the same amount. As a result, this may result in a lower average purchase price compared to investing the entire AED 36,000,000 immediately.

The benefits of a lump sum investment

The primary advantage of a lump sum investment is that it allows an investor to benefit from the compounding of interest. For example, if the market delivers an annual return of approximately 18%, it translates to around 1.5% per month. If an investor invests AED 36,000,000 at a time, the return of the first month alone can be as high as 540,000 (1.5% OF AED 36,000,000).

On the other hand, if the same investor uses DCA and invests 6,000,000 at the end of January, the investment might grow by 90,000 by the end of February, assuming a consistent 1.5% monthly return.

That is why, while DCA can outperform a lumpsum investment given the market is volatile and declining, a lump sum tends to outperform DCA in consistently upward-trending markets.

The benefits of a lump sum investment

Regular savings vs. lump sum returns: Investors who are still undecided about these two investment vehicles can keep in mind that, regardless of the strategy they follow, diversification remains one of the most reliable ways to reduce overall risk. One can diversify investments by industry (such as finance, technology, or manufacturing), geography (including both developed and emerging markets), and market capitalisation (including small cap stocks , medium, and large-cap stocks).

Once an investor diversifies a set of assets, it reduces the overall risks in a portfolio, as a loss in one area can be balanced by a gain in another.

Regular savings versus long-term returns: Long-term wealth building

When it comes to building long-term wealth, the strategy that really matters is getting started and staying consistent. The real difference comes when one gets the money to work in the market instead of letting it sit idle.

Whether one invests gradually after a fixed period or all at once, the key principles of wealth building stay the same.

- Start as early as possible to get the compounding benefits.

- Try to keep investment fees low to preserve more of the returns.

- Emotional investors should avoid panic selling and stay invested through market ups and downs.

- Instead of chasing winners, sometimes investors try to focus on broad market index funds.

Over time, steady growth helps investors focus on earning more. Ultimately, wealth is built by taking action, investing money in productive endeavours, and adhering to a well-defined strategy.

Speak to your Standard Chartered relationship manager or contact us to learn more about investing in Regular Savings Plans (RSPs).