This is to inform that by clicking on the hyperlink, you will be

leaving

sc.com/sg

and entering a website operated by other parties.

Such links are only provided on our website for the convenience of

the Client and Standard Chartered Bank does not control or endorse

such websites, and is not responsible for their contents.

The use of such website is also subject to the terms of use and

other terms and guidelines, if any, contained within each such

website. In the event that any of the terms contained herein

conflict with the terms of use or other terms and guidelines

contained within any such website, then the terms of use and other

terms and guidelines for such website shall prevail.

3 Strategies to Build Financial Cushions now and Emerge Stronger for the Next Recession

3 Strategies to Build Financial Cushions now and Emerge Stronger for the Next Recession

The COVID-19 crisis has definitely taught us a number of life lessons. One key takeaway is no one can say that they are fully protected for certain — whether from the virus or from the economic effects of a major financial downturn.

For those of us fortunate enough to still have our health, jobs, and maintain our lifestyles, we have survived this financial downturn relatively unscathed thus far, but what can we do to prepare for and protect ourselves from the next one? How do we emerge stronger from COVID-19’s lessons?

The answer is to build a financial cushion for you and your family’s needs and requirements.

Why do we need a financial cushion?

With or without COVID-19, markets are cyclical, and economies go through boom-and-bust cycles, with major regional or global financial downturns happening every decade or so.

When a recession strikes, it is often accompanied by industry disruptions. And despite our best efforts towards continuous learning, certain job families could soon become irrelevant. Studies predict that by 2030, as much as 20 million jobs could be replaced by robots. This includes jobs in the manufacturing, cash services and food & beverage sectors, as companies increasingly rely on industrial robots and automation.

When redundancy occurs, we may not have enough savings to tide us through prolonged unemployment. To make matters worse, the value of our investments may have plummeted, and cashing them out would be of little use.

Knowing this, we should prepare financial safety nets that can cushion our fall even in times of volatility. So, besides cash savings and investments, what are our other options? This may come as a surprise to some, but could be the answer.

Here are three cushioning strategies that may suit different financial profiles.

1. The Full Body Pillow Strategy

The strategy: Imagine an immensely plush, deluxe, full-body cushion to land on if you fall. Reassuring, isn’t it?

How it works: Deploy your savings to maximum effect by getting a single premium insurance plan offering either a guaranteed lump sum payout or recurring income in the future. Or, opt for a tactical combination of both! Timed well, these plans can pay out when the next recession hits, so that you can receive an income even during a downturn.

Who is it suitable for: Those with sufficient spare cash idling in their bank accounts. Ideally, you would want to secure a future payout high enough to sustain your needs and lifestyle, and that typically requires a significant sum as the premium.

Why is this a good strategy: This is the most comfort that money can buy, because you pay a single amount upfront and will not need to be concerned about setting aside money for future payments, yet get financial security for your future. Furthermore, it may be an effective way to put your savings to work, rather than leaving the cash idle in your bank accounts.

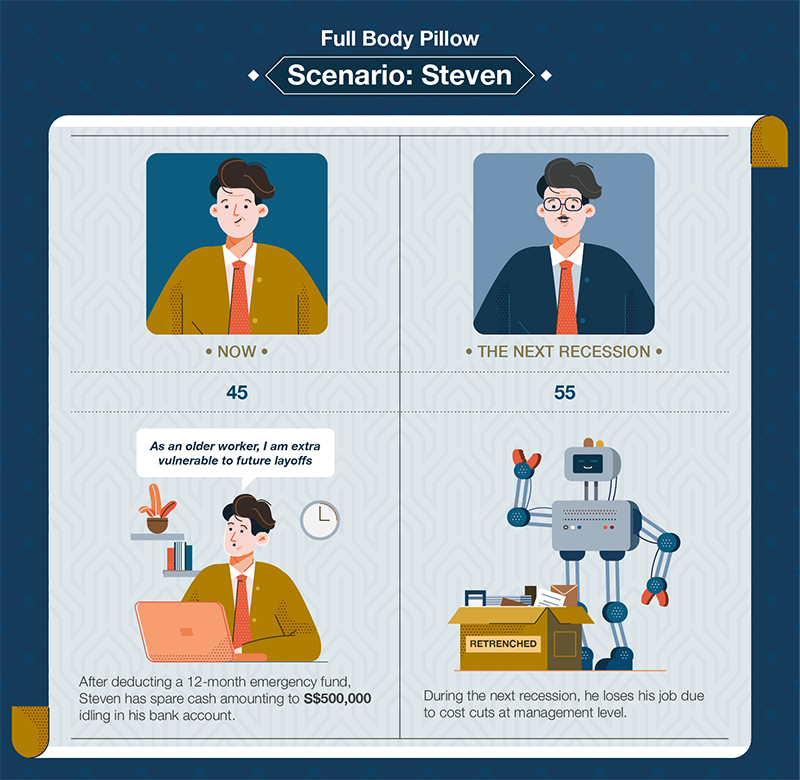

Scenario: Steven, 45, has spare cash amounting to S$500,000 sitting idle in his bank account (after deducting a 12-month emergency fund). He is not confident that he can continue working all the way till retirement age.

So, he purchases a single premium insurance plan that offers the option of regular payouts starting from 2 years later, but chooses to accumulate these cash payouts within the plan to collect interest until such point that he needs it. During the next recession, he loses his job due to cost cuts at management level, but fortunately, he is able to receive the lump sum cash payout (which he accumulated over the years) and activate regular payouts from the subsequent year onwards to help him through prolonged unemployment.

2. The Stack of Cushions Strategy

The strategy: Picture a stack of cushions. On its own, each one is not particularly thick or fluffy. But in a stack, they add up to a significant pile. Furthermore, you can adjust the cushion layers to the exact thickness you prefer.

How it works: Unlike the Full Body Pillow Strategy which requires a large outlay to provide ample cushioning, the Stack of Cushions Strategy breaks this down into several more affordable insurance plans. Simply purchase an insurance plan every time you accumulate enough savings and watch your stack of future payouts grow.

Who is it suitable for: Those who have irregular savings that are built up over time, and who are willing to put their savings into an insurance plan each time they have accumulated enough to purchase one.

Why is this a good strategy: It is a great compromise between security and affordability. You do not need a large amount of capital to start building up your cushion at the start, nor are you locked into a regular premium insurance plan which does not suit your savings style. You can slowly build up your stack of cushions at whatever pace is best for you.

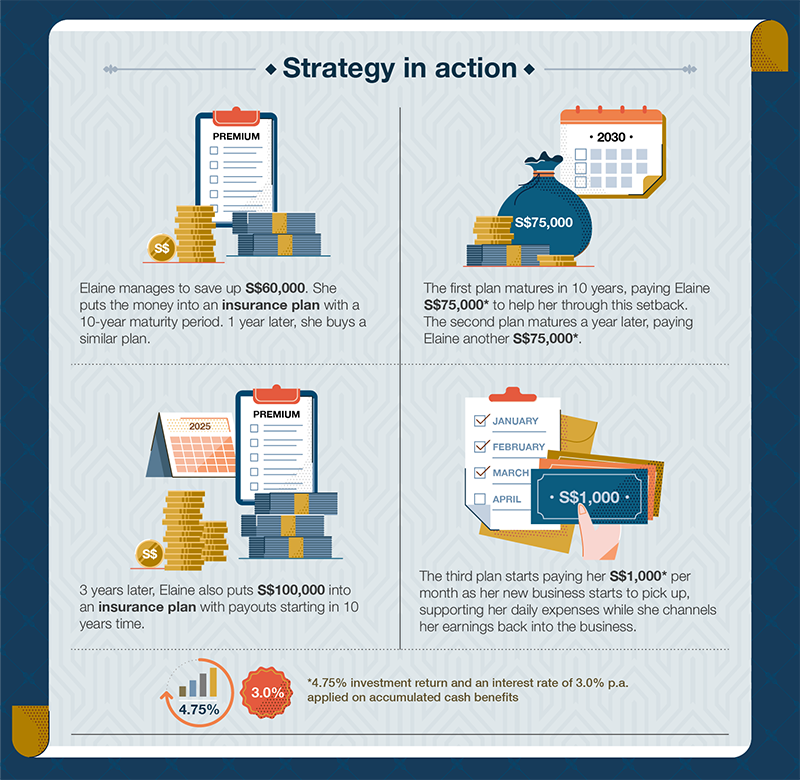

Scenario: Elaine, 40, is looking to build up her cushion while balancing the needs of her family and small home business. She is unable to commit a large lump sum upfront like Steven, but every time she manages to save up a bit of money, she puts it in an insurance plan. Over the years, she progressively builds up a “stack” of such plans. The next recession, these plans may reach their respective maturities and she can receive payouts.

3. The Slow & Steady Padding Strategy

The strategy: Imagine a small trickle of stuffing, filling up a cushion slowly. Initially, the cushion starts out thin, but over time it becomes much thicker and plusher. That’s how you afford financial cushioning in a slow and steady way.

How it works: Choose a regular premium insurance plan that you can contribute to in small monthly payments (premiums can be as low as S$80/month!) for a continuous period of several years. As long as you faithfully contribute that small amount each month to your insurance plan, your savings will gradually compound into a sufficient buffer against financial setbacks.

Who is it suitable for: Those with little savings at the moment but who wish to build up a financial cushion over time without taking on hefty commitments immediately. Think of this as a monthly subscription to your future financial security!

Why is this a good strategy: By forcing yourself to set aside a small amount of money each month, this strategy results in “paying your future self, first” before your funds flow into other wants and needs. With minimal intrusion on your current monthly cashflow, this strategy allows you to maintain a healthy emergency fund yet continue saving for big ticket items.

Scenario: Mark, 35, is a first-time father and is excited about his new phase of life. But he is unsure of his future commitments. He decides to put aside S$500 every month (a comfortable amount) into a regular premium plan, steadily growing his financial cushion. The next recession, he is the breadwinner supporting 3 growing kids and facing imminent pay cuts in his company. But thanks to the cushion he built up over a decade, he has a financial buffer which he can withdraw should he need it.

Financial cushions should be accessible to everyone, regardless of financial circumstances.

You don’t have to commit a huge sum immediately to enjoy financial cushioning; small amounts spread out over time can also contribute to a safety net. There is a strategy for everyone — you simply need to find your fit.

As the saying goes, “If you get tired, learn to rest, not to quit.” Rest on your financial cushions and emerge stronger from this crisis!

Disclaimer

^By clicking on this button, you are leaving the Standard Chartered Bank (Singapore) Limited website to access a third party website (“Third Party Website”).

Standard Chartered Bank (Singapore) Limited shall not be liable for the handling of any information you may provide on the Third Party Website, or for any loss incurred in connection with your access to or use of the Third Party Website. The Bank makes no warranties, representations or undertakings about the Third Party Website

This article and its infographics are for general information only and they do not constitute an offer, recommendation or solicitation of an offer to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments, nor do they constitute any prediction of likely future moments in rates, or prices or any representation that any such future movements will not exceed those shown in any illustration. This article and its infographics have not been prepared for any particular person or class of persons and they have been prepared without regard to the specific investment objectives, financial situation or particular needs of any person, and do not constitute and should not be construed as investment advice nor an investment recommendation. Where the article and its infographics describe any insurance product or service, they also do not constitute an offer, recommendation or solicitation of an offer to buy or sell any insurance product or service, nor are they intended to provide insurance or financial advice. You should seek advice from a licensed or an exempt financial adviser on the suitability of a product for you, taking into account these factors before making a commitment to purchase any product. In the event that you choose not to seek advice from a licensed or an exempt financial adviser, you should carefully consider whether the product is suitable for you.

Standard Chartered Bank (Singapore) Limited (the “Bank”) will not accept any responsibility or liability of any kind, with respect to the accuracy, or completeness of the information herein. The Bank makes no representation or warranty of any kind, express, implied or statutory regarding this article and its infographics or any information contained or referred to in this article and its infographics. This article and its infographics are distributed on the express understanding that, whilst the information in them is believed to be reliable, they have not been independently verified by the Bank.