This is to inform that by clicking on the hyperlink, you will be

leaving

sc.com/sg

and entering a website operated by other parties.

Such links are only provided on our website for the convenience of

the Client and Standard Chartered Bank does not control or endorse

such websites, and is not responsible for their contents.

The use of such website is also subject to the terms of use and

other terms and guidelines, if any, contained within each such

website. In the event that any of the terms contained herein

conflict with the terms of use or other terms and guidelines

contained within any such website, then the terms of use and other

terms and guidelines for such website shall prevail.

Infrastructure – A place for investors to hide in 2022

Written by Winnie Lim, Investment Advisor

The article is an educational piece on listed infrastructure assets. For informational purposes only.

Infrastructure is widely regarded as a comparatively low-risk asset class, with a longer-term investment horizon than other investments. While not as topical or fashionable as its technology counterparts, listed infrastructure assets are still worth a look.

In this article, I will share 1) what constitutes listed infrastructure assets; 2) why investors are increasingly seeking refuge in this asset class; 3) their growing importance as well as 4) their investment performance resiliency relative to other equities and bonds.

What are Listed Infrastructure Assets? 1

Infrastructure assets are physical assets that provide an essential service to society. These are the services we use and interact with every day. For instance, we use gas, water and electricity to carry out our daily activities and infrastructure such as airports, rail and roads help to move people and goods from one place to another.

There are four major categories of infrastructure assets, as seen in Figure 1. Out of these four categories, Regulated Assets and User Pays Assets can generate income for investors. You may refer to the Appendix for a detailed explanation on Regulated Assets and User Pays Assets.

Figure 1: Infrastructure 101

Source: ClearBridge. For illustrative purposes only.

Community & Social

Regulated Assets

User Pays Assets

Competitive Assets

– Government backed cash flows, availability payment

– Hospitals, schools, housing etc.

– Asset based regulation, return on assets/equity

– Poles, wires, pipes

– Defensive assets, high income, low GDP exposure.

-Concession based contracts

– Roads, rail, ports, airports

– Growth assets, lower income, leveraged to GDP.

– Unregulated assets, supply /demand risk

– Energy retail & generation, logistics, exploration and production.

Boring is Beautiful – The General Case for Listed Infrastructure Assets 2

Though listed infrastructure assets may not be as exciting as their technology counterparts, in volatile times like this, boring may be the way to go. Moreover, it is an asset class with attractive investment attributes.

– Lower Volatility

Demand for infrastructure assets tend to be stable and almost inelastic, making them relatively insensitive to economic fluctuations. Even at times of economic weakness, consumers continue to use water, electricity and gas, drive cars on toll roads and use other essential infrastructure services. This means lower volatility than global equities, as seen in Figure 2, and greater resiliency of revenues across business cycles.

Figure 2: 5-year Annualized Volatility

Source: Bloomberg, Data as of 30 Jun 2022. Global bonds represented by the Bloomberg Global Aggregate Bond Index; Global equities represented by the MSCI All Country World Gross Total Return USD Index; Global listed infrastructure represented by the FTSE Global Core Infrastructure 50/50 Total Return USD Index.

– Stable Cash Flows & Stable Dividends

Infrastructure companies provide predictable income distributions, as they are usually government regulated, and/or have long-term contracts that provide stable cash flow and greater capital stability. For example, utility, gas, water and electricity companies provide essential services in our lives that we need regardless of how well the economy is doing. For investors, this provides excellent visibility for revenues and dividends.

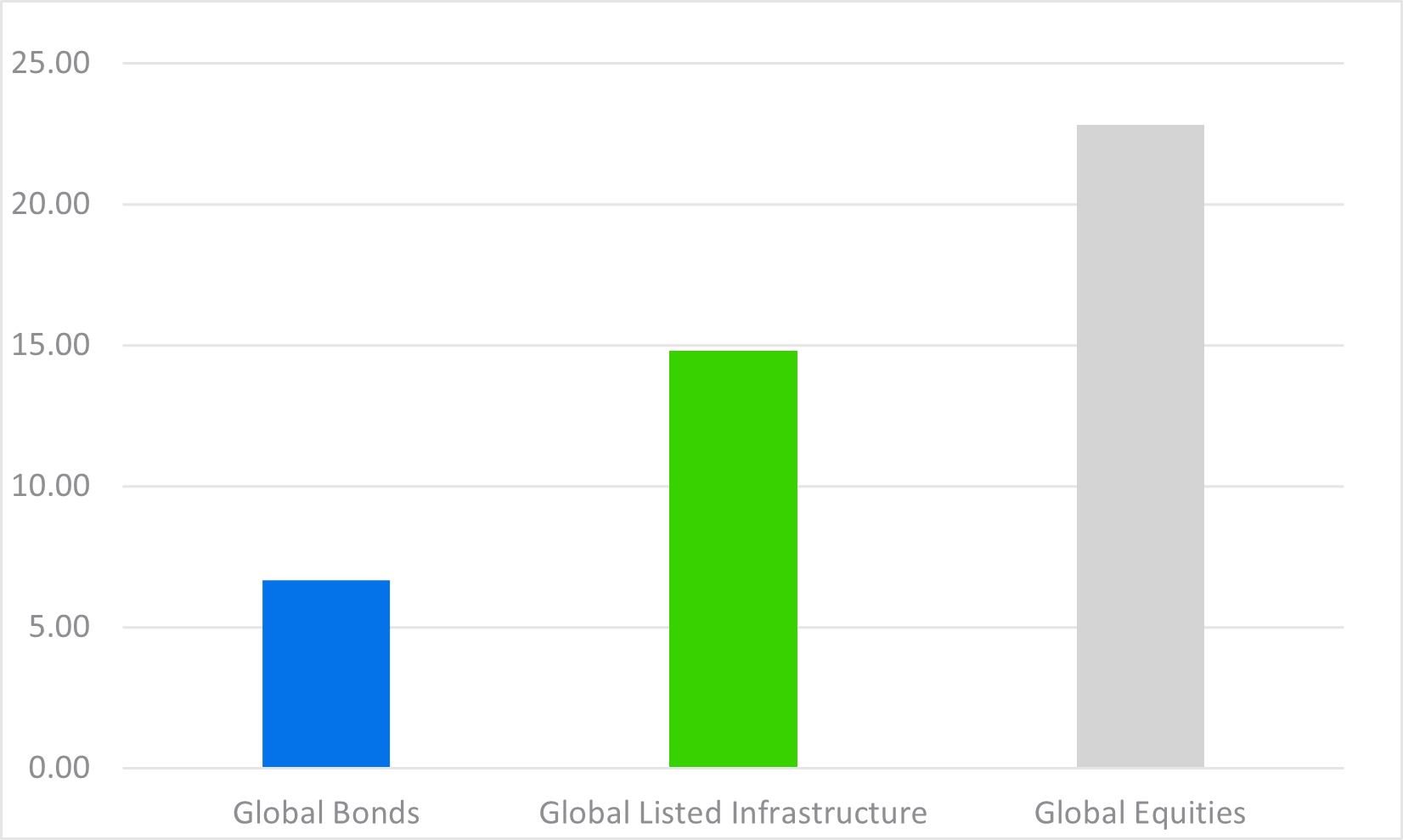

Compared to traditional bonds and equities, listed infrastructure assets are dividend cows, offering the potential for higher yields, as seen in Figure 3. This is a desirable attribute to have for income-seeking investors.

Figure 3: 12-month Forward Dividend Yield (Global Listed Infrastructure and Global Equities) & Yield-to-worst (Global Bonds)

Source: Bloomberg, Data as of 31 Dec 2021. Global bonds represented by the Bloomberg Global Aggregate Bond Index; Global equities represented by the MSCI All Country World Gross Total Return USD Index; Global listed infrastructure represented by the FTSE Global Core Infrastructure 50/50 Total Return USD Index.

– Inflation Hedge

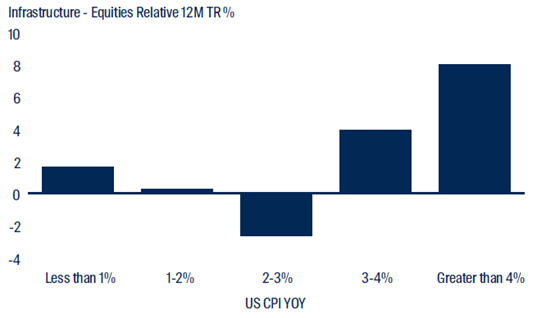

Revenues of most infrastructure assets have an explicit link to inflation through regulation, concession agreements or contracts which provide inflation protection to investors. For instance, utility companies are able to increase their prices to end consumers when inflation increases, raising revenues and cashflows as a result. This makes the asset class a good hedge against inflation. Figure 4 shows that global infrastructure has outperformed global equities during periods where US CPI is greater than 3%.

In today’s environment where we are seeing the highest inflation numbers in 40 years, listed infrastructure assets will help to hedge the risk of persistent inflation from investors’ portfolios.

Figure 4: Infrastructure Performance During Periods of Inflation

Source: Bloomberg, First Sentier Investors. Quarterly time series from 2006-2021. Equities represented by the MSCI Daily TR Gross World USD; Infrastructure represented by the FTSE Global Core Infrastructure 50/50 Net TR Index (USD).

– Diversification

As the underlying return streams are strongly linked to regulatory or contractual frameworks, rather than typical drivers of equity or bond returns, global listed infrastructure can provide diversification to one’s investment portfolio, especially in times of market stress.

What will drive growth in the infrastructure sector?

Infrastructure spending is expected to grow in both developed and emerging economies. In developed economies, an increased need for maintenance, facilities upgrades, capacity boosts as well as the embracement of environment sustainability will escalate infrastructure expenditure.

The unwavering policy support towards net zero by 20503 is a huge push for countries to explore alternative energy supplies. This means a surge for green infrastructure to support renewable energy adoption to fulfil the global energy demand.

Meanwhile in the Emerging Markets, expected increase in population growth and urbanization will similarly facilitate the expansion of infrastructure. By 2050, 68% of the world’s population is projected to be urban compared with 55% in 2018.4

Figure 5: Estimated Global Infrastructure Spending 2018 – 2040

Source: ClearBridge. International Energy Agency, (2018), World Energy Outlook, iea.org/weo2018/electricity, as of November 2018.

USD 20 trillion

USD 8.4 trillion

USD 8.6 trillion

– investment in electricity supply/efficiency

– in regulated /contracted generation (gas, solar, wind)

– in networks /storage

How did the infrastructure sector perform?

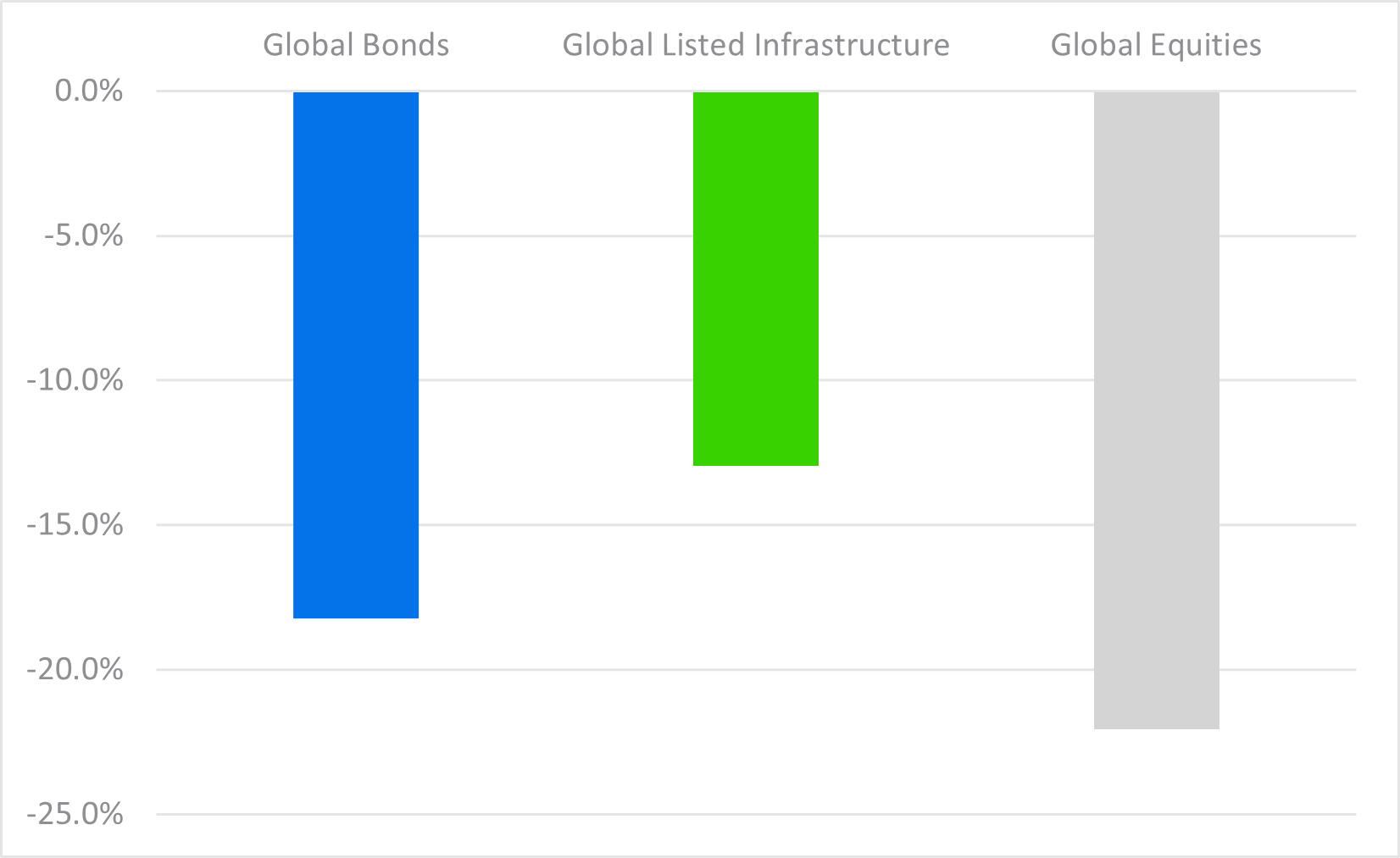

The S&P 500 started the year having more than doubled from the lows it hit in March 2020, an upswing that went into reverse almost immediately as the calendar flipped to 2022. Bonds were not spared either as the Fed signaled earlier in the year that it was pivoting to tighter monetary policy in order to tamp down surging inflation, a significant change to the investing environment.5

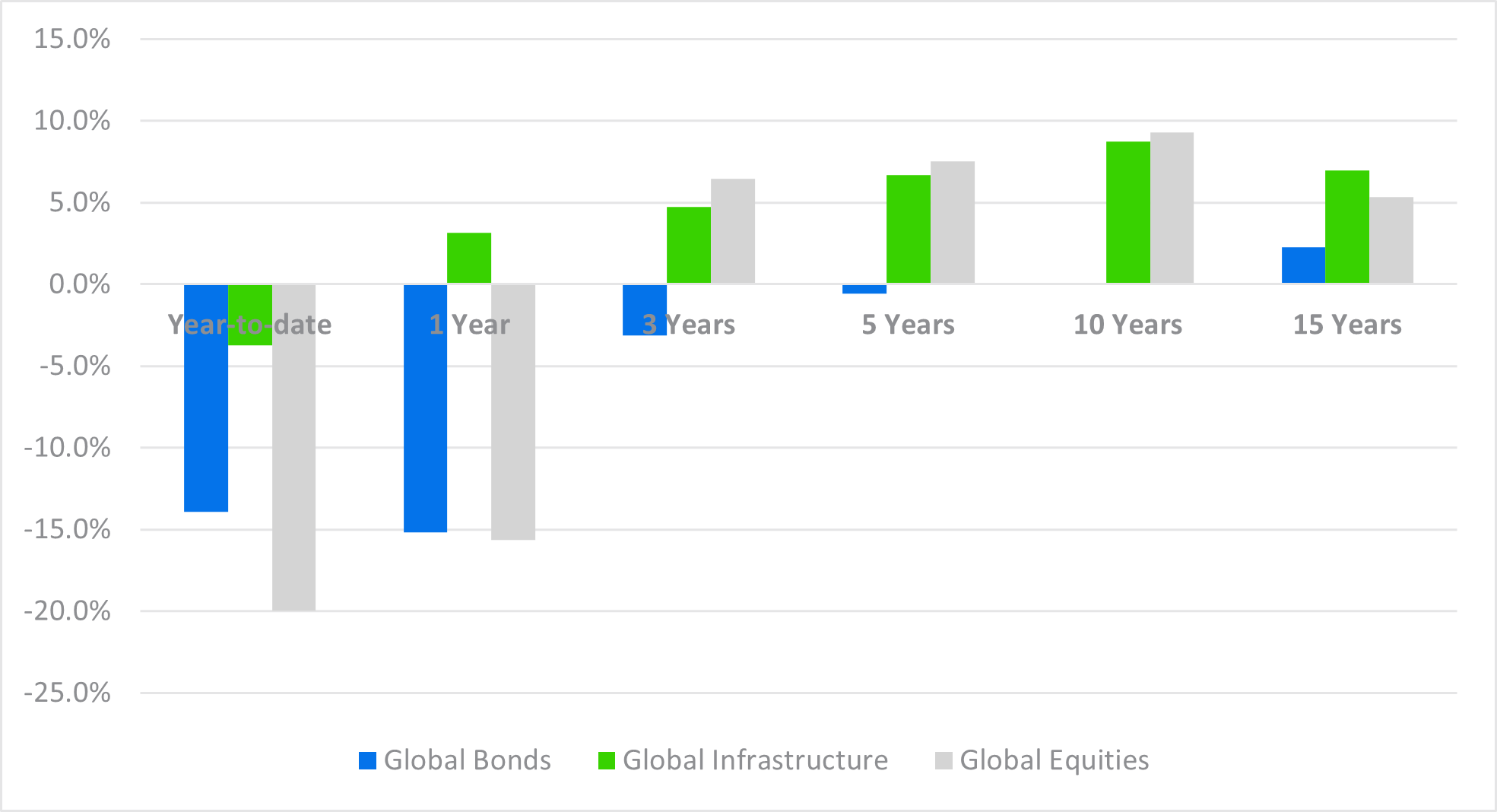

As a result, as seen in Figure 6, global equities and global bonds were down 20% and 14% YTD respectively. On the flip side, infrastructure stocks were down by less than 4% YTD; a testament to its inflation hedge and diversification benefits.

Infrastructure stocks also boast an extensive and solid performance track record versus the broad market on a longer term. Referencing to Figure 6, over the past 15 years, annualized total return of global listed infrastructure stocks significantly outstripped that of global bonds while only slightly trailing behind that of global equities on a 3-year, 5-year and 10-year basis; In fact, on a 15-year time horizon, global listed infrastructure has outperformed global equities.

Figure 6: Year-to-date and Annualized Total Return

Source: Bloomberg, Data as of 30 Jun 2022. Global bonds represented by the Bloomberg Global Aggregate Bond Index; Global equities represented by the MSCI All Country World Gross Total Return USD Index; Global listed infrastructure represented by the FTSE Global Core Infrastructure 50/50 Total Return USD Index. Past performance is no guarantee of future results.

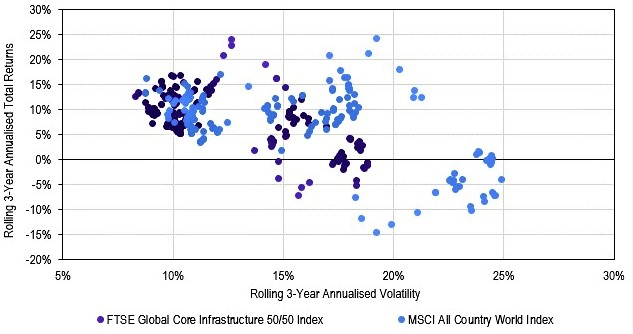

While higher returns are usually associated with higher risks, this is not the case for global listed infrastructure stocks. From Figure 7, it is evident that global listed infrastructure stocks are well placed for rolling returns on the top left of the chart i.e. almost comparable returns but lower volatility compared to global equities.

Figure 7: Rolling 3-year Annualized Volatility vs Rolling 3-year Annualized Total Return

Infrastructure stocks generate almost comparable returns to global equities but with less volatility.

Time period: 31 December 2008 – 31 May 2022

Source: Bloomberg, Data as of 31 May 2022

In terms of downside risk over the past one-year, global listed infrastructure is also a clear winner, as seen in Figure 8. It has the smallest maximum drawdown in the last one-year, which is the maximum observed loss from peak to trough.

Figure 8: 1-year Maximum Drawdown

Source: Bloomberg, Data as of 30 Jun 2022

What are the risks involved?

Besides the standard operational risks, listed infrastructure companies also have to manage and navigate specific operating conditions or constraints that are imposed directly by regulators. These return drivers and risks are fairly unique and somewhat different from most other equity sectors where the regulator may not play such a conspicuous role. As a result, the value of listed infrastructure shares may be negatively affected by economic or regulatory occurrences affecting their industries.

Final Words

Global infrastructure is a growing asset class that may appeal to investors seeking investment attributes such as a high yield relative to many other asset classes, fairly predictable cash flow growth and portfolio diversification.

With concerns around rising inflation and higher interest rates, global listed infrastructure assets can be a valuable addition to any well-diversified portfolio today by adding some much-needed predictability and stability – a place worth considering as a hideout from the current market turmoil.

Appendix 6

– Regulated Assets: Regulated and contracted utilities companies, such as water, electricity, and gas transmission and distribution, tend to be more defensive in nature due to its relatively low exposure to the vagaries of the economic cycle – after all, you still need to turn on the lights during a recession.

These assets tend to enjoy higher income potential. The regulator largely determines the revenues these companies are allowed to earn on their assets, which leads to a relatively stable cash flow profile over time.

Demand for these assets are typically stable and price increases are often linked to inflation. Long-term valuations are also relatively immune to changes in bond yields.

– User Pays Assets: User-pay assets, such as roads, rails, ports, airports and telecommunication towers, offer higher capital growth potential but with relatively lower income. Here, prices of essential services are generally set by long-dated contracts. Pricing contracts tend to incorporate a range of pass-through mechanisms where prices can be adjusted, either fully or partially, to short term movements in inflation.

As prices are often fixed, the company takes on usage volume risk, where its revenue is broadly determined by the number of people who use these assets. The nature of these long-dated contracts allows companies to effectively pass through the effects of inflation to the end users, thereby keeping the value of earnings in real terms relatively stable.

These physical assets move people, goods and services throughout an economy and as such, demand tends to grow as the population expands and the economy matures, increasing the scope for robust capital gains.

6. ”Listed Infrastructure: Defensive with a touch of growth” by Franklin Templeton, December 2021

About the writer

A globetrotter at heart, Winnie did not stop being one even after becoming a mother of 2; in fact, her children are her greatest travel partners! During her free time, besides planning for her next vacation, Winnie also enjoys listening to Maroon 5 and Ed Sheeran going on quiet drives, spending time with her family and friends, and watching football. One of her biggest moments as an Arsenal fan was watching the team play from the stands at the Emirates Stadium.

Disclaimers:

This article is for general information only and it does not constitute an offer, recommendation or solicitation of an offer to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments.

This article has not been prepared for any particular person or class of persons and does not constitute and should not be construed as investment advice or an investment recommendation. It has been prepared without regard to the specific investment objectives, financial situation or particular needs of any person or class of persons. You should seek advice from a licensed or an exempt financial adviser on the suitability of a product for you, taking into account these factors before making a commitment to purchase any product or invest in an investment. In the event that you choose not to seek advice from a licensed or an exempt financial adviser, you should carefully consider whether the product or service described herein is suitable for you. You are fully responsible for your investment decision, including whether the investment is suitable for you. The products/services involved are not principal-protected and you may lose all or part of your original investment amount. Standard Chartered Bank (Singapore) Limited will not accept any responsibility or liability of any kind, with respect to the accuracy or completeness of information in this article.

This document is being distributed for general information only and is subject to the relevant disclaimers available at https:// www. sc. com/en/regulatorydisclosures/#market-commentary-disclaimer. It is not and does not constitute research material, independent research, an offer, recommendation or solicitation to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments. This document is for general evaluation only. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person or class of persons and it has not been prepared for any particular person or class of persons. You should not rely on any contents of this document in making any investment decisions. Before making any investment, you should carefully read the relevant offering documents and seek independent legal, tax and regulatory advice. In particular, we recommend you to seek advice regarding the suitability of the investment product, taking into account your specific investment objectives, financial situation or particular needs, before you make a commitment to purchase the investment product. Opinions, projections and estimates are solely those of SCB at the date of this document and subject to change without notice. Past performance is not indicative of future results and no representation or warranty is made regarding future performance. Any forecast contained herein as to likely future movements in rates or prices or likely future events or occurrences constitutes an opinion only and is not indicative of actual future movements in rates or prices or actual future events or occurrences (as the case may be). This document must not be forwarded or otherwise made available to any other person without the express written consent of the Standard Chartered Group (as defined below). Standard Chartered Bank is incorporated in England with limited liability by Royal Charter 1853 Reference Number ZC18. The Principal Office of the Company is situated in England at 1 Basinghall Avenue, London, EC2V 5DD. Standard Chartered Bank is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and Prudential Regulation Authority. Standard Chartered PLC, the ultimate parent company of Standard Chartered Bank, together with its subsidiaries and affiliates (including each branch or representative office), form the Standard Chartered Group. Standard Chartered Private Bank is the private banking division of Standard Chartered. Private banking activities may be carried out internationally by different legal entities and affiliates within the Standard Chartered Group (each an “SC Group Entity”) according to local regulatory requirements. Not all products and services are provided by all branches, subsidiaries and affiliates within the Standard Chartered Group.

Market Abuse Regulation (MAR) Disclaimer Banking activities may be carried out internationally by different branches, subsidiaries and affiliates within the Standard Chartered Group according to local regulatory requirements. Opinions may contain outright “buy”, “sell”, “hold” or other opinions. The time horizon of this opinion is dependent on prevailing market conditions and there is no planned frequency for updates to the opinion. This opinion is not independent of Standard Chartered Group’s trading strategies or positions. Standard Chartered Group and/or its affiliates or its respective officers, directors, employee benefit programmes or employees, including persons involved in the preparation or issuance of this document may at any time, to the extent permitted by applicable law and/or regulation, be long or short any securities or financial instruments referred to in this document or have material interest in any such securities or related investments. Therefore, it is possible, and you should assume, that Standard Chartered Group has a material interest in one or more of the financial instruments mentioned herein. Please refer to https:// www .sc. com/en/banking-services/market-disclaimer.html for more detailed disclosures, including past opinions/ recommendations in the last 12 months and conflict of interests, as well as disclaimers. A covering strategist may have a financial interest in the debt or equity securities of this company/issuer. This document must not be forwarded or otherwise made available to any other person without the express written consent of Standard Chartered Group.

Deposit Insurance Scheme

Singapore dollar deposits of non-bank depositors are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law. For clarity, these investment products are not deposits and do not qualify as an insured deposit under the Singapore Deposit Insurance and Policy Owners’ Protection Schemes Act 2011. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured.