What is Electronic Deferred Payment?

Electronic Deferred Payment (EDP/EDP+) is a new solution that supports the transition to e-payments, complementing existing solutions such as PayNow, FAST, GIRO and MEPS+.

EDP is the digital alternative to a post-dated cheque while EDP+ is the digital alternative to cashier’s order.

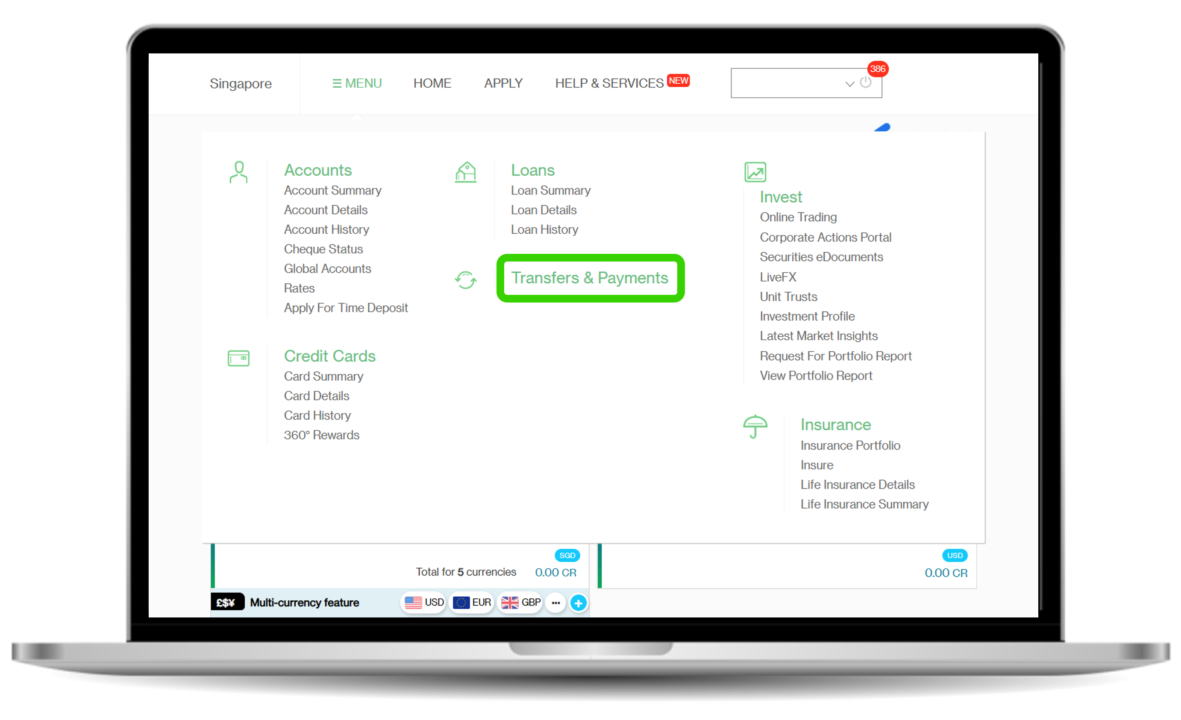

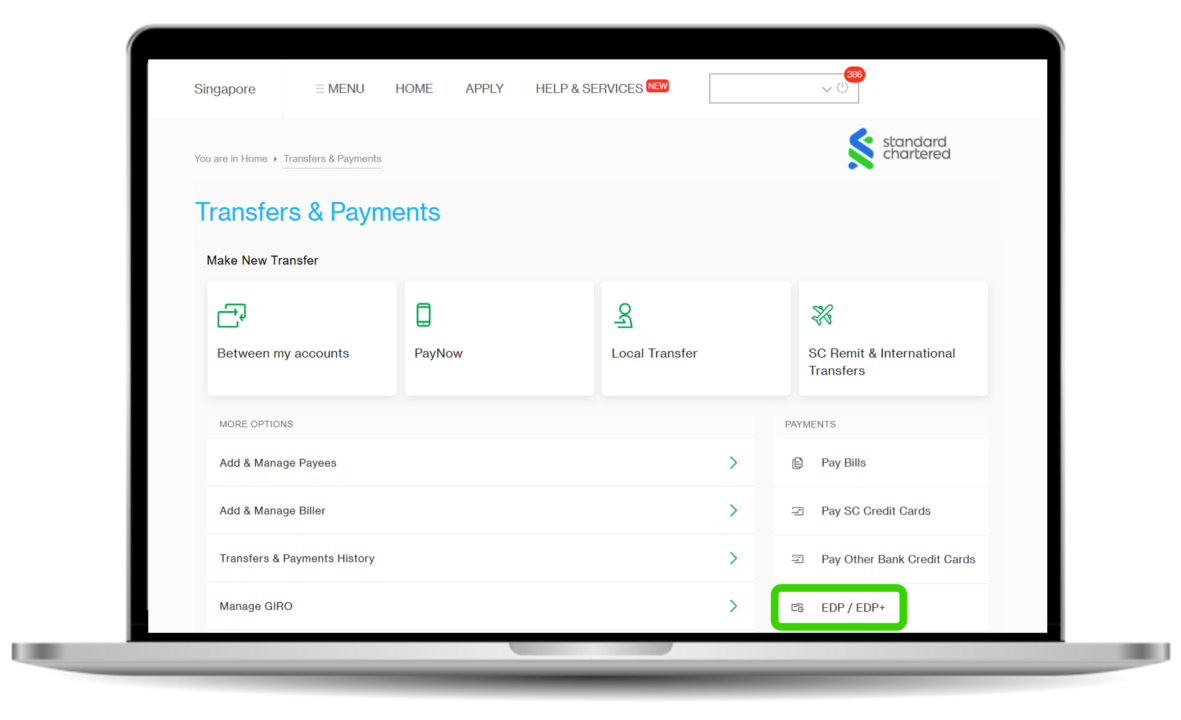

How to access EDP

How to access EDP

FAQ – EDP and EDP+

As set out in the consultation paper published in November 2022, MAS is facilitating Singapore’s transition into an innovative e-payments society.

EDP and EDP+ are two new e-payment solutions introduced in July 2025 that complement existing solutions such as PayNow, FAST, GIRO and MEPS+. Specifically, EDP and EDP+ can be used to make deferred payments in place of cheques.

The key difference between these solutions lies in when funds are deducted from the payer’s account:

- EDP: Funds are deducted from the payer’s account only when payee requests payment, i.e. upon presentment of the EDP.

- EDP+: Funds are deducted immediately from the payer’s account upon issuance of the EDP+, ensuring the amount cannot be used for other transactions. This reduces the risk of non-payment due to insufficient funds in the payers’ account, providing greater assurance to payees as compared to EDP.

Individuals and companies can use EDP and/or EDP+ via the digital banking platforms of participating banks available here.

Standard Chartered Bank does not offer EDP+ issuance however, you will be able to receive EDP+ from other participating banks.

If you hold a joint account where transactions must be authorised by more than 1 account holder, such accounts will not be eligible for EDP.

For payers, EDP and EDP+ can be used to make deferred payments and indicate an intent to pay without the need for a physical cheque.

While FAST and PayNow remain suitable for instant and same-day transactions, EDP and EDP+ are designed for scenarios that require deferred payments or refundable deposits.

- Status Updates: Both payer and payee receive real-time updates on status changes

- Full Traceability: Clear visibility of when and why a payment was made, from whom and to whom

- Ease of Reconciliation: Simplified reconciliation process for accurate record-keeping

- Reduced Administrative costs: Minimised manual paperwork, tracking and associated costs

- Sustainability: Eliminates the need for paper cheques

You will not be charged any fees to use EDP with Standard Chartered Bank.

You do not need to sign up for EDP if you have enabled digital banking access via Online Banking or SC Mobile.

Step 1: Log in to Online Banking or SC Mobile to initiate EDP creation:

- Input payee identifier – mobile number / bank account number / NRIC / UEN

- Input transfer details – amount, effective date of payment*

*The effective date of payment is the earliest date on which a payee can initiate presentment of the EDP. The effective date must be at least one day after the creation date, but no more than six months from it.

Step 2: Receive email and push notification on:

- Successful/unsuccessful issuance of the EDP

- Successful/unsuccessful presentment of the EDP by payee

- Successful/unsuccessful cancellation of the EDP

Step 1: You will receive an email and push notification on:

- An EDP/EDP+ received

Step 2: Log in to Online Banking or SC Mobile to initiate presentment of the EDP/EDP+ received

Step 3: Receive email and push notification on:

- Successful/unsuccessful presentment of the EDP/EDP+

- Successful/unsuccessful cancellation of the EDP/EDP+

An EDP/EDP+ expires six months from its effective date of payment.

- EDP: Upon expiry, the payee must contact the payer to request re-issuance. The payer’s account is not impacted.

- EDP+: Funds from the payer’s account is deducted upfront. Upon expiry, the funds from EDP+ will be refunded to the payer’s account and the payer must contact the payer to initiate re-issuance of the EDP+ if needed.

Your EDP transaction limit is aligned with your Daily Transaction Limit settings. You can manage your EDP transaction limit by adjusting your Daily Transaction Limit. The maximum transaction limit for EDP issuance is capped at S$200,000 per day.

EDP and EDP+ is only available for payments in SGD.

At the outset, EDP and EDP+ is only available for domestic payments in SGD. For payments in USD, USD cheques remain available for both individuals and companies.

FAQ – For Retail Cheque Users

Yes, retail users will still be able to issue and deposit SGD cheques after 2026. This includes the issuance of retail cheques for payment into corporate accounts.

Retail customers in receipt of cheques issued by a corporate should present their cheques for clearing well before 31 December 2026, to ensure that their cheques can be processed before the deadline.

Cashier’s orders remain available for corporates and retail users.

USD cheques remain available for corporates and retail users.

Retail cheques, cashier’s orders and USD cheques will continue to be available to serve users that require more time to transition to alternative payment methods. MAS, ABS and the industry will continue to monitor cheque usage and provide updates on any changes to the timeline or availability of these payment methods following future reviews. In the meantime, retail users are encouraged to explore and adopt digital alternatives where possible.

Currently, cheque issuance fees are being waived for customers aged 60 years old and above until 31 December 2025. To ensure that the banking needs of seniors are well met going forward, customers who are aged 60 years old and above as of 31 December 2025 will remain eligible for the waiver of cheque services fees after 31 December 2025.

FAQ – For Corporate Cheque Users

As set out in the consultation paper published in November 2022, MAS is facilitating Singapore’s transition into an innovative e-payments society. Phasing out corporate cheques could accelerate businesses’ transition to more efficient e-payment methods and provide gains to the economy.

Cheque usage has steadily declined as businesses and individuals increasingly adopt faster, more efficient digital payment methods. As a result, cheque clearing and processing costs have risen, making cheque-based transactions costly for financial institutions to maintain.

- From 1 January 2026: All banks will stop issuing new SGD corporate cheque books, bulk cheque services and cheque self-printing services

- From 1 January 2027: All banks will stop processing SGD corporate cheques

Banks will not process any corporate cheques from 1 January 2027. Corporate cheque payees must deposit all corporate cheques by 31 December 2026 to avoid having such cheques rejected.

Should corporate cheque payees miss the deadline to deposit their cheques or have their cheques rejected, they will need to make alternative payment arrangements with the cheque payer.

Individuals and companies have access to a broad range of e-payment alternatives, including GIRO, FAST, PayNow and MEPS+.

Cashier’s orders will still be available for corporates and retail users.

USD cheques will still be available for corporates and retail users.