This is to inform that by clicking on the hyperlink, you will be

leaving

sc.com/sg

and entering a website operated by other parties.

Such links are only provided on our website for the convenience of

the Client and Standard Chartered Bank does not control or endorse

such websites, and is not responsible for their contents.

The use of such website is also subject to the terms of use and

other terms and guidelines, if any, contained within each such

website. In the event that any of the terms contained herein

conflict with the terms of use or other terms and guidelines

contained within any such website, then the terms of use and other

terms and guidelines for such website shall prevail.

Five key tips for buying property as an investment or a home

This article is for information purposes only.

It is common for many to view property as a path to wealth; and for some it is both an investment asset, as well as a home. However, homeowners and investors have different needs in a property. Here is what you need to consider before purchasing a property.

Tip 1: Know what your long-term plan for the property is

There are three types of property buyers:

Owner-occupiers

Owner-occupiers are pure homeowners. They are more focused on whether the property suits their lifestyle and needs.

An owner-occupier has no interest in rental gains (as they will not rent out their home anyway) and is not overly concerned with resale gains. Some owner-occupiers may intend to live out their entire lives in the property, or to simply pass on the home to future generations.

Owner-occupiers focus on details such as whether the property is close to their workplace, close to their children’s school or parents, or whether they like the surrounding neighbourhood. They may even be willing to pay above-average prices, to secure a home that suits these needs.

Owner-investors

Owner-investors may see their property purchase as a “starting step”. They have intentions toward asset progression: that means they intend to sell at some point and move to a better home.

A common example would be a young couple, who start off with a small two-bedroom apartment. This is not large enough to house a family; but they hope that the property will appreciate over time. They can then sell it and combine the sale proceeds with their savings to buy a larger home.

Alternatively, owner-investors may see their property as a form of retirement asset. They buy a large home but expects to sell it and downgrade to a smaller home upon retirement; the sale proceeds will be used to boost their retirement funds.

As owner-investors still live in the same property, they are concerned about details like the surrounding neighbourhood, presence of good schools, proximity to work, and so forth.

Pure investors and landlords

These are property investors who are focused on rental and resale gains. They are usually purchasing their second or third property, and often don’t reside in the property by themselves.

They are concerned only about the rentability of the property (if they want tenants), the rental yield, and capital gains when they resell.

Tip 2: Understand how to make money from property and the accompanying risks

There are two main ways to make money from your property: capital gains, and rental income.

Capital gains

You make a capital gain when you sell your property for more than you bought it, even after expenses.

A simple example:

You purchase your home for $1.5 million in the year 2010 and resell it for $1.9 million in 2020. Along the way, you incur various costs (see below) which amount to $200,000.

This gives you a net gain of $200,000, upon the sale of the property (before any relevant taxes in your country).

Note that, because the property is not rented out, it is an overhead until you sell it.

Relying on capital gains involves a degree of risk. There is no guarantee that you can sell your property for more than its initial purchase price. Real estate prices fluctuate over time – if you sell during a downturn or make a fire sale (i.e., selling fast during a crisis), you could even incur a capital loss.

Rental income

If you rent out the property to tenants, it can become a cash-generating asset. A common metric used to estimate rental asset, is the gross rental yield. This is the annual rental income, divided by the total cost of the property.

For example, a property that generates $42,000 in annual rent, but costs $1.5 million, would have a gross rental yield of about 2.8 per cent.

This is only a rough estimate however, and serious investors also need to work out the net rental yield (i.e., the yield after deducting recurring costs such as mortgage interest, maintenance fees, property taxes, and other costs).

Relying on rental income also carries a strong element of risk. There is no way to guarantee that you will have tenants. Don’t forget the process of looking for tenants, such as with the help of a realtor or by posting listings, also incurs a marketing cost. Also, rental rates fluctuate over time; there is no certainty that, many years down the road, you can still charge the same rental rates as today.

Tip 3: Know what can affect the prices and value of your property

Some of the main factors that affect property prices include:

I. Supply and demand

When there is a shortage of homes and a high demand for housing, then home prices tend to rise. Conversely, prices tend to fall if there are many vacant homes available, but few interested buyers.

II. Changes to the surrounding neighbourhoods

It is important to check the development plans in your neighbourhood before you buy property there. Look out for urban planning showcases or master plans for indication what will be built nearby.

Future developments can be a detriment or advantage to your property value. If a new high-rise condominium complex springs up right in front of yours and affecting the view and greenery, it will likely lower your property value. On the flip side, the emergence of good schools, better public transport nodes, or new amenities like parks and libraries can boost property value.

III. Government policies on housing

Governments can raise or lower property taxes and impose new stamp duties on property purchases. This can severely impact demand and property prices. There is, unfortunately, no reliable way to predict government actions; so, these are perpetual risks faced by property investors.

IV. Lease decay

Properties that are nearing the end of their lease will see falling values, although the rate of depreciation can vary widely. Lenders also tend to be more restrictive in giving out home loans for properties that are near the end of their lease, or which have worn out over time.

V. Holding power

Properties that must be sold urgently (referred to as fire sales) may transact at a loss: buyers might agree to complete a transaction in the span of a few days, but only at a steep discount. As such, holding power – your ability to wait out downturns or rental vacancies – are a major factor in resale gains.

These are just some of the many factors that can impact your property value; and it is better not to take the term “safe as houses” too literally. While property prices may not be as volatile as some other assets, real estate is not free of its own fluctuations.

Tip 4: Check if you can afford purchasing a property (upfront fees plus recurring fees)

We have looked at the factors affecting property value, let’s understand the costs (and hidden ones) to buy a property.

I. Minimum down payment

Lenders can only provide a certain loan amount (called the loan quantum) for your property; the rest of it must be covered with your own cash.

The loan amount is commonly expressed as the Loan To Value (LTV) ratio. This is the percentage of the property value that a lender can finance. For example, if your property is valued at $1 million, and the LTV is 75 per cent, then the lender can loan you $750,000 at most. You would need to plan for a minimum down payment of $250,000.

Not sure whether you have sufficient money or how to bridge the shortfall to buy your property few years down the road? Use Standard Chartered Goals Planner to simulate your property goal and get a consolidated view of your net worth, cashflows and savings. As everyone’s situation and needs are different, discover suitable opportunities for your money and optimise your road to home ownership.

II. Stamp duties

Stamp duties are added fees required to complete your property purchase. They are usually paid at or close to the time of completing the transaction.

Some countries charge higher stamp duties to foreigners or temporary residents, so it is important to check the amounts before buying.

III. Legal fees

Also called conveyancing fees, these are paid to the law firm handling the papers for your property purchase.

The fees charged will vary based on the law firm you use; specialised conveyancing firms tend to charge less, while established law firms may have higher fees.

IV. Commissions to realtors

A realtor’s commission is usually a percentage of the property price, which should be agreed upon before you engage their services.

In some countries, it may be possible to buy and sell properties without the help of a realtor; while others, it is common practice for the seller or buyer to pay for it.

V. Renovation, furnishing & other recurring costs

Older homes tend to require more renovation and refurnishing. The overall cost of renovations, however, will depend on how elaborate your plans are.

Besides, the initial costs, there are some recurring costs to consider. These include the monthly loan repayment, maintenance fees, property taxes, and any required insurance premiums.

– Fire and flood insurance covers the cost of rebuilding your home in the event of fire, or some other natural disasters. This type of insurance is required by law in some countries and may be necessary to get a home loan.

– Home content insurance covers damages to items inside your home, such as furniture, valuables, some appliances, and so forth. Fire insurance does not cover such items. Home content insurance can also cover – to a limited degree – losses from burglary, and third-party liability (for example, if flooding from your home damages your neighbour’s home, and you are held liable).

– Mortgage insurance pays off your remaining mortgage, in the event of death or permanent disability. This policy does not cover any damages to your home, it is only for paying off the mortgage.

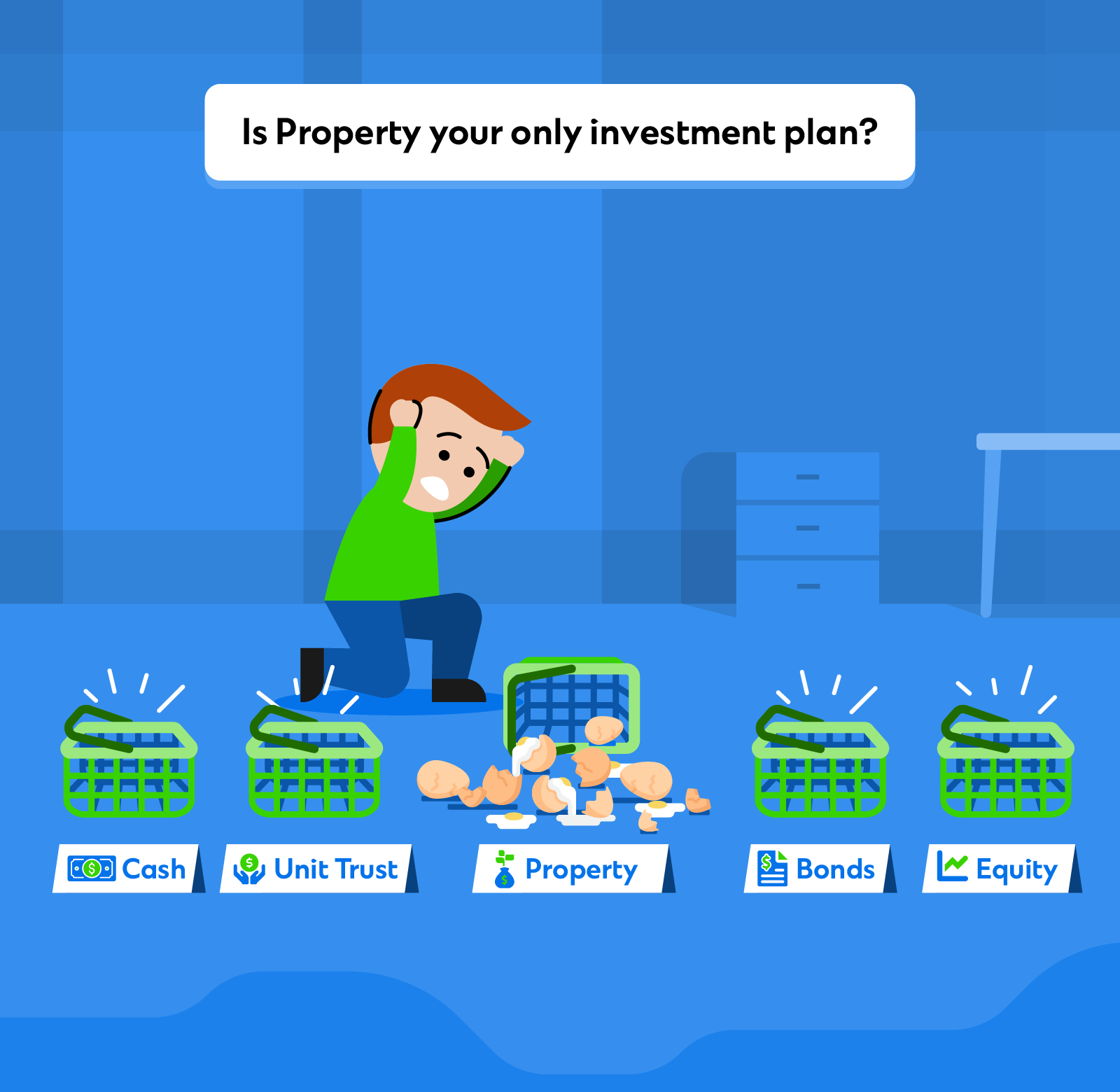

Tip 5: Avoid seeing property as a “one-stop” financial solution, rather it can be a part of your investment portfolio

As the saying goes: Do not put all your eggs in one basket. Refrain from treating your property as your entire investment plan. As explained above, you cannot predict the eventual resale gains of your property or count on perpetually strong rental demand.

It is more prudent to look at property as just one part of a diversified and well-balanced portfolio. Complement your property returns with other assets, such as unit trusts, insurance savings plans, or equities that can potentially bring you higher returns.

If you want to avoid the high capital costs and complexities of buying property, you can consider Real Estate Investment Trusts (REITs).

REITs are funds that invest in a portfolio of properties, usually with some specialisation (e.g., there are office REITs, retail REITs, hotel REITs, and others). The rental returns of these properties are paid out as dividends to investors, and units in REITs can be bought or sold on a stock exchange. This is much less capital intensive and liquid than buying physical property. You can access a wide range of REITs on Standard Chartered Online Trading.

A well-chosen property is a home or an appreciating asset, rarely a liability. Speak to Standard Chartered’s Relationship Managers, or visit any of our branches, to find out the best way to save and budget for your new property, or to find alternative, affordable ways to invest in real estate.

Disclaimer

This article is for general information only and it does not constitute an offer, recommendation or solicitation of an offer to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments. This article has not been prepared for any particular person or class of persons and does not constitute and should not be construed as investment advice or an investment recommendation. It has been prepared without regard to the specific investment objectives, financial situation or particular needs of any person or class of persons. You should seek advice from a licensed or an exempt financial adviser on the suitability of a product for you, taking into account these factors before making a commitment to purchase any product or invest in an investment. In the event that you choose not to seek advice from a licensed or an exempt financial adviser, you should carefully consider whether the product or service described herein is suitable for you.

You are fully responsible for your investment decision, including whether the investment is suitable for you. The products/services involved are not principal-protected and you may lose all or part of your original investment amount. Standard Chartered Bank (Singapore) Limited will not accept any responsibility or liability of any kind, with respect to the accuracy or completeness of information in this article.

Deposit Insurance Scheme

Singapore dollar deposits of non-bank depositors are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law. For clarity, these investment products are not deposits and do not qualify as an insured deposit under the Singapore Deposit Insurance and Policy Owners’ Protection Schemes Act 2011. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured.