This is to inform that by clicking on the hyperlink, you will be

leaving

sc.com/sg

and entering a website operated by other parties.

Such links are only provided on our website for the convenience of

the Client and Standard Chartered Bank does not control or endorse

such websites, and is not responsible for their contents.

The use of such website is also subject to the terms of use and

other terms and guidelines, if any, contained within each such

website. In the event that any of the terms contained herein

conflict with the terms of use or other terms and guidelines

contained within any such website, then the terms of use and other

terms and guidelines for such website shall prevail.

Jamie Wong, Director, Team Head Investment Advisory

This article is an education piece about investment outlook in China. For informational purposes only.

Given the recent interventions by the China policy makers, some people are wondering whether China is becoming an uninvestable market. But is it true? While it may be extremely volatile, I believe China remains a market which still presents immense long-term opportunities. A view which is echoed by Howard Marks, co-founder of distressed asset manager Oaktree Capital Management, who said “compared with the US, Europe and Japan, I think of China as an economic adolescent … tempestuous and volatile but its best decades are ahead1”. I could not agree more. Investing in China is not for the short-term, and one needs to have a longer-term view and investment horizon to participate in its continued evolution of its economy.

It is easy to forget that while China is now the world’s second largest economy after recording immense growth over the past decades, it is still in the development process and remains an emerging market with all its associated risks and volatility. And China’s financial markets and business operating environment will remain volatile as China continues to restructure its economic model for the next stage of development, one where the old growth model based on resource intensive and low labour costs manufacturing will be replaced with a shift towards higher-end manufacturing and higher quality services, with stronger focus on consumption rather than investments. Given that current model has been in place over a few decades, obviously there will be pain associated the change. As the proverb says, “no pain, no gain”, this transition will lead China towards a developed nation status with more sustainable growth.

“Common Prosperity”

To accelerate this shift, China aggressively embarked on its “common prosperity” agenda for its 14th Five-Year Plan with heavy regulatory action on multiple sectors, which has unsettled many foreign investors and prompted many to flee the market. This exodus by foreign investors led to sharp declines in China’s capital markets, leading to some to call China as uninvestable. Now “common prosperity” is not new. It was first coined in the 1950s by Mao Zedong and reiterated in the 1980s by Deng Xiaoping, as communist China sought to build a stronger economy. To achieve this, Deng Xiaoping believed that by allowing some people and regions to get rich first would accelerate economic growth and eventually achieve the goal of common prosperity2. This approach to incorporate elements of capitalism worked well since, but China has now reached a stage where the widening income and wealth gap is leading to deepening inequality, a threat to the future growth and stability of both the economy and society.

While the trillions lost in capital markets may appear to be resulting in “common poverty”, one needs to understand it is necessary to maintain key long-term structural growth trends such as the emerging middle-class which in a country with a massive population size of 1.4 billion, presents tremendous potential and opportunity. To “unlock” this huge consumption potential, China needs to raise the living standards of its people and reduce income inequality. No surprise that early policy actions targeted areas which are important to the middle-income – education, healthcare, and housing.

More equality drives more growth

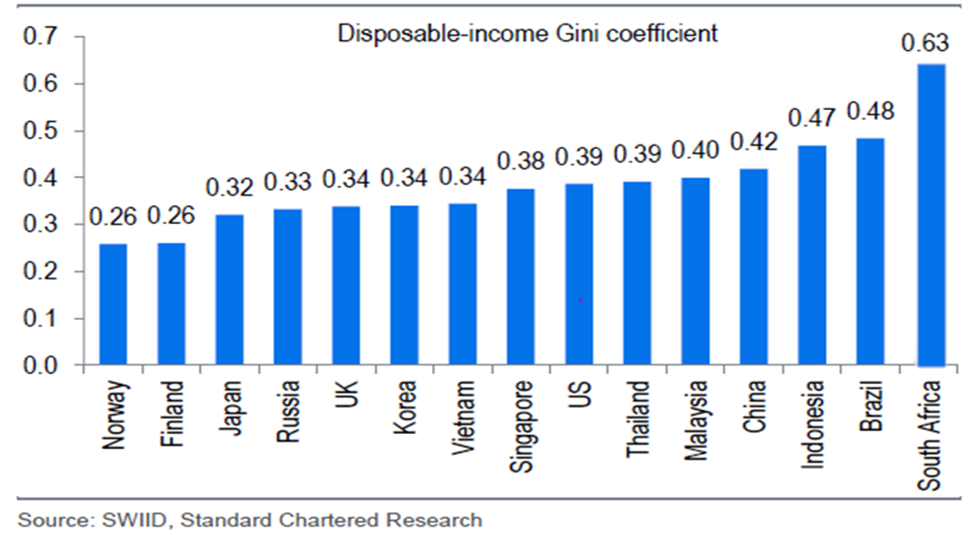

“Common prosperity” is highly important to China as its economy moves from a period of high growth to slower but more high quality and sustainable growth. To achieve the latter, China needs to address its rising-income inequality as many studies show that it damages long-term economic growth. An empirical study of 31 OECD (Organisation for Economic Co-operation and Development) countries from 1970-2010 found that rise in income inequality over 1985-2005 cut 4.7 percentage point of cumulative growth over the 1990-2010 period3, while a decline in income inequality by 1 Gini coefficient point (measure of income or wealth inequality) contributes to a 0.88 percentage point rise in cumulative growth in the following five years4. From a global perspective, China’s income inequality is higher than that of most developed or developing Asian economies (Refer to Figure 1), and its own estimate of their income Gini coefficient was even higher at 0.47 in 2019. For a US$18.1 trillion economy5, every percentage point counts as it can amount in the billions.

Figure 1: Disposable-Income Gini Coefficient by Country

Long-term growth with cheap valuations

If one can look past the short-term pain, there is immense long-term growth potential in China’s evolving economy. Not only is China addressing income inequality to continue growing its middle-class and bolster consumption, focus and resources are also being channeled into new growth areas such as renewable energy, green manufacturing, healthcare, software, semiconductors, artificial intelligence, and new energy vehicles. Even the technology sector which bore the brunt of regulatory crackdowns, remains a key focus area in China’s 14th Five Year Plan6 as government plans to raise the proportion of the added value of the “digital economy” in its GDP to 10% in 2025, up from 7.8% in 2020. That 2.2% difference on a GDP which is US$18.1 trillion in size equates to an additional US$400 billion!

Following the extremely sharp declines over the past year, MSCI China is now trading at historically cheap levels at between 8-10x 12M forward PE multiples (Refer to Figure 2), despite Peoples Bank of China embarking on an easier monetary policy, and 7IMF forecasting +4.8% growth in GDP for 2022. This compares against 19x for S&P, with the US Federal Reserve committed to and initiating an aggressive tightening policy, and 7IMF forecasting +4% growth in GDP for 2022.

Figure 2: Forward P/E of MSCI China vs S&P 500

Source: Bloomberg

Cost of missing out could be substantial

If history is of any guide, the worst for China could soon be behind us as it enters a period of consolidation before the next stage higher (Refer to Figure 3). This may be a generational opportunity for investors with a longer-term view, and the cost of missing out could possibly be substantial. Highlighted by our venerable former founder and Prime Minister Lee Kuan Yew in his timeless wisdom – “If you do not know history, you think short-term. If you know history, you think medium and long-term” (see “Lee Kuan Yew: The Grand Master’s Insights on China, the United States, and the World”). Growing pains is an inevitable process of progress, one should look forward towards the future. Remember, it is always darkest before dawn.

Figure 3: MSCI China entering consolidation phase

Source: Bloomberg

About the writer

Prior to venturing into wealth advisory, Jamie was an equity sales trader for two decades covering global financial markets and servicing both institutional and retail clients. Having seen many market cycles, booms and busts, a key lesson that Jamie learnt is to never underestimate human ingenuity and its ability to adapt, improvise and overcome. Jamie hopes he can help to free the mind of others on the complexities and inter-connectedness of the financial markets, just like Morpheus in the “Matrix” movies.

This article is for general information only and it does not constitute an offer, recommendation or solicitation of an offer to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments.

This article has not been prepared for any particular person or class of persons and does not constitute and should not be construed as investment advice or an investment recommendation. It has been prepared without regard to the specific investment objectives, financial situation or particular needs of any person or class of persons. You should seek advice from a licensed or an exempt financial adviser on the suitability of a product for you, taking into account these factors before making a commitment to purchase any product or invest in an investment. In the event that you choose not to seek advice from a licensed or an exempt financial adviser, you should carefully consider whether the product or service described herein is suitable for you. You are fully responsible for your investment decision, including whether the investment is suitable for you. The products/services involved are not principal-protected and you may lose all or part of your original investment amount. Standard Chartered Bank (Singapore) Limited will not accept any responsibility or liability of any kind, with respect to the accuracy or completeness of information in this article.

This document is being distributed for general information only and is subject to the relevant disclaimers available here. It is not and does not constitute research material, independent research, an offer, recommendation or solicitation to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments. This document is for general evaluation only. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person or class of persons and it has not been prepared for any particular person or class of persons. You should not rely on any contents of this document in making any investment decisions. Before making any investment, you should carefully read the relevant offering documents and seek independent legal, tax and regulatory advice. In particular, we recommend you to seek advice regarding the suitability of the investment product, taking into account your specific investment objectives, financial situation or particular needs, before you make a commitment to purchase the investment product. Opinions, projections and estimates are solely those of SCB at the date of this document and subject to change without notice. Past performance is not indicative of future results and no representation or warranty is made regarding future performance. Any forecast contained herein as to likely future movements in rates or prices or likely future events or occurrences constitutes an opinion only and is not indicative of actual future movements in rates or prices or actual future events or occurrences (as the case may be). This document must not be forwarded or otherwise made available to any other person without the express written consent of the Standard Chartered Group (as defined below). Standard Chartered Bank is incorporated in England with limited liability by Royal Charter 1853 Reference Number ZC18. The Principal Office of the Company is situated in England at 1 Basinghall Avenue, London, EC2V 5DD. Standard Chartered Bank is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and Prudential Regulation Authority. Standard Chartered PLC, the ultimate parent company of Standard Chartered Bank, together with its subsidiaries and affiliates (including each branch or representative office), form the Standard Chartered Group. Standard Chartered Private Bank is the private banking division of Standard Chartered. Private banking activities may be carried out internationally by different legal entities and affiliates within the Standard Chartered Group (each an “SC Group Entity”) according to local regulatory requirements. Not all products and services are provided by all branches, subsidiaries and affiliates within the Standard Chartered Group.

Market Abuse Regulation (MAR) Disclaimer Banking activities may be carried out internationally by different branches, subsidiaries and affiliates within the Standard Chartered Group according to local regulatory requirements. Opinions may contain outright “buy”, “sell”, “hold” or other opinions. The time horizon of this opinion is dependent on prevailing market conditions and there is no planned frequency for updates to the opinion. This opinion is not independent of Standard Chartered Group’s trading strategies or positions. Standard Chartered Group and/or its affiliates or its respective officers, directors, employee benefit programmes or employees, including persons involved in the preparation or issuance of this document may at any time, to the extent permitted by applicable law and/or regulation, be long or short any securities or financial instruments referred to in this document or have material interest in any such securities or related investments. Therefore, it is possible, and you should assume, that Standard Chartered Group has a material interest in one or more of the financial instruments mentioned herein. Please refer to https:// www .sc. com/en/banking-services/market-disclaimer.html for more detailed disclosures, including past opinions/ recommendations in the last 12 months and conflict of interests, as well as disclaimers. A covering strategist may have a financial interest in the debt or equity securities of this company/issuer. This document must not be forwarded or otherwise made available to any other person without the express written consent of Standard Chartered Group.

Deposit Insurance Scheme

Singapore dollar deposits of non-bank depositors are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law. For clarity, these investment products are not deposits and do not qualify as an insured deposit under the Singapore Deposit Insurance and Policy Owners’ Protection Schemes Act 2011. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured.

This advertisement has not been reviewed by the Monetary Authority of Singapore.