This is to inform that by clicking on the hyperlink, you will be

leaving

sc.com/sg

and entering a website operated by other parties.

Such links are only provided on our website for the convenience of

the Client and Standard Chartered Bank does not control or endorse

such websites, and is not responsible for their contents.

The use of such website is also subject to the terms of use and

other terms and guidelines, if any, contained within each such

website. In the event that any of the terms contained herein

conflict with the terms of use or other terms and guidelines

contained within any such website, then the terms of use and other

terms and guidelines for such website shall prevail.

This article is an educational piece about uranium and nuclear energy. For informational purposes only.

We have all heard about the electrification that needs to happen in our generation. You would have probably read countless articles on batteries, solar panels, wind farms – the whole gamut. But nobody seems to be talking much about uranium. Not until recently, of course.

This blog is dedicated to providing a layman understanding of uranium (and nuclear energy!), and also some thoughts on what’s ahead for this market.

Uranium 101

Uranium is the fuel most widely used by nuclear power plants for nuclear fission. It is a radioactive material which is found pretty commonly in many places worldwide, but mining is currently concentrated in mainly 4 countries: Kazakhstan, Australia, Canada, and Namibia, which account for 75% of the world’s uranium production1.

Want to know how powerful uranium is? A single uranium pellet, slightly larger than a pencil eraser, contains the energy of a ton of coal, three barrels of oil, or 17,000 cubic feet of natural gas2.

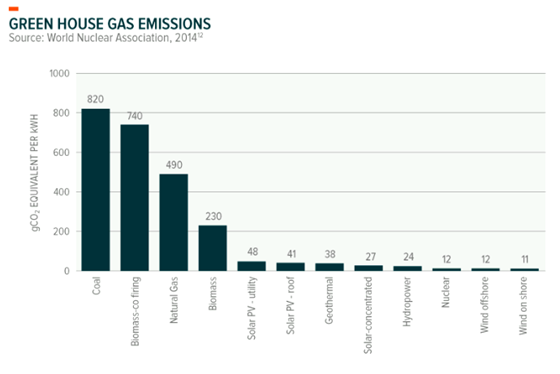

The best part? It is one of the cleanest and most cost-effective3 methods of producing energy. (See graph below for the pecking order, but no prizes for guessing which energy sources are the biggest polluters.)

So why is it that uranium and nuclear power are not particularly well covered by mainstream media?

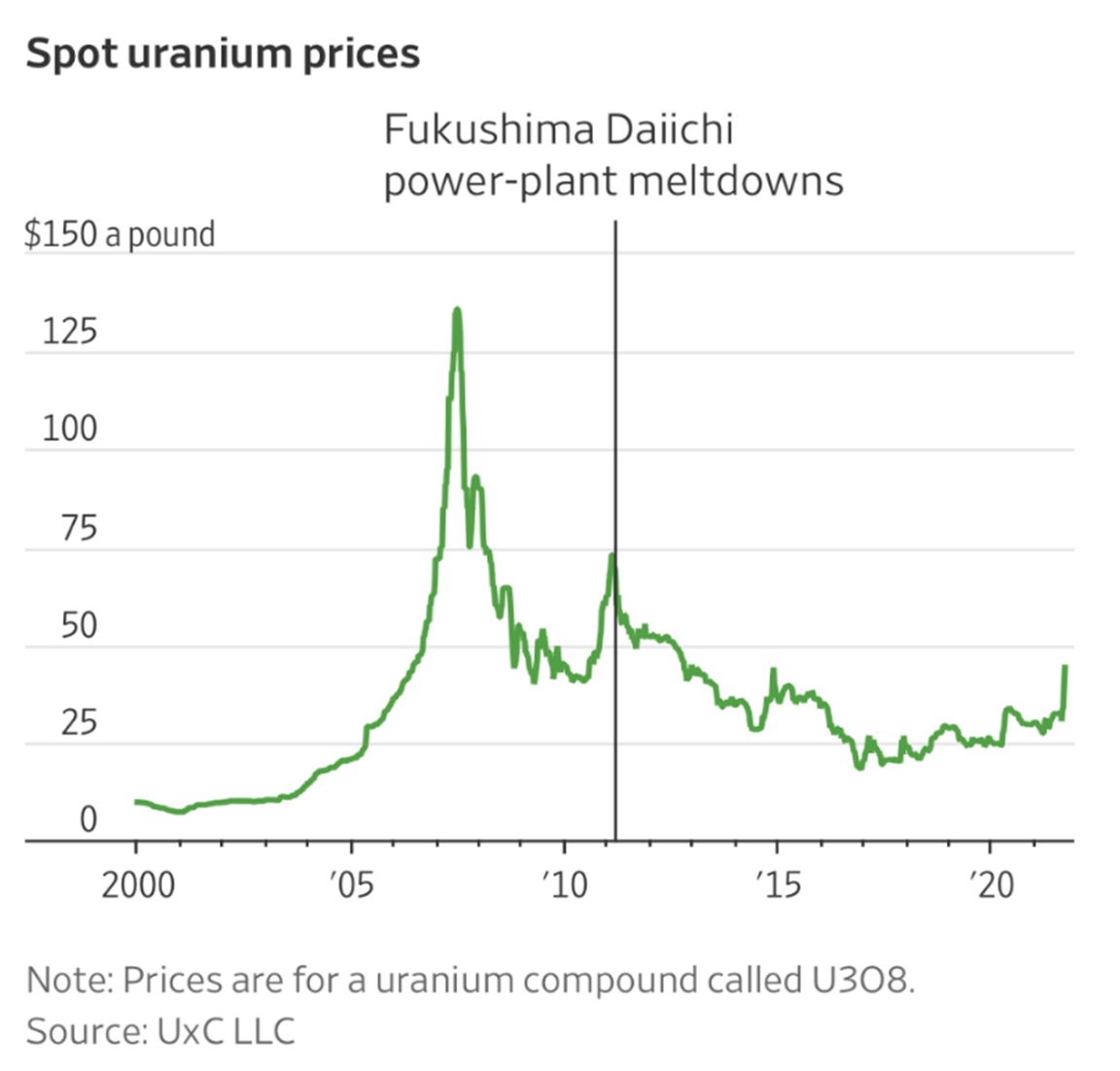

Well, it is simply because nuclear energy is in fact an extremely contentious topic – the 2011 Fukushima reactor meltdowns really gutted the industry. Following the disaster, Japan’s nuclear power production dropped from 30% to just 2%; all nuclear plants in the country were either closed down or suspended, and many countries (Germany, France, Switzerland) became wary and scaled back on their own operations. The price of uranium plummeted and has yet to regain its peak ever since.

However the tide is changing for uranium, it seems.

The Paris Climate Agreement in 2015 has brought about an interesting change in fate for the sector, as it urges every country to seriously consider at least a portion of its energy portfolio in nuclear power, to meet the ambitious climate goals.

Its main aim: for countries to reaffirm their commitments to keep global temperatures from warming above 1.5 degrees Celsius (relative to pre-industrial levels4) and effectively reach net zero5 by 2050.

However, according to the UN, the unfortunate reality is in fact that the world is set to warm 2.7 degrees century, because the countries’ current pledges are simply insufficient. So far, the commitments would only reduce 2030 emissions by 7.5%, when what is needed is in fact a 55% cut of emissions by 2030!

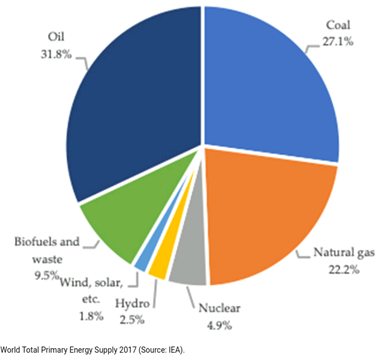

To make the matter worse, the intermittency of wind and solar power7 are revealing early cracks in our efforts to transit to “greener” pastures, and we find ourselves ever as reliant on the very fossil fuels we have been trying to tear ourselves away from. Based on stats from International Energy Agency (IEA), the world still relies heavily on oil, coal, and natural gas which make up the lion’s share of the world’s energy supply (see graph below). And because of the pandemic-induced disruptions, countries had ironically set record global carbon emissions8 in 2021, instead of cutting it.

World Total Energy Supply, 2017

The spike in energy prices in 2021 (and into 2022) made it clear that the transition to green energy and cleaner sources of power, is notthat easy after all. At point of writing, here are the stats from 4 Jan 2021 to present:

Uranium’s future: Is nuclear about to have its next renaissance?

In a message released just before the climate summit, the Director General of IAEA9, Raphael Grossi acknowledged that “the choice of energy sources remains a sovereign decision and every country has different needs”. But he notes that more and more scientists, policymakers and members of the public are starting to recognize nuclear as a critical part of decarbonized energy systems10.

Two examples stand out for me.

Both England and France have shown that they are making nuclear energy a pillar of their energy strategies going forward.

France:

Nuclear power currently provides France with 70% of the electricity it consumes, the highest in the world.11 As a result, France also boasts one of the lowest-cost electricity schemes in the EU.

In the face of Europe’s energy crisis, France has recently committed to investing €1 billion in nuclear power by 2030, as well as an intention to roll out small modular reactors (SMR). We’ll get to SMRs in a bit.

UK:

According to Yardeni research, nuclear power provides about 16.8% of Britain’s electricity generation in 2019.12

The UK’s plan to reach net zero carbon emissions by 2050 is expected to rely on building more nuclear power plants, which is necessary because almost all of the country’s existing nuclear plants, some of which date back to the 1950s, are scheduled to be retired by 2035. They currently have one large nuclear plant under construction, with two more on the drawing board. Similarly, UK is also looking to invest into the build out of SMRs as well.

Next Gen Nuclear: What are SMRs?

Small modular reactors (SMRs) are the less expensive and less risky cousins of traditional nuclear reactors. Fun fact: they are small enough to fit in the back of a truck! They have lower safety radius requirements (known as EPZ ie. Emergency planning zones), which means they could be more easily inserted into a community to be used to electrify a small town or provide the energy to an industrial plant.

SMR developers and potential operators argue that SMRs are safe enough to have a safety radius of under 5km, which would benefit local governments in that it would minimize disruptions to communities, and not drastically hamper federal budgeting or spatial planning. These SMRs could even sit on offshore floating rigs to power a coastal city or assist in water desalination13.

It is projected that the global SMR market could grow to USD 11.3 billion by 2026 from an estimated USD 9.7 billion in 202114, the growth dominated by Asia Pacific, followed by Europe.

Well, if these stats failed to pique your interest in SMRs, then perhaps this will: Bill Gates, – yes, the same forward-looking guy that pretty much predicted Covid would happen15 – Bill Gates is excited about and has been investing in SMRs, in fact since 2006!16

In June 2021, Reuters reported that Bill Gates’ advanced nuclear reactor company, TerraPower, would launch their first nuclear project on the site of a retiring coal plant – a sign of the changing times. In that same report, it also mentioned how the project would lift up that region’s once active uranium mining industry.17

So what are the investible opportunities out there?

Quite a number of the major players in the SMR market are currently private18. As such, for retail investors, perhaps the easiest way to gain access to this sector is via Uranium-themed ETFs for now.

• Global X Uranium ETF(URA) – incepted in 2010 and the largest by AUM & volume, provides investors targeted access to companies involved in uranium mining and the production of nuclear components. Its 3 largest holdings are:

• North Shore Global Uranium Mining ETF(URNM) – incepted in 2019, also provides concentrated access to a similar set of uranium miners, plus it also invests into companies that hold the physical element. Its 3 largest holdings are:

◦ Sprott Physical Uranium Trust (U-U), which holds physical uranium.

• VanEck Uranium+Nuclear Energy ETF(NLR) – incepted in 2007, provides investors with a slightly different exposure. 87% of the fund’s assets are invested in utility companies that produce electricity from nuclear sources. Its largest holdings include names like:

◦ Dominion Energy (D),

◦ Duke Energy (DUK),

◦ Electricite De France (EDF).

Concluding Thoughts

The use of nuclear energy is definitely not an easy topic to cover. As with many controversial topics these days, there is both a “pro-nuclear” camp as well as an “anti-nuclear” camp. Beware: discussing this topic over a casual coffee may potentially invoke spirited discussions and big emotions, and is quite often politically divisive too19.

On the “anti-nuclear” camp, the downsides would include:

• Concerns around radioactive waste management

• Nuclear energy’s dangerous proximity to nuclear weapon proliferation

• Adverse public opinion

• Fear of nuclear accidents occurring

Ultimately, I believe it might boil down to how urgent the climate agenda is, and how open each country is to seeking out alternatives to the traditional fossil fuel sources. In the end, it is likely that countries would settle for a compromise of several different sources of energy for diversification20.

While the outlook for uranium remains uncertain, it does seem clear that people are starting to approach the adoption of nuclear power with a much better disposition than before. It might be early days for us still, but this asset class is definitely worth keeping an eye on.

Map of countries with operational nuclear power programs

Cheryl is a (hard)working mom with three school-going kids, and identifies as a millennial. She enjoys converting difficult concepts into simple and bite-sized ideas that people can use.

In her free time, you will find her nurturing (read: nagging) her three beautiful children towards following the Singapore dream (whatever that means). In this post-Covid world, she often daydreams about the next time she will get to hike in some faraway mountain where the weather is not eternally humid.

This article is for general information only and it does not constitute an offer, recommendation or solicitation of an offer to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments.

This article has not been prepared for any particular person or class of persons and does not constitute and should not be construed as investment advice or an investment recommendation. It has been prepared without regard to the specific investment objectives, financial situation or particular needs of any person or class of persons. You should seek advice from a licensed or an exempt financial adviser on the suitability of a product for you, taking into account these factors before making a commitment to purchase any product or invest in an investment. In the event that you choose not to seek advice from a licensed or an exempt financial adviser, you should carefully consider whether the product or service described herein is suitable for you. You are fully responsible for your investment decision, including whether the investment is suitable for you. The products/services involved are not principal-protected and you may lose all or part of your original investment amount. Standard Chartered Bank (Singapore) Limited will not accept any responsibility or liability of any kind, with respect to the accuracy or completeness of information in this article.

This document is being distributed for general information only and is subject to the relevant disclaimers available here. It is not and does not constitute research material, independent research, an offer, recommendation or solicitation to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments. This document is for general evaluation only. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person or class of persons and it has not been prepared for any particular person or class of persons. You should not rely on any contents of this document in making any investment decisions. Before making any investment, you should carefully read the relevant offering documents and seek independent legal, tax and regulatory advice. In particular, we recommend you to seek advice regarding the suitability of the investment product, taking into account your specific investment objectives, financial situation or particular needs, before you make a commitment to purchase the investment product. Opinions, projections and estimates are solely those of SCB at the date of this document and subject to change without notice. Past performance is not indicative of future results and no representation or warranty is made regarding future performance. Any forecast contained herein as to likely future movements in rates or prices or likely future events or occurrences constitutes an opinion only and is not indicative of actual future movements in rates or prices or actual future events or occurrences (as the case may be). This document must not be forwarded or otherwise made available to any other person without the express written consent of the Standard Chartered Group (as defined below). Standard Chartered Bank is incorporated in England with limited liability by Royal Charter 1853 Reference Number ZC18. The Principal Office of the Company is situated in England at 1 Basinghall Avenue, London, EC2V 5DD. Standard Chartered Bank is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and Prudential Regulation Authority. Standard Chartered PLC, the ultimate parent company of Standard Chartered Bank, together with its subsidiaries and affiliates (including each branch or representative office), form the Standard Chartered Group. Standard Chartered Private Bank is the private banking division of Standard Chartered. Private banking activities may be carried out internationally by different legal entities and affiliates within the Standard Chartered Group (each an “SC Group Entity”) according to local regulatory requirements. Not all products and services are provided by all branches, subsidiaries and affiliates within the Standard Chartered Group.

Market Abuse Regulation (MAR) Disclaimer Banking activities may be carried out internationally by different branches, subsidiaries and affiliates within the Standard Chartered Group according to local regulatory requirements. Opinions may contain outright “buy”, “sell”, “hold” or other opinions. The time horizon of this opinion is dependent on prevailing market conditions and there is no planned frequency for updates to the opinion. This opinion is not independent of Standard Chartered Group’s trading strategies or positions. Standard Chartered Group and/or its affiliates or its respective officers, directors, employee benefit programmes or employees, including persons involved in the preparation or issuance of this document may at any time, to the extent permitted by applicable law and/or regulation, be long or short any securities or financial instruments referred to in this document or have material interest in any such securities or related investments. Therefore, it is possible, and you should assume, that Standard Chartered Group has a material interest in one or more of the financial instruments mentioned herein. Please refer to https:// www .sc. com/en/banking-services/market-disclaimer.html for more detailed disclosures, including past opinions/ recommendations in the last 12 months and conflict of interests, as well as disclaimers. A covering strategist may have a financial interest in the debt or equity securities of this company/issuer. This document must not be forwarded or otherwise made available to any other person without the express written consent of Standard Chartered Group.

Deposit Insurance Scheme

Singapore dollar deposits of non-bank depositors are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law. For clarity, these investment products are not deposits and do not qualify as an insured deposit under the Singapore Deposit Insurance and Policy Owners’ Protection Schemes Act 2011. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured.

This advertisement has not been reviewed by the Monetary Authority of Singapore.