Patent cliffs to policy shifts: Big Pharma’s key priorities

It is critical for CFOs and Treasurers to understand what drives value in the sector, to ensure the ‘right’ capital allocation framework is in place.

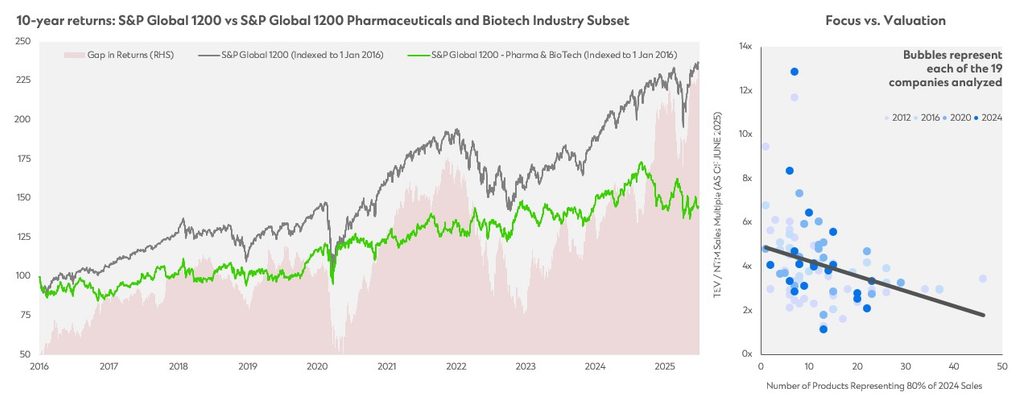

The pharmaceutical industry is entering a pivotal phase. Geopolitical and regulatory pressures are rising, a USD 350 billion patent cliff is fast approaching, and pricing scrutiny is increasing under US Medicare reforms tied to the Inflation Reduction Act. These are all contributing to the sector’s underperformance relative to the broader market.

A large-scale, broad investment strategy is also not translating into better performance. Our analysis shows that companies with a more focused product base tend to trade at stronger valuations. Fewer than ten core products seem to be the optimal range.

Shifting capital allocation priorities

R&D and Capex continue to rise, but M&A activity is more selective – perhaps driven by the ‘focus vs valuation’ conundrum. So far this year, jumbo deals have been rare. Most activity is focused on early to mid-stage assets in the USD 1 – 10bn range, with structures that rely more on milestones and earnouts rather than heavy upfront payments. China has also overtaken the EU as the second-largest innovation hub globally, trailing only the US in novel drug development.

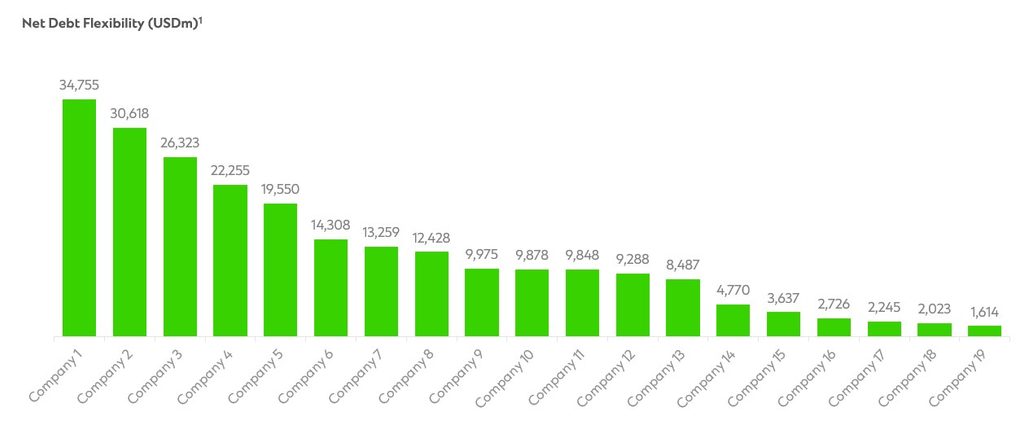

The good news is that companies have room to manoeuvre. The sector’s combined net debt capacity stands at approximately USD 240 billion, based on current ratings, giving flexibility to act quickly when needed.

Whether it is cross-border M&A, portfolio transformation, or buying back undervalued shares, capital allocation will remain a critical lever for value creation in a period that continues to be defined by uncertainty.

To read more about these themes, as well as what they mean for capital structure strategy for corporates in these sectors, contact us here.

Explore more insights

Indonesia’s healthcare moment is now

With rising demand, bold reforms and a digital backbone now in place, Indonesia is opening its doors to long-ter…