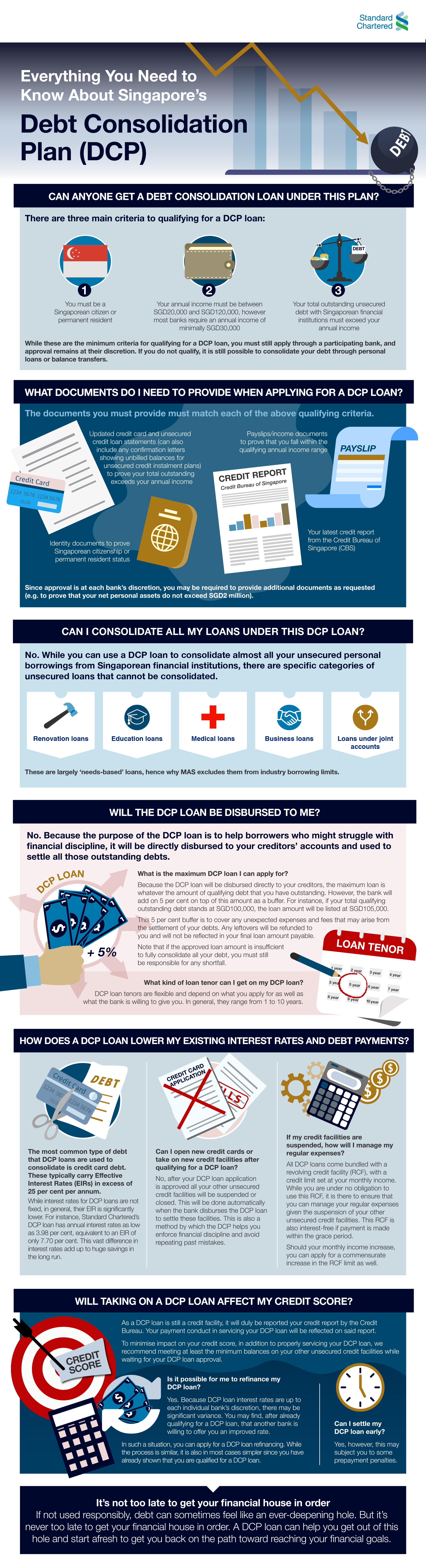

Debt consolidation is the process of taking all your unsecured debt, meaning debt that you have not pledged collateral against, such as credit cards and personal loans, and putting them all in a single bucket. The most common way this is done is by taking out a single loan and using it to pay off all your outstanding debt.

Now, instead of paying varying amounts to different institutions each month, you just lump it all into a single monthly payment. There are three main benefits to doing this.

● Easier tracking and planning: When you have so many disparate payments to make each month, it can be hard to keep track of them all. Consolidating your debt into one single payment means you know exactly how much you must pay each month.

● Potentially lower interest rates: You can often get debt consolidation loans at a lower interest rate compared to your outstanding debts, especially if it comprises mostly credit card debts. This means that you usually end up paying a lesser amount overall.

● Enforced financial discipline: If you are considering a debt consolidation loan, then you already know that you need to improve your financial discipline and spending habits. By consolidating all your debts into an easily trackable single monthly payment, financial discipline is easier to uphold. This is further strengthened by the conditions stipulated by Singapore’s DCP – which we will be elaborating on.

As a financial institution, we have a responsibility to do good for society. While provision of credit is essential to keep the economy flowing, we also recognise that we have a duty to help those who have yet to learn how to responsibly use debt.

The ABS introduced the DCP in January 2017. Under this plan, qualified borrowers can consolidate their outstanding unsecured debt at a single participating financial institution– including Standard Chartered. The DCP complements other debt remediation measures, such as the Debt Management Programme offered by Credit Counselling Singapore and the Debt Repayment Scheme under the Ministry of Law .

The DCP has garnered support from the Monetary Authority of Singapore (MAS), which has already taken proactive measures to prevent the accumulation of excessive debt. For instance, the authority implemented credit limit management measures in 2015, which restrict all financial institutions from granting further unsecured credit to individuals with borrowings that exceed a certain threshold .

That threshold has been progressively lowered since 2015, and as of June 2019, now stands at 12 times monthly income. This means that if your unsecured borrowings exceed your annual income, you would not be able to get higher or new credit limits or draw down further on existing facilities.

At Standard Chartered, we are doing our part by actively participating in the DCP. If you are struggling with your debt load, read the infographic below to learn everything you need to know about this plan.

At Standard Chartered, we can help you manage your debt through our Debt Consolidation Plan loans. Click here to. Contact us today.

Do you feel like you are drowning in debt? A debt consolidation loan may be what you need to get your financial house in order. Learn more about getting a loan under Singapore’s Debt Consolidation Plan here.

¹https://www.ccs.org.sg/services/dmp/

²https://io.mlaw.gov.sg/debt-repayment-scheme/about-debt-repayment-scheme/

³https://abs.org.sg/docs/library/faqs-credit-limit-management-measures.pdf