Multilateral development banks: A clear path to closing the world’s infrastructure gap

Authors:

There is an urgent need for multilateral development banks (MDBs) to collaborate with the private sector if we are to achieve the UN’s Sustainable Development Goals and realise a net zero emissions future. Our recent collaboration with the World Bank in Angola underscores the potential.

Nearly half of Angolan households lack access to clean water.1 Men, women, and children across the country face preventable health risks including exposure to communicable diseases. In 2021, we partnered with the World Bank to finance the USD1.1 billion Luanda Bita Water Supply Project, improving access to potable water for more than two million people.

African infrastructure projects in particular are chronically underfunded. What made this deal work was a partial guarantee from the World Bank on the loan facility. That enabled us to work with the Africa Trade Insurance Agency (ATI), which provided a second loss insurance above the World Bank’s guarantee. The two guarantees provided substantial risk mitigation which – coming at the height of the global pandemic and amid significant risk aversion – enabled bankability and encouraged private sector participation.

Luanda Bita underscores the power of collaboration and the potential to significantly ramp-up so-called ‘crowding-in’ of private capital into these kinds of socially and economically important projects. It shows that by working together, MDBs and the private sector can address today’s most pressing infrastructure challenges, meeting critical needs for current and future generations.

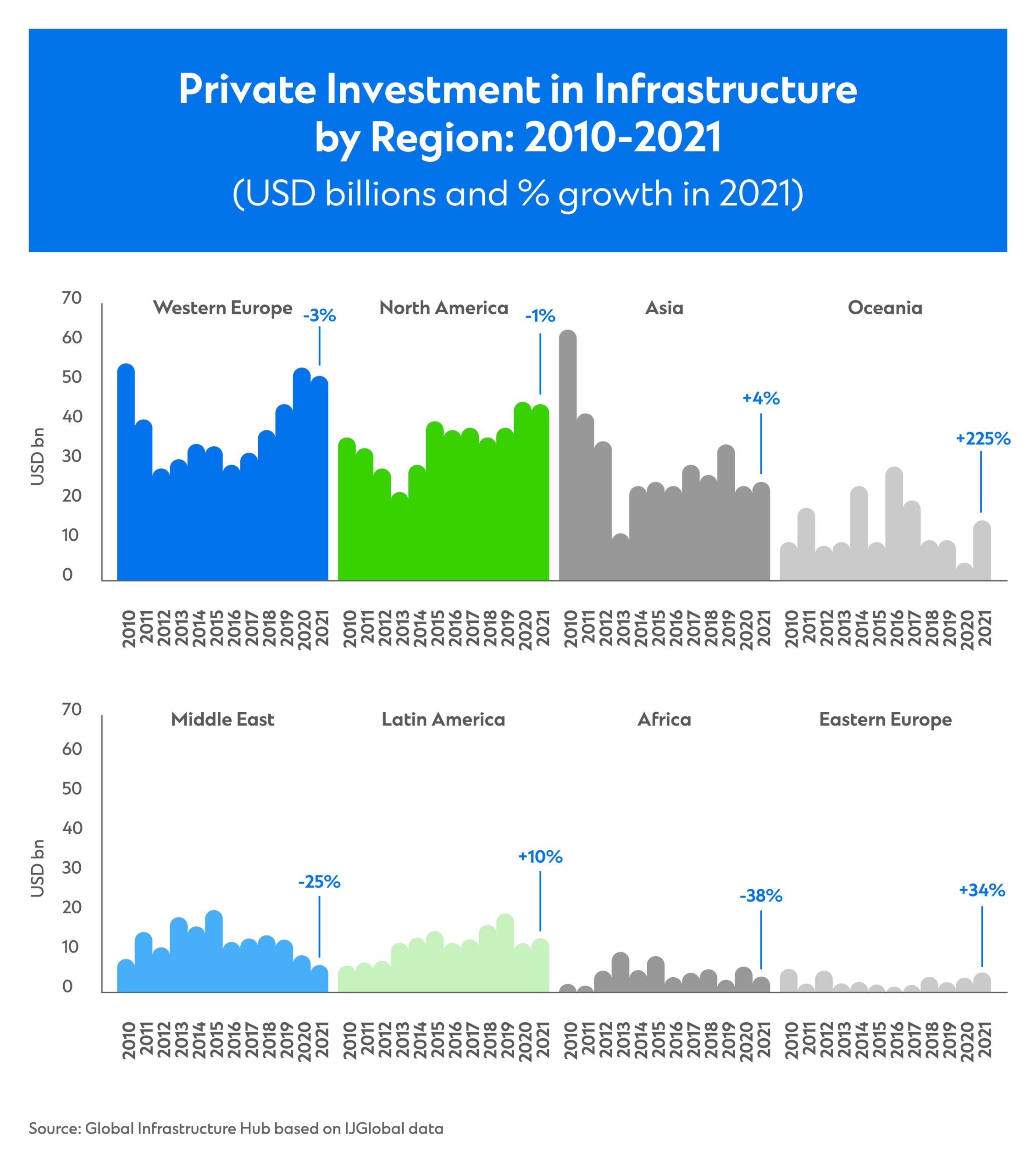

The world faces an estimated USD15 trillion infrastructure financing gap through 2040.2 To provide basic infrastructure for everyone, we must spend nearly USD1 trillion per year. Yet, private investment stood at just USD172 billion in 2021 – a far cry from what is needed.3

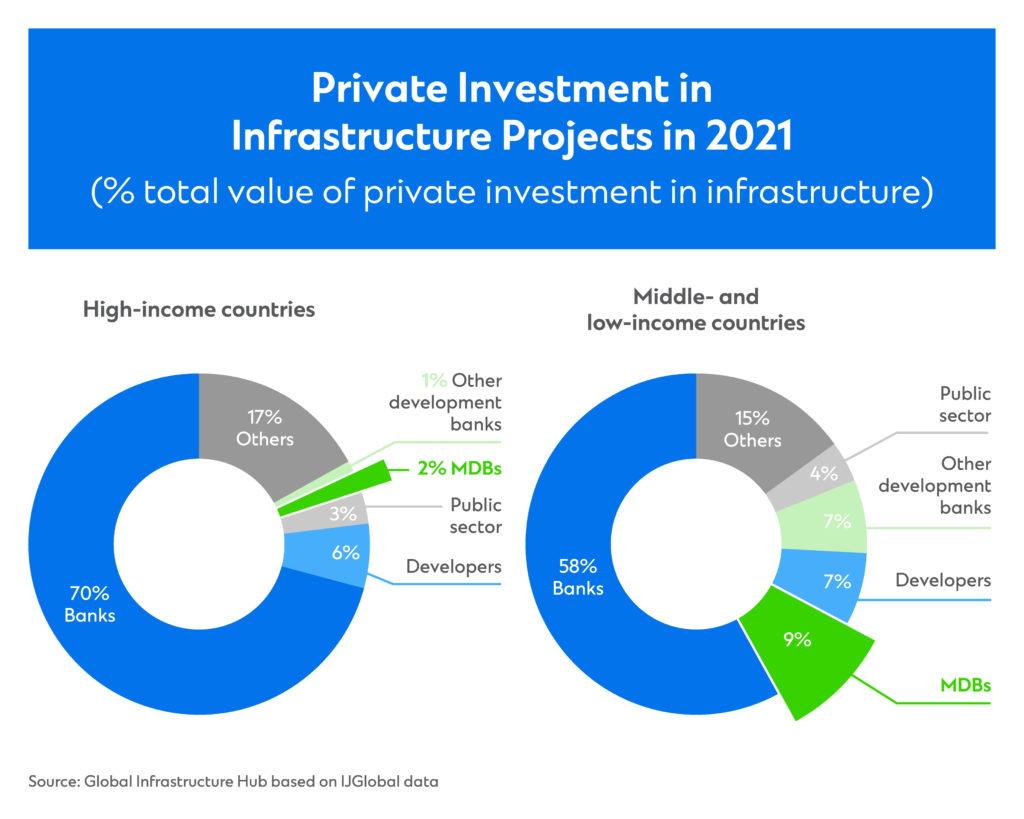

Unfortunately, the gap between private investment in infrastructure projects in high-income countries and that in middle- and low-income countries is actually widening. In 2021, only 20 per cent of private investment in infrastructure projects occurred in middle- and low‑income countries.4 Heightened political risk and a lack of adequate mechanisms to mitigate financial risk create significant barriers.

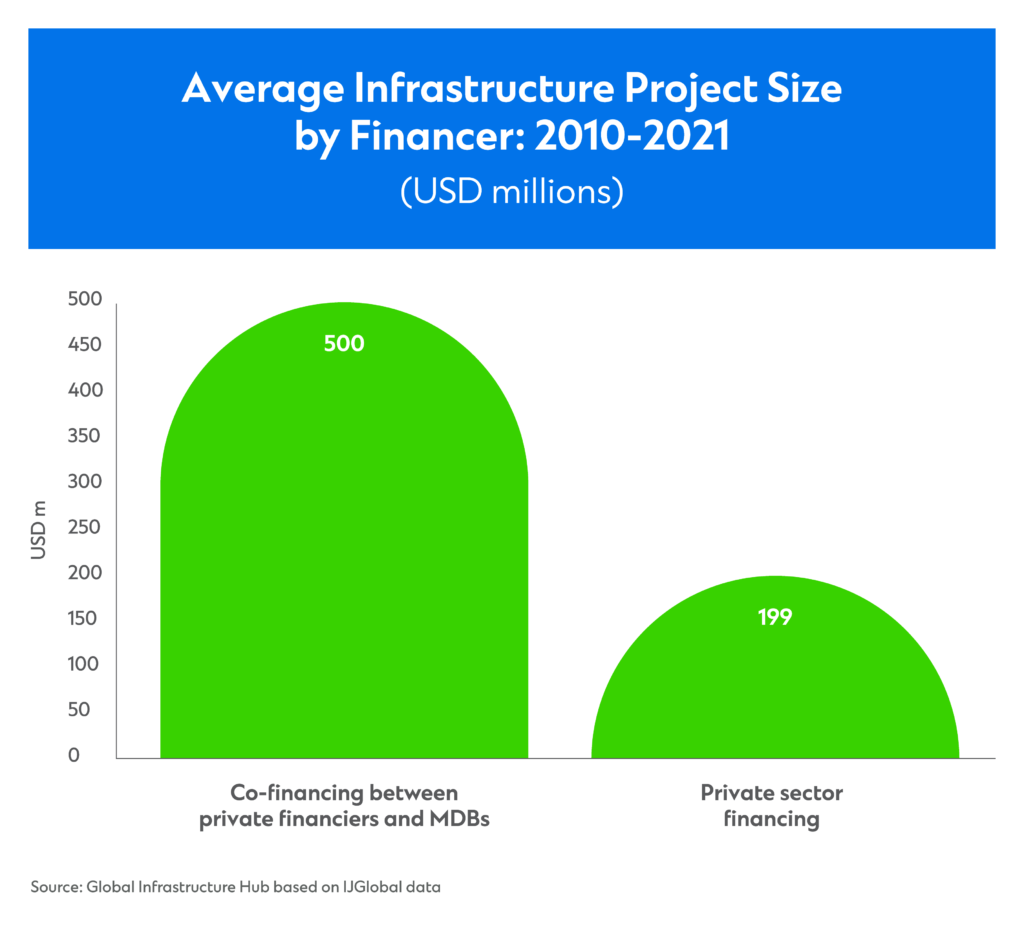

MDBs can lower those barriers. Their participation in a project signals its viability, stability, and creditworthiness, which helps reduce risk and attract more private capital. MDB participation also enables cheaper and longer-term financing, which is critical for emerging markets – in particular low-income countries that are in most need of infrastructure investment. Data from the Global Infrastructure Hub show that 27 per cent of private investment in infrastructure in middle- and low-income countries involved an MDB as a co-financier in 2021. Those transactions were larger than transactions financed by the private sector alone because MDB participation can reduce risks associated with larger projects.

MDBs can also play an important role as market maker, deploying their products in a manner that will accelerate private sector participation. New products like infrastructure asset-backed securities (IABS) are a perfect example.

Bayfront Infrastructure Management, for instance, provides exposure to a diversified portfolio of project and infrastructure loans across multiple geographies and sectors through the issuance of IABS. This allows institutional investors to access project and infrastructure loans in Asia Pacific and the Middle East in a credit-enhanced structure. MDBs could be actively involved to help support similar structures and broaden the investor base for the right infrastructure projects.

In a world where many low-income countries are grappling with sovereign debt distress, MDBs have significant if often under-appreciated influence. In Angola, the World Bank’s partial guarantee was enough to bring ATI into play to provide second loss insurance. There are so many options available. By embracing them, MDBs can help bring the broad and deep universe of institutional investors to the table, greatly expanding on the current loan market investor base that has traditionally dominated these projects through risk mitigation.

Guarantees will help crowd-in private investors. Even partial guarantees from AAA-rated institutions makes a difference. For every USD1 of guarantee that MDBs can provide, we can bring USD2 of financing. The multiplier effect is incredible. We miss that opportunity when an MDB provides a direct loan instead of issuing guarantees to the private sector. Guarantees can enhance capital allocation.

MDBs are not regulated by traditional regulators. In a way, ratings agencies serve as their regulators by imposing the requirements for a AAA credit rating. Yet the rating agencies all have different methodologies, which means MDBs are left to solve for the lowest and most conservative common denominator. The upshot: MDBs are unable to fully deploy the power of their balance sheets and large capital base – despite a growing awareness that the risk of sovereign default may have been historically overstated.

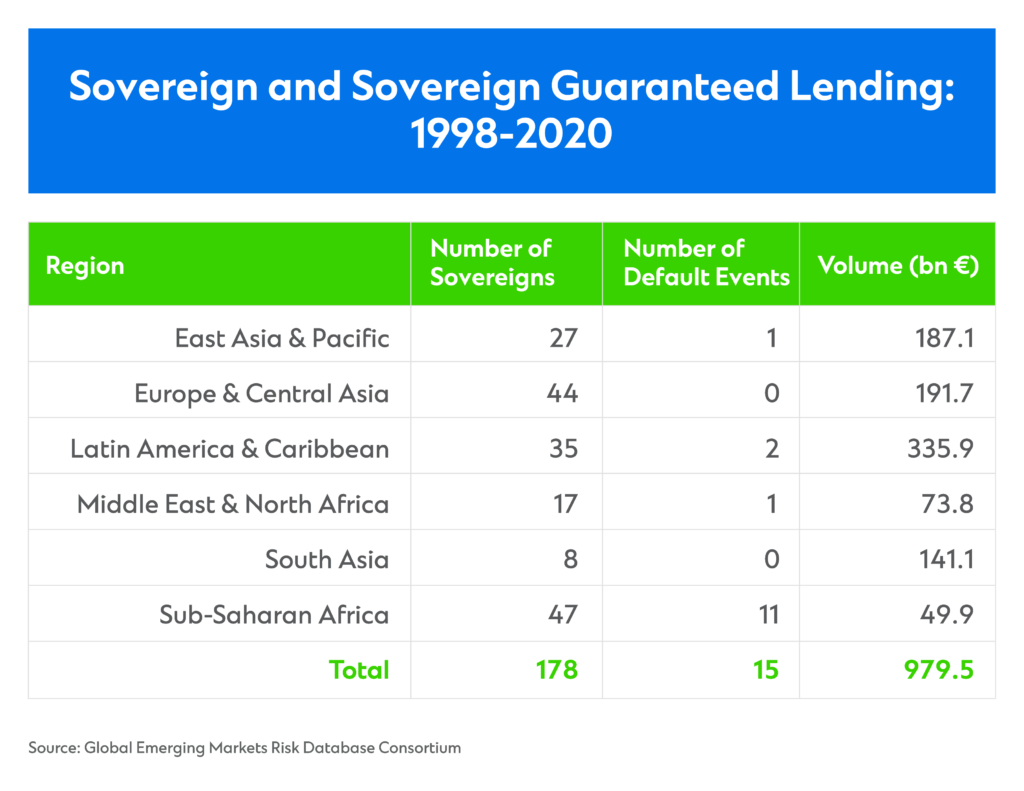

This misapprehension of risk often stems from the lack of objective, verifiable track records. Data from the Global Emerging Markets Risk Database Consortium (GEMs) could help change that. GEMs is one of the world’s largest credit risk databases for MDBs’ emerging markets operations.5 It pools data on credit defaults on the loans extended by consortium members, the migrations of their clients’ credit rating and the recoveries on defaulted projects.

Using this data could change the conversation with ratings agencies. Data showing a lower probability of default can lead to a direct adjustment in the amount of capital that MDBs are able to lend. In turn, this would allow MDBs to fully deploy the firepower of the large capital base and make bigger strides towards closing the infrastructure gap.

MDBs also have a great opportunity to enhance balance sheet management through the use of exposure swaps. Risk-transfer mechanisms with other MDBs can help reduce portfolio concentration by swapping assets to include countries where credit exposure is lower or non-existent. This could potentially further support their credit ratings and free up more capital for investment.

The Asian Development Bank (ADB) blueprinted this in a policy framework in 2020.6 Last year, the ADB signed a USD1.5 billion exposure exchange agreement with the Inter-American Development Bank (IADB),7 which unlike the ADB focuses its development efforts in Latin America. In turn, the IADB will be guaranteeing a certain percentage of the ADB’s country exposure to a group of countries and vice versa. As IADB’s CFO, Gustavo De Rosa, said of an earlier pilot exchange, it’s a pro-rata of an entire exposure to a country.8

MDBs may also want to consider the kind of “blue sky opportunities” that could be true game-changers. Consider for instance if all the AAA and highly rated MDBs were to aggregate all their paid-in and callable capital globally. They would arrive at something like USD1.5 trillion. That’s a super institution with a super-sized capital base that, in theory, could issue super-sized financing solutions. Of course, reality is much more complicated; for most MDBs, shareholders haven’t actually approved callable capital contributions. But just imagine what MDBs could do if they were able to navigate the politics to make this possible.

Much of what we suggested will take time, sustained effort and real collaboration. It won’t be easy. But in a world that is facing both unprecedented risks and unparalleled development needs, it must be done.

Produced by Bloomberg Media Studios in partnership with Standard Chartered.

With topics around urban transformation, energy transition, the future of transport and critical infrastructure across Asia, Africa and the Middle East, this content series will unearth fresh trends and showcase how we are supporting clients in the transition towards a more sustainable and inclusive future.