Recovering from COVID-19 – Three focus areas for mid-corporates to improve liquidity

COVID-19 caught many businesses by surprise, with many facing government-imposed operational restrictions, severe supply chain disruptions and declining consumer demand. The most serious impact, experienced by most if not all businesses, was on their finances, especially working capital.

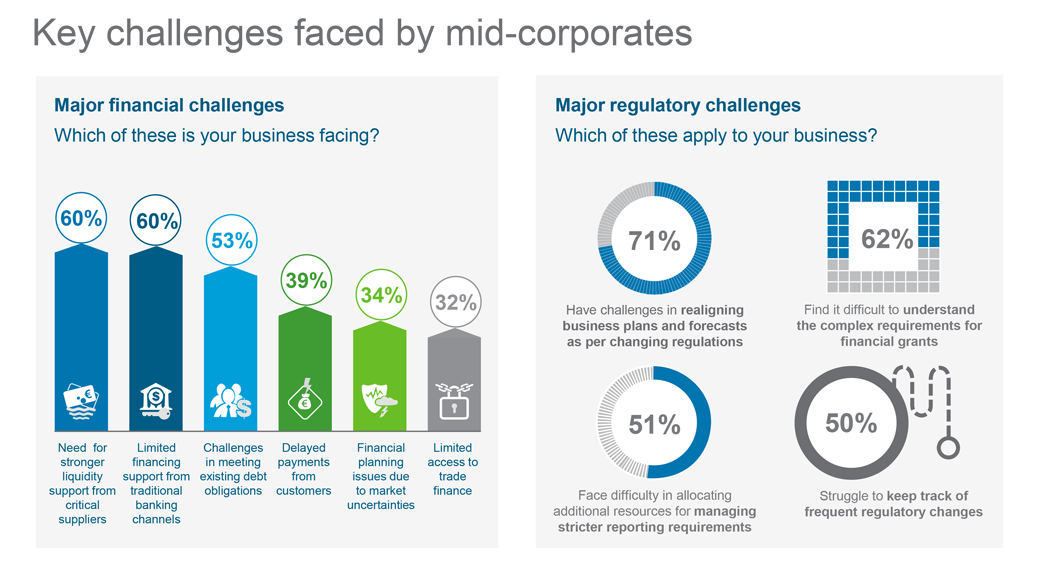

In our survey1 of 205 mid-corporates, 60 per cent of C-level executives said they face challenges in receiving financing support from traditional channels, and want stronger liquidity support from critical suppliers, while 39 per cent of them are facing delayed payments from customers. Given these scenarios, companies will need an effective finance strategy focused on preserving liquidity through immediate cash conservation measures to weather the effects of this ongoing crisis.

As economies re-open, companies are finding themselves in the ‘Preservation and Stability’ phase, i.e. Stage 2 of the ‘The Mid-Corporate Journey to Resilient Growth’. They are actively exploring ways to maximise revenues and re-evaluating their cost structures with an immediate need to optimise working capital.

Besides the upheaval to their finances, mid-corporates also cited keeping up with regulatory developments as something they find challenging even as they grapple with revising business plans and forecasts in the face of fast-changing circumstances. Complying with stricter reporting and the myriad complex requirements in order to qualify for financial grants have added to their concerns.

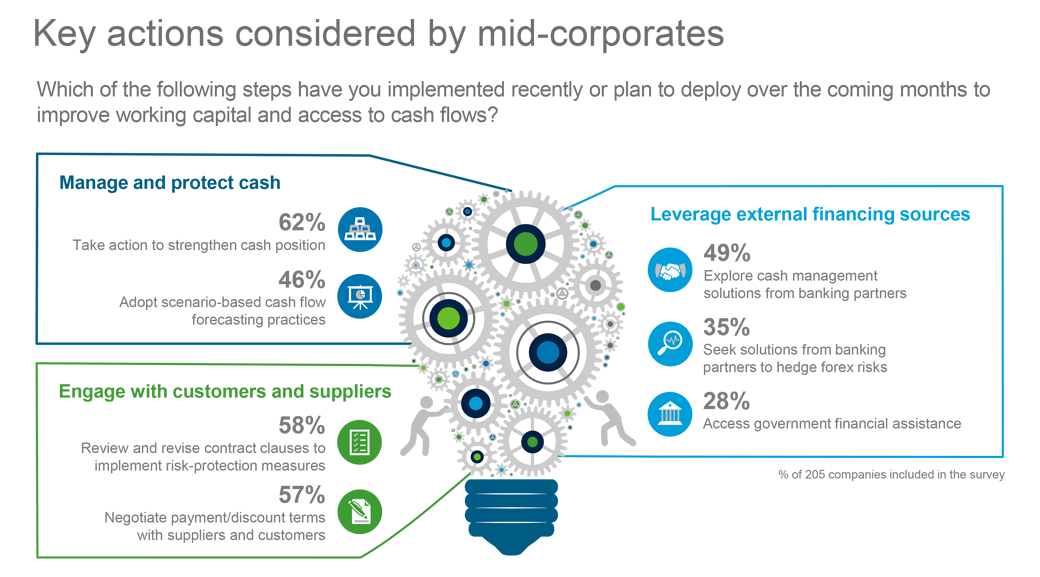

While these challenges are not uncommon, the scale of impact is significant in a crisis of this nature. To overcome them, mid-corporates need to build a comprehensive and well-defined plan followed by swift execution.

Read about Standard Chartered’s collaboration with SAP Ariba to help companies seamlessly manage their supply chain finance needs with the digital platform here.

Mid-corporates should also consider more active engagement with industry lobby groups to campaign for sector-specific policies around financial and other support to businesses during the COVID-19 crisis.

As companies progress along ‘The Road to Resilient Growth’ and enter Stage 3 (‘Preparing for Growth’), they should consider actions that will improve their cash position in the longer-term, such as realigning corporate real estate and manufacturing locations to map against revised operational capacity and leveraging digital technologies for cost-efficiencies (e.g. blockchain for trade finance).

The next point-of-view in our series will focus on alternative sources of capital and investments that mid-corporates can potentially tap into to further strengthen their capital base and enable this new phase in their journey towards resilient growth.

Watch now

[iframe title=”Video” width=”800″ height=”450″ scrolling=”no” marginheight=”0″ marginwidth=”0″ src=”https://www.youtube.com/embed/https://www.youtube.com/watch?v=rGOB9i5R-_0?showinfo=0&rel=0″]

PwC, ‘COVID-19: Finance and liquidity – Managing cash pressures due to coronavirus disruptions’

PwC, ‘Measures to mitigate the impact of coronavirus – Optimisation of working capital’

Standard Chartered, ‘We’ve joined forces with SAP Ariba to bring financial supply chain solutions to the world’s largest digital business network’, August 2019

Standard Chartered, ‘We’ve completed our first joint transaction on blockchain platform with Linklogis’, August 2109

Treasury & Risk, ‘Strengthen Your Cash Position in the Covid-19 Crisis’, May 2020

Oberlo, ‘5 Steps Business Owners Can Take Now to Improve Cash Flow During COVID’, May 2020

EuroFinance, ‘Managing treasury through the Covid-19 crisis’, April 2020

The Asset, ‘Covid-19, trade war uncertainties spark supply chain innovation’, March 2020

1 Survey commissioned by Standard Chartered in June 2020 and completed by 205 mid-corporates (annual revenue USD100m-500m) based in Mainland China, Hong Kong, Singapore, Malaysia and India

This material has been prepared by PricewaterhouseCoopers Consulting (Singapore) Pte Ltd. (“PwC”) at the request of Standard Chartered PLC and its affiliates (“SC Group”) in accordance with the agreement between PwC and SC Group. Other than to SC Group, PwC will not assume any duty of care to any third party for any consequence of acting or refraining to act, in reliance on the information contained in this report or for any decision based on it. PwC accepts no responsibility or liability for any use of this report by any third party, including any partial reproduction or extraction of this content.

It is not independent research material. This material has been produced for information and discussion purposes only and does not constitute advice or an invitation or recommendation to enter into any transaction or to subscribe for or purchase any products or services and should therefore not be relied upon as such. It is not directed at Retail Clients in the European Economic Area as defined by Directive 2004/39/EC, neither has it been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The information herein may not be applicable or suitable to the specific investment objectives, financial situation or particular needs of recipients and should not be used in substitution for the exercise of independent judgment.

Some of the information appearing herein may have been obtained from public sources and while PwC and SC Group believe such information to be reliable, it has not been independently verified by PwC or SC Group. Information contained herein is subject to change without notice. Neither PwC nor SC Group is under any obligation to update or revise the information contained herein. Any opinions or views of PwC or SC Group or any other third parties expressed in this material are those of the parties identified. PwC and SC Group do not provide financial, accounting, legal, regulatory or tax advice. This material does not provide any investment or tax advice. Please note that (i) any discussion of U.S. tax matters contained in this material (including any attachments) cannot be used by you for the purpose of avoiding tax penalties; (ii) this communication was written to support the promotion or marketing of the matters addressed herein; and (iii) you should seek advice based on your particular circumstances from an independent tax advisor.

While all reasonable care has been taken in preparing this material, PwC, SC Group and each of their affiliates make no representation or warranty as to its accuracy or completeness, and no responsibility or liability is accepted for any errors of fact, omission or for any opinion expressed herein. You are advised to exercise your own independent judgment (with the advice of your professional advisers as necessary) with respect to the risks and consequences of any matter contained herein. PwC, SC Group and each of their affiliates expressly disclaim any liability and responsibility for any damage or losses (including, without limitation, any indirect or consequential losses or damages) you may suffer from your use of or reliance on this material or as a result of any information being incorrect or omitted from this material.

Any financial projections or models included in this material are based on numerous assumptions regarding the present and future business strategy of the entities to which such projections or models relate and the environment in which such entities may operate in the future. These future events are not a guarantee of future performance and are subject to certain risks, uncertainties and assumptions.

SC Group or its affiliates may not have the necessary licenses to provide services or offer products in all countries or such provision of services or offering of products may be subject to the regulatory requirements of each jurisdiction. This material is not for distribution to any person to which, or any jurisdiction in which, its distribution would be prohibited.

The SC Group may be involved in transactions and services with clients or other persons who are, or may be, involved in the transactions that are referred to in this material or who may have conflicting interests with you or any other person. The SC Group’s ability to enter into any transaction (or to provide any person with any services) will be subject to, among other things, internal approvals and conflicts clearance.

The distribution of this material in certain jurisdictions may be restricted by law and therefore persons who receive this document or any Information should inform themselves about, and observe, any such restrictions. Any failure to comply with these restrictions may constitute a violation of the laws of any such jurisdiction. No liability to any person is accepted by SC Group or PwC in relation to the distribution of this document or the Information in such jurisdictions.

The distribution of this material in any other country locations may require suitable disclosures to be made by the SC Group. Should you receive this material in such other country location, please contact the relevant SC Group member.

Copyright in this document and all materials, text, articles and information contained herein is the property of SC Group or its licensors (save for any copyright in materials created by any identified third parties which remain vested with the respective third party), and may not be copied, distributed, adapted, translated or otherwise used (in whole or in part) without the prior written consent of SC Group.

Copyright © 2020. SC Group. All rights reserved.