This is to inform that by clicking on the hyperlink, you will be

leaving

sc.com/sg

and entering a website operated by other parties.

Such links are only provided on our website for the convenience of

the Client and Standard Chartered Bank does not control or endorse

such websites, and is not responsible for their contents.

The use of such website is also subject to the terms of use and

other terms and guidelines, if any, contained within each such

website. In the event that any of the terms contained herein

conflict with the terms of use or other terms and guidelines

contained within any such website, then the terms of use and other

terms and guidelines for such website shall prevail.

The article is an educational piece about planning early for retirement. For informational purposes only.

This is a hands-on activity, and will need you to download a free TVM calculator from your app store.

Ask around and everyone will be able to tell you the typical “successful Singaporean” formula instilled in us since childhood. You graduate, get a job, get married, have a house, have children, pay for their education, retire – you get the picture. Above all, there is an ingrained need to build up a large cash buffer to feel safe.

But have you ever stopped to wonder what are you even doing this for, or why are you doing it?

Amassing wealth for wealth’s sake really doesn’t do much practical good for you unless you know what you are going to do with it. Here are five steps to make sure you are on the right track to retiring well:

Step 1: Visualize the end goal

It’s easy to fall into auto-pilot mode and forget about what you hope to achieve 10, 20 years down the road. As the saying goes, “Begin with an end in mind”, you should first ask yourself the following questions.

– What would a day in my retirement look like?

– How would I like to spend my time? (For example, caring for grandkids, taking up a course on MasterClass, gardening, playing golf with friends, cycling around Singapore, traveling with loved ones)

– What are some of the dreams I hope to realise?

Step 2: Get specific

Now it’s time to crunch some numbers and get specific.

Retirement expenses

Work out an estimation of how much you think you would be spending monthly after retiring. An easy hack is to just take stock of how much you are spending today, then, extrapolate it into the future with the ‘TVM calculator’ app that you have just downloaded.

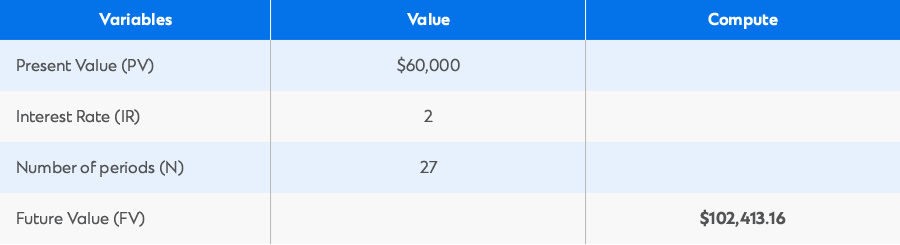

For example, if you are 38 this year with a personal monthly expenditure of $5,000, and plan to retire by 65 – find out how much your monthly expenses that would be 27 years later. Since a cup of kopi only cost $0.70 back in the 90s and today it is roughly $1.30, let’s assume an inflation rate of about 2%.[1]

Go to your TVM calculator and key in:

>> where $5000 is your monthly expenditure today, extrapolated forward 27 years , with an inflation of 2%. Click Future Value (FV) to see the result. Based on the above, your extrapolated expenses during retirement should work out to be $8,534.43. Therefore $102,413.16 would your extrapolated annual expenses

Life Expectancy

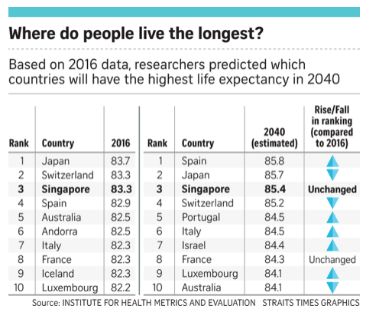

Did you know that life expectancy in Singapore is one of the highest in the world? (Source: Institute for Health Metrics and Evaluation)

Tip: make sure you plan for a longer-than-expected retirement!

According to these stats below (Graph 1), the average life expectancy in Singapore is estimated to be 85 years by 2040. So, let’s use that figure in our assumptions. This means that you would need to cater for 20 years of retirement ( age 65 – 85).

Graph 1: Countries with highest life expectancy in 2040

Step 3: Sum it all up

Now you’ve come to the important step. You will need to figure out exactly how much the required retirement lump sum is for you to kick start our retirement. Technically, you need to have amassed this figure by the expected retirement age.

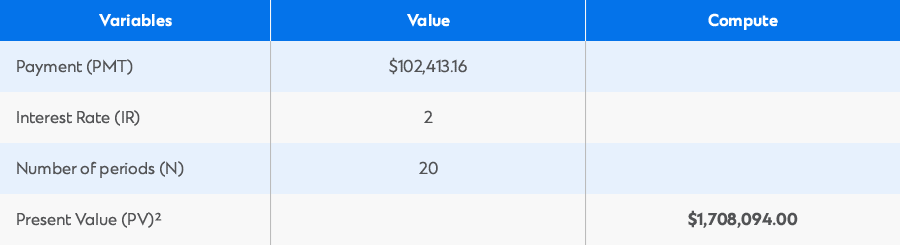

Going back to your TVM calculator, key in:

>> where $102,413.16 is the annual retirement income stream you hope to receive to sustain your standard of living over 20 years (65 – 85 years old), with an inflation rate of 2%. .Click Present Value (PV) to see the result. You should get $1,708,094.00, this would be the retirement lump sum required to kick start our retirement at age 65.

I know, this sounds like a huge and seemingly unattainable amount, but it’s better late than never.

You should get a Future Value of $1.27, which is close to the price of a cup of kopi at the kopitiam today

Step 4: Harness the power of compounding

There is hope! Even if today you have accumulated no known assets to your name today, you can still work towards the huge $1.7 million figure mentioned above.The magic is in the power of compounding.

In your TVM calculator, key in these values:

Click PMT to see the result.

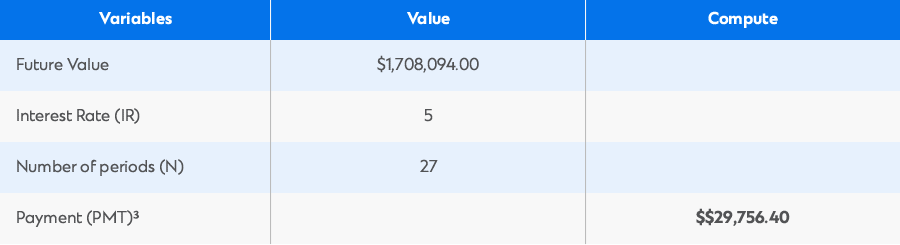

>>where $1,708,094 is the future retirement sum that we are working towards, 5% is the assumed rate of return on your portfolio, and 27 years is the time from now till your retirement age.

You should get $29,756.40. For simplicity, let’s just round this number up to $30,000.

Effectively, I’m saying that as long as you consistently invest$30,000 every year (or breaking it down, $2,500 each month), you should be able to hit your target of ~$1.7mil by retirement.

Tip: A ballpark figure to save and invest is about 25% of your gross monthly income each month. Instead of putting it aside just as cash savings, plough it into an investment portfolio that has a return of at least 5% p.a. As your income grows, you should likewise increase the regular amount that you can set aside.

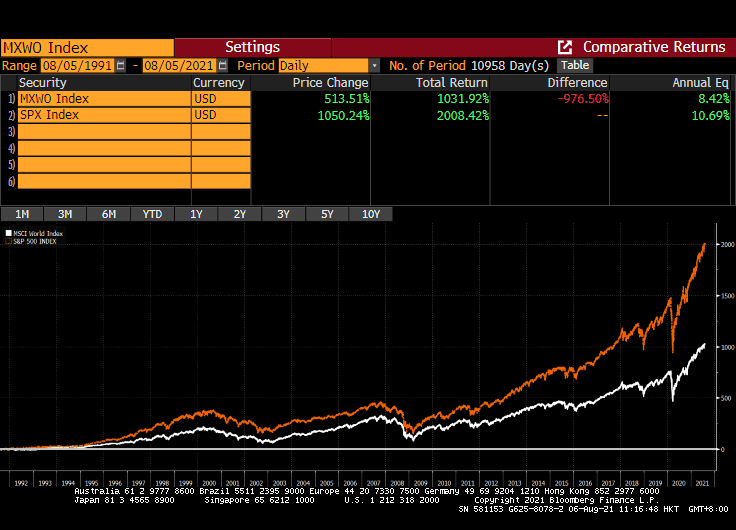

Over the past 30 years, the global equity stock market has grown annually by 8.42%pa (Graph 2). Assuming it continues to grow at this rate, ploughing steadily into a globally diversified equity portfolio should cover you all the way, and even more.

Graph 2: MSCI World Index (MXWO) vs. S&P 500 Index (SPX)

Source: Bloomberg

Step 5: Start now, don’t wait

There may be a million different reasons in your head telling you why you should wait it out, especially since the US and European equity markets are at an all-time high (ATH). As much as there are uncertainties and fears, let me also show you the opportunity cost of waiting.

Let’s say I start planning for my retirement at 40 instead of 38.

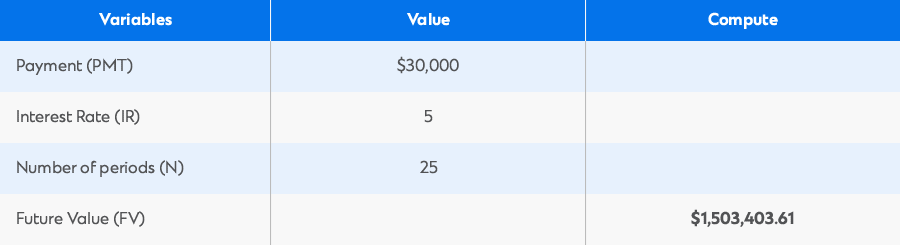

Going back to the TVM calculator, key in these values:

>>where $30,000 is the amount invested per year, 5% is the assumed rate of return of your portfolio, and 25 years is the time from 40 till retirement age of 65. Click FV4 to see the result.

You should get $1,503,403.61.

This means that just by waiting an additional two years (where the cash outlay for investment would have just been $60,000), the drop in the target sum turns out to be a whopping $204,690 ($1,708,094.00 – $1,503,403.61) lost in opportunity cost. And if you wait till you are 45 to start, the opportunity cost balloons to $667,362 ($1,708,094.00 – $1,041,577.55).

As the adage goes, “timein the market is better than timing the market”. Therefore, getting in as early as possible is the aim of the game here. If the ATH is stirring fear, activate a progressive investment plan as mentioned earlier (e.g. $2,500/month) so that you can plough into your portfolio in a disciplined way and effectively cope with the emotional (and oftentimes irrational) swings of the stock market.

Parting thoughts

My plan is predicated on the assumption that you invest into a well-diversified equity portfolio. These days, there are many great mutual funds and ETFs5 that can achieve just that. I also assume that once you plough in, you don’t meddle too much with it or try to time the market with multiple entries and exits.

For those who aren’t as risk loving as me, you could modify the above strategy by combining annuity plans together with some exposure into equity funds. Rightsizing the risk to your comfort level is of utmost importance, and never invest in anything you do not understand.

On the other hand, for those who are ahead of the curve and have already done some preliminary retirement planning: If you are now thinking about working on multiple other goals, please have a go at our recently launched

SC Goals Planner. It is a holistic planning tool that takes your family and your needs, wants, dreams and life events into account. I particularly like that in one glance, it immediately gives you a clear visualization of how your dreams and life events affect your financial standing.

Finally, planning for retirement is not solely a financial exercise. and I hope that reading this post spurs you on to think more holistically about other non-financial pursuits that would also bring you joy during your retirement years.

For me, my ideal retirement is leading an active and healthy lifestyle well into my sixties, perhaps going back to school to take up a degree in counselling and hosting sunset drinks for my friends on my balcony.

Profile

Cheryl is a (hard)working mom with 3 young kids, and happens to be a millennial. She enjoys converting difficult concepts into simple and bite-sized ideas that people can use. In her free time, you will find her nurturing (read: nagging) her 3 beautiful children towards following the Singapore dream (whatever that means). In this post-Covid world, she often daydreams about the next time she will get to hike in some faraway mountain where the weather is not eternally humid.

Footnotes

[1]You can check the inflation rate by keying these values into the TVM calculator:

Key in:

$0.70 in Present Value (PV)

2% in Interest Rate (IR)

30 years in the Period field (N) – I assumed time period from 1991 to 2021

You should get a Future Value of $1.27, which is close to the price of a cup of kopi at the kopitiam today

[2] If your TVM app has an option for BGN mode, use it for this calculation, i.e. receiving payments at the beginning of each period.

[3] If your TVM app has an option for BGN mode, use it for this calculation i.e. investing regularly at the beginning of each period.

[4] If your TVM app has an option for BGN mode, use it for this calculation i.e. investing regularly at the beginning of each period.

[5] An exchange traded fund (ETF) is a type of security that tracks an index, sector or commodity, which can be purchased or sold on a stock exchange the same way a regular stock can. A well-known example is SPD S&P 500 ETF (ticker code: SPY), which tracks the S&P 500 Index (i.e. The US Stock market).

Disclaimers

This article is for general information only and it does not constitute an offer, recommendation or solicitation of an offer to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments.

This article has not been prepared for any particular person or class of persons and does not constitute and should not be construed as investment advice or an investment recommendation. It has been prepared without regard to the specific investment objectives, financial situation or particular needs of any person or class of persons. You should seek advice from a licensed or an exempt financial adviser on the suitability of a product for you, taking into account these factors before making a commitment to purchase any product or invest in an investment. In the event that you choose not to seek advice from a licensed or an exempt financial adviser, you should carefully consider whether the product or service described herein is suitable for you. You are fully responsible for your investment decision, including whether the investment is suitable for you. The products/services involved are not principal-protected and you may lose all or part of your original investment amount. Standard Chartered Bank (Singapore) Limited will not accept any responsibility or liability of any kind, with respect to the accuracy or completeness of information in this article.

This document is being distributed for general information only and is subject to the relevant disclaimers available here. It is not and does not constitute research material, independent research, an offer, recommendation or solicitation to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments. This document is for general evaluation only. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person or class of persons and it has not been prepared for any particular person or class of persons. You should not rely on any contents of this document in making any investment decisions. Before making any investment, you should carefully read the relevant offering documents and seek independent legal, tax and regulatory advice. In particular, we recommend you to seek advice regarding the suitability of the investment product, taking into account your specific investment objectives, financial situation or particular needs, before you make a commitment to purchase the investment product. Opinions, projections and estimates are solely those of SCB at the date of this document and subject to change without notice. Past performance is not indicative of future results and no representation or warranty is made regarding future performance. Any forecast contained herein as to likely future movements in rates or prices or likely future events or occurrences constitutes an opinion only and is not indicative of actual future movements in rates or prices or actual future events or occurrences (as the case may be). This document must not be forwarded or otherwise made available to any other person without the express written consent of the Standard Chartered Group (as defined below). Standard Chartered Bank is incorporated in England with limited liability by Royal Charter 1853 Reference Number ZC18. The Principal Office of the Company is situated in England at 1 Basinghall Avenue, London, EC2V 5DD. Standard Chartered Bank is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and Prudential Regulation Authority. Standard Chartered PLC, the ultimate parent company of Standard Chartered Bank, together with its subsidiaries and affiliates (including each branch or representative office), form the Standard Chartered Group. Standard Chartered Private Bank is the private banking division of Standard Chartered. Private banking activities may be carried out internationally by different legal entities and affiliates within the Standard Chartered Group (each an “SC Group Entity”) according to local regulatory requirements. Not all products and services are provided by all branches, subsidiaries and affiliates within the Standard Chartered Group.

Market Abuse Regulation (MAR) Disclaimer Banking activities may be carried out internationally by different branches, subsidiaries and affiliates within the Standard Chartered Group according to local regulatory requirements. Opinions may contain outright “buy”, “sell”, “hold” or other opinions. The time horizon of this opinion is dependent on prevailing market conditions and there is no planned frequency for updates to the opinion. This opinion is not independent of Standard Chartered Group’s trading strategies or positions. Standard Chartered Group and/or its affiliates or its respective officers, directors, employee benefit programmes or employees, including persons involved in the preparation or issuance of this document may at any time, to the extent permitted by applicable law and/or regulation, be long or short any securities or financial instruments referred to in this document or have material interest in any such securities or related investments. Therefore, it is possible, and you should assume, that Standard Chartered Group has a material interest in one or more of the financial instruments mentioned herein. Please refer to https:// www .sc. com/en/banking-services/market-disclaimer.html for more detailed disclosures, including past opinions/ recommendations in the last 12 months and conflict of interests, as well as disclaimers. A covering strategist may have a financial interest in the debt or equity securities of this company/issuer. This document must not be forwarded or otherwise made available to any other person without the express written consent of Standard Chartered Group.

Deposit Insurance Scheme

Singapore dollar deposits of non-bank depositors are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law. For clarity, these investment products are not deposits and do not qualify as an insured deposit under the Singapore Deposit Insurance and Policy Owners’ Protection Schemes Act 2011. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured.

This advertisement has not been reviewed by the Monetary Authority of Singapore.