This is to inform that by clicking on the hyperlink, you will be

leaving

sc.com/sg

and entering a website operated by other parties.

Such links are only provided on our website for the convenience of

the Client and Standard Chartered Bank does not control or endorse

such websites, and is not responsible for their contents.

The use of such website is also subject to the terms of use and

other terms and guidelines, if any, contained within each such

website. In the event that any of the terms contained herein

conflict with the terms of use or other terms and guidelines

contained within any such website, then the terms of use and other

terms and guidelines for such website shall prevail.

One of the biggest investment debates of our times is whether to own cash or government bonds. In the Developed Markets, one of the most rapid policy rate hiking cycles in history has meant that short-term returns from cash are now higher than what one can earn on a longer maturity bond. Unsurprisingly, this has led to a significant move into cash deposits or money market funds across major economies around the world.

Despite this, many asset allocators (ourselves included) continue to advocate the case for high quality bonds over cash. Are the yield optics sending investors a false signal?

Yield today vs. yield tomorrow

If yields were the only drivers of total investment returns, then there would be little debate on which asset to choose – one could simply allocate to the asset class with the highest yield. In today’s market, that would be cash.

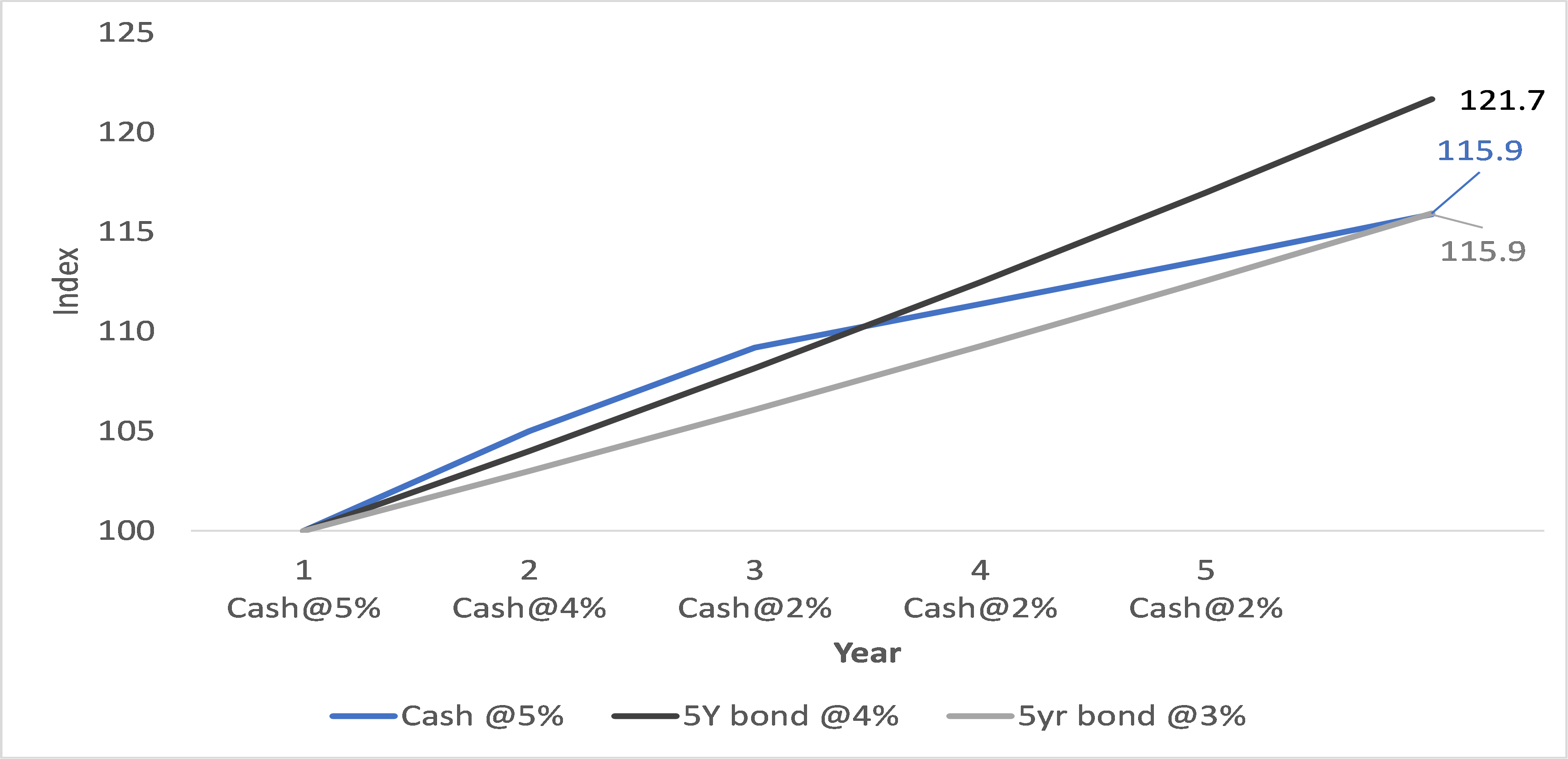

However, one needs to dig a little deeper in the investment world to figure out the real value of the two competing assets. The trade-off is best illustrated with a simple example. In the chart below, we compare three scenarios over a 5-year horizon:

– In the first scenario, an investor allocates to cash deposits, which currently yield around 5% over one year. We assume these yields stay relatively high at 5% and 4% in the first two years but fall to 2% thereafter as an economic recession unfolds and, in response, the central bank cuts short-term rates rapidly.

– In the second scenario, an investor buys a 5-year bond that yields 4% i.e., less than the return from cash. However, in this case, the investor can lock in the 4% yield for the next 5 years till the bond matures.

– In the third scenario, the investor buys another 5-year bond, but one that yields just 3%.

The chart illustrates how an investor’s returns pan out over the five-year period. In the first year, cash is clearly ahead with its higher yield.

However, as the one-year cash yield starts to drop in later years, returns fall rapidly. When the investor looks back with hindsight after 5 years, the 5-year bond yielding 4% (1 full percent below the cash yield) ended up being the investment that delivered the highest returns.

Cash only ended up matching returns for a 5-year bond that yielded 3%.

Quantifying reinvestment risk

Today’s investment environment is not that far off from our simple example – in US Dollars, 3-month US Treasury bills yield approximately 5.5%, while 5-year and 10-year US government bonds yield 4.6% and 4.5%, respectively.

Our stylised path of 1-year deposit rates over the coming years is also plausible, in our view. While it remains debatable how long the Fed holds rates at high levels, we continue to expect an economic recession over the next 6-12 months. History shows that a recession has always resulted in the Fed cutting interest rates rapidly in response. This means investors with cash deposits are likely to reinvest their deposits at much lower yields once their current deposits mature in the years ahead.

For investors, our example illustrates the real cost of reinvestment risk. Today’s yields optically favour cash deposits. However, we believe this is not the optimal decision for generating the highest total returns possible. Given where we are in the economic cycle, we continue to believe Developed Market government bonds offer a more attractive reward for the risk assumed relative to cash.

Some cash is prudent, but beware of losing purchasing power

Leaving aside the need for liquidity, some cash can make sense within an investment allocation. This was not really the case for a large part of the previous cycle when cash yields largely went to zero. However, ever since central banks began to raise rates rapidly, cash has become a little more competitive.

Nevertheless, there is little reason to expect cash to do a better job of preserving wealth in real (or inflation-adjusted) terms compared with riskier asset classes. The Optical yield illusion is making many investors respond to the headline yield on cash, but high-quality bonds are the hidden gems that are likely to outperform cash and better keep up with inflation over the coming years.

Disclaimer

This article is for general information only and it does not constitute an offer, recommendation or solicitation of an offer to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments. This article has not been prepared for any particular person or class of persons and does not constitute and should not be construed as investment advice or an investment recommendation. It has been prepared without regard to the specific investment objectives, financial situation or particular needs of any person or class of persons. You should seek advice from a licensed or an exempt financial adviser on the suitability of a product for you, taking into account these factors before making a commitment to purchase any product or invest in an investment. In the event that you choose not to seek advice from a licensed or an exempt financial adviser, you should carefully consider whether the product or service described herein is suitable for you.

You are fully responsible for your investment decision, including whether the investment is suitable for you. The products/services involved are not principal-protected and you may lose all or part of your original investment amount. Standard Chartered Bank (Singapore) Limited will not accept any responsibility or liability of any kind, with respect to the accuracy or completeness of information in this article.

Deposit Insurance Scheme

Singapore dollar deposits of non-bank depositors are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law. For clarity, these investment products are not deposits and do not qualify as an insured deposit under the Singapore Deposit Insurance and Policy Owners’ Protection Schemes Act 2011. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured.

Grow your wealth with insights, advice and Priority Banking