Reasons to be bullish on gold

The precious metal has suffered a sell-off during the Middle East war but the outlook is more positive.

This article was originally published on FT.com.

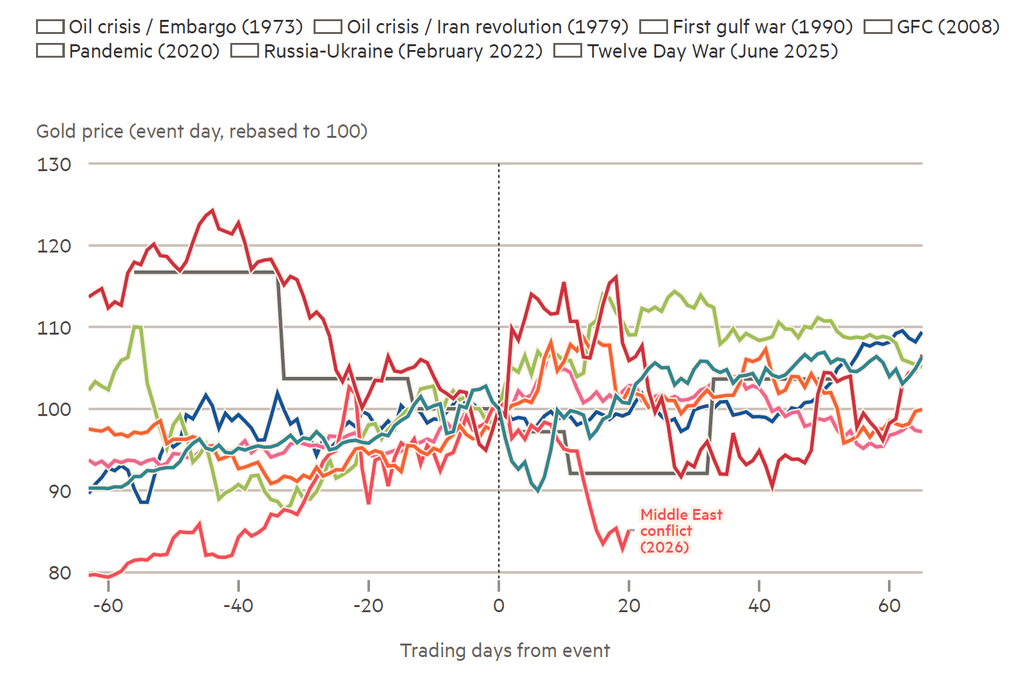

Gold’s haven status is being questioned — again. Prices have fallen sharply since the start of the Middle East conflict, dropping about 12 per cent.

This has contradicted the view of gold as a haven asset that provides stability (or appreciates) at times of market distress, heightened uncertainty or geopolitical tensions. However, I believe gold’s status remains intact even as it switches roles in the short term and expect prices to test.

Gold can play both the headliner and a supporting role in markets. However, this does not mean gold has lost its traditional role.

In periods of distress, investors rotate between assets and stock market losses trigger calls for more margin collateral on trades. Gold is one of very few assets that can be called upon to provide liquidity without incurring losses.

Historically, such liquidity needs have tended to weigh on gold for four to six weeks after a crisis event; once those needs become less acute, investors rebuild gold exposure. This process can take longer in the event of a prolonged crisis — during the global financial crisis, for example, it took gold more than four months to retrace losses.

While gold has fallen more sharply this time than during past geopolitical shocks, particularly conflicts in the Middle East, there are reasons for this divergence.

Gold prices scaled record highs in January, taking the exchange-traded products that track them to new peaks as investor demand surged. This made gold a prime candidate for selling. The differential of spot prices over the 50-day moving average surged in January to levels last seen in 1999. Now, the reverse is true — spot prices have fallen below the 50-day moving average, and the gap is the largest since 2013. Gold went from overbought territory in January to oversold since the start of the conflict.

Gold price response to oil spikes and market shocks

So, what is the gold price telling us? First, markets remain uncertain on the duration of the conflict, driving a continued need for liquidity. Evidence of this is shown in how the implied volatility in gold markets has jumped to levels last seen during the pandemic.

Gold also appears to have now reverted to taking its short-term cues from US rate expectations and uncertainty around the policy response to the current crisis.

Exchange Traded Products (ETPs) and central bank flows are the two factors to watch. ETP investors tend to track real yield expectations more closely than structural drivers. Net ETP redemptions in March are on track for the steepest decline since September 2022, suggesting a near-term shift away from structural or safe-haven drivers of gold appetite. That said, ETP liquidation has started to slow, implying that frothy positioning could be largely flushed out.

On central banks, markets are watching for signs of potential selling of reserves built up in recent years. Their net buying slowed in volume terms last year to 863 tonnes from more than 1,000 tonnes but continued to scale record highs in dollar value.

But there are a host of reasons that support the argument that gold prices should be higher. Gold is not currently pricing in recession risks. It tends to rise 15 per cent on average during recessions, whereas industrially biased commodities tend to be weighed down by negative output growth.

And the precious metal is not pricing in stagflation fears. Even if the conflict is resolved tomorrow, oil prices are likely to remain higher for longer, raising fears of an increase in inflation. As a store of value, gold prices tend to rally in an environment of rising inflation, particularly if it is unexpected and prolonged.

Many of gold’s structural drivers also remain intact, including concerns about elevated US and global debt, fiat currency debasement, tariff and trade uncertainty, and geopolitical risks.

Gold is pricing in many fears all at once, so its path is unlikely to be linear in the near term. And the current liquidity needs could weigh on gold for a little longer. But we still expect prices to resume their upward trajectory in the coming months. On the downside, the 200-day moving average for gold prices has not been breached since October 2023, suggesting a price floor. The compass for the gold market still points north.

Related insights

Testing times: Commodity markets reprice as conflict blockad…

Find out how the strait blockage supply shock is impacting commodities trade and prices.