This is to inform that by clicking on the hyperlink, you will be

leaving

sc.com/sg

and entering a website operated by other parties.

Such links are only provided on our website for the convenience of

the Client and Standard Chartered Bank does not control or endorse

such websites, and is not responsible for their contents.

The use of such website is also subject to the terms of use and

other terms and guidelines, if any, contained within each such

website. In the event that any of the terms contained herein

conflict with the terms of use or other terms and guidelines

contained within any such website, then the terms of use and other

terms and guidelines for such website shall prevail.

Being accountable to broadening range of stakeholders

Key Highlights

– Effective governance is no longer just about protecting and benefiting shareholders, as institutional investors’ definition of stakeholders has broadened to include supply chains, members of society impacted by business activities and public-policy influencers, among others.

– Companies in highly regulated or publicly scrutinised industries such as utilities and consumer staples tend to have boards that are better equipped to oversee sustainability issues.

– Governance scores can add insight into the quality of high-yield corporate bonds.

In environmental, social and governance (ESG), the governance (G) aspect is the oldest, and has been an integral part of robust investment research for decades. But what is considered effective governance has evolved, and the speed of evolution has quickened as institutional investors’ definition of stakeholders continues to broaden beyond shareholders. While older forms of G focused on serving and protecting shareholders, the newer approaches stretch beyond basic dimensions related to financial and accounting misconduct as well as legal and regulatory non-compliance, such as transparency, corporate structures and ethics.

Reflecting the broader scope of G, RobecoSAM, an asset manager specialising in sustainability investing, has devised the economic dimension score, which evaluates eight groups of criteria. They include older concepts of corporate governance such as board structure and effectiveness, compensation, codes of conduct, corruption and bribery, and reporting on breaches. The newer governance evaluations include risk and crisis management; supply chain management; tax strategy; an ability to identify and report on the sources of long-term value creation; funding extended to organisations creating or influencing public policy, legislation and regulation; and business impact on societal issues which may not be reflected in financial accounting but could be priced in, in the future.

Although traditional financial accounting does not include these wider considerations, the Sustainability Accounting Standards Board (SASB), which is supported by investors representing US$72 trillion1 in assets under management, is encouraging companies to step in that direction. The SASB framework puts competitive behaviour, critical incident risk management, systemic risk management and management of the legal and regulatory environments into a “leadership and governance” pillar.

Investors are also aligning G with the 17 United Nations Sustainability Development Goals (SDGs), where governance issues include industry, innovation and infrastructure (Goal 9); peace, justice and strong institutions (Goal 16); and partnerships with public and private institutions (Goal 17). This broader scope for G has a similar rationale as it does for E and S, which we have discussed previously in our three-part series.

The various proponents of the wider ambit of governance may use differing terminology, but their aim is broadly similar: more effective risk management as well as value creation in an increasingly complex world. In other words, institutional investors are beginning to see it as the board of directors’ fiduciary duty to oversee sustainability risks and opportunities that can have a material impact on their companies’ financial and economic health.

Evolving at the speed of boards

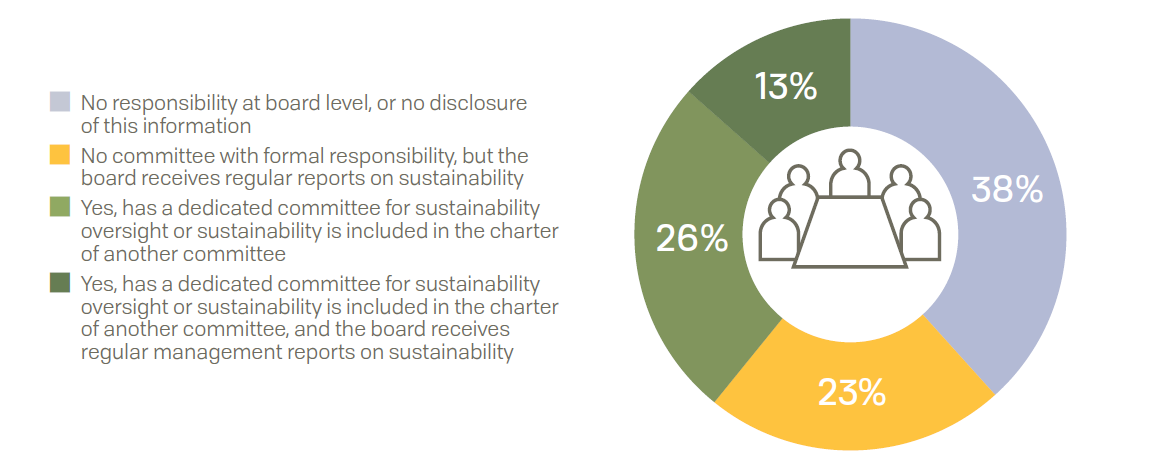

Companies are catching up with these evolving changes but perhaps not fast enough. Ceres, a sustainability organisation, studied 475 of the world’s biggest companies listed on the Forbes Global 2000. The results, which were published in May 2018, show that 62% of the companies say they have sustainability oversight at the board level.

However, only 13% have a dedicated sustainability committee or has incorporated sustainability as part of overall oversight as well as receiving regular sustainability reports from management. A deeper analysis shows that only 10% of these companies’ boards review most of the material sustainability issues brought to the table; while 63% do not conduct reviews at board meetings or do not disclose this information. One reason for the lack of board action could be the dearth of sustainability expertise on most boards, as the Ceres study found only 17% of companies have at least one board director with sustainability expertise or experience.

Figure 1: Companies with board-level responsibility for sustainability

Source: Ceres, May 2018.

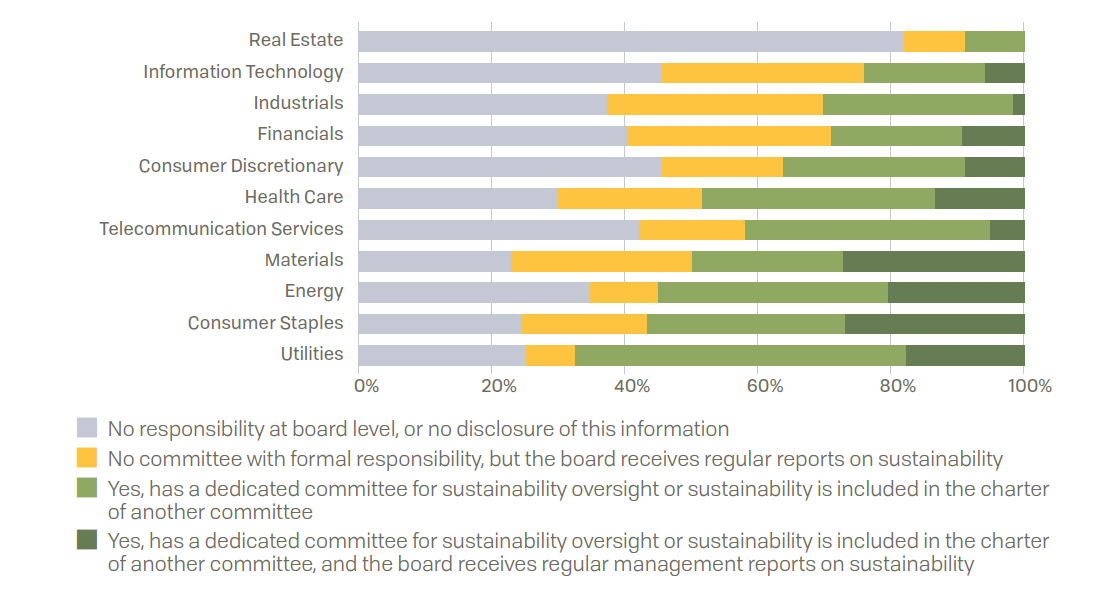

The level of board commitment and expertise varies from one sector to another. Sectors facing the greatest public, consumer or regulatory scrutiny such as utilities, consumer staples and materials tend to have more robust board oversight on sustainability, presumably because they face regulatory and reputational risks. For example, a third of utilities companies have at least one board director with expertise in climate change, renewable energy, environmental compliance and regulation, employee safety or other relevant areas.

Figure 2: Board-level responsibility for sustainability in various sectors (percentage of companies in each sector)

Source: Ceres, May 2018

At the management level, executives’ incentives to align with sustainability aren’t as robust as they sound, according to Ceres’ study. While 32% of companies said executive compensation is linked to sustainability outcomes, only 6% have explicit targets and disclosed them. The remaining 26% did not reveal the sustainability targets linked to compensation and 68% had no link between the two.

Ceres concluded that boards are often “ineffective” where sustainability is concerned because “too often board systems are still rudimentary and do not focus on material issues.” Given the link between sustainability and financial as well as investment performance, which we have explored in our previous articles on E and S, this could mean that companies with good sustainability track records are in a stronger competitive position.

For example, Sealed Air, the creator of the Bubble Wrap and other packaging as well as packaging equipment for a wide range of industries worldwide, has made a commitment to eradicate child labour, modern slavery and human trafficking from its vast supply chains. Suppliers representing 81% of Sealed Air’s expenditure in 2019 have committed to the company’s code of conduct, according to the latest sustainability report available.

Rothesay Life is one of the first 70-plus banks, investors and housing associations to adopt the Sustainability Standard for Social Housing (SRS) in the UK. The SRS contains 48 ESG criteria2, which include explanations on how the board manages organisational risks, with references to risk management frameworks, systems and mitigation of organisational risks.

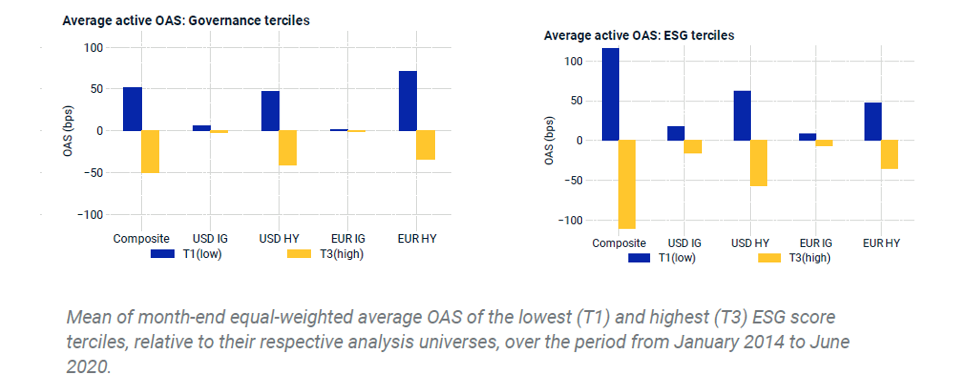

The link between G and high-yield credits

Governance scores, on top of traditional credit ratings, can help investors get a better grasp of the credit quality of high-yield bonds. This is demonstrated by MSCI’s study of a basket of investment-grade (IG) and high-yield (HY) credits denominated in US dollars (USD) and Euros (EUR). The study, published in November 2020, showed a risk spread of nearly 50 basis points between USD HY with high and low governance scores. The spread was even more pronounced for EUR HY.

However, governance scores provide far less additional information to the assessment of IG credits, which could be due to the fact that well-run companies tend to have fewer surprises awaiting investors.

Figure 3: Bond spreads between low and high governance scores

Source: MSCI, November 2020 Note1: OAS refers to option-adjusted spread, which is the difference in the yields of risk-free assets and the bond.

We would like to emphasise that ESG evaluations should be taken as a whole for proper analysis, and we are focusing on the G pillar in this article for the purposes of discussion.

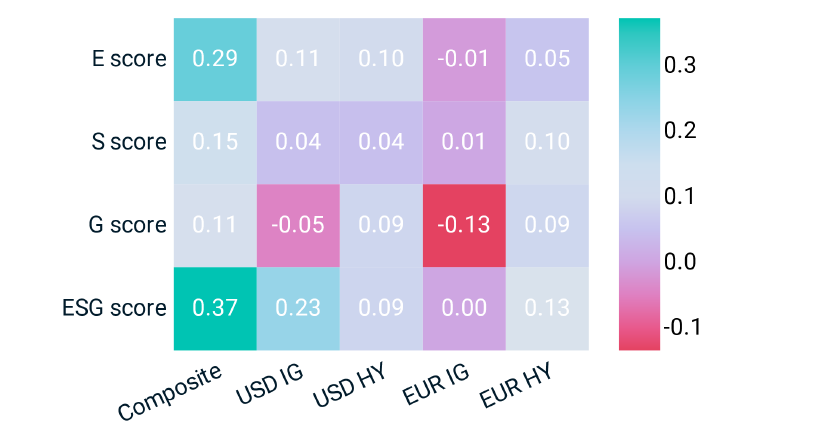

The MSCI findings also underscore that investors are more familiar with G than with E and S, possibly because G has been on the radar for much longer. This is borne by the fact that G scores provide less additional information to credit ratings (see Figure 4), unlike E scores and to a smaller extent, S scores.

Figure 4: Correlation between credit ratings and E, S and G ratings

Source: MSCI, November 2020 Note1: USD IG is USD investment-grade credit, USD HY is USD high-yield credit, EUR IG is EUR investment-grade credit, and EUR HY is EUR high-yield credit. Note2: Composite refers to the combination of USD and EUR investment-grade and high-yield credits used in the study.

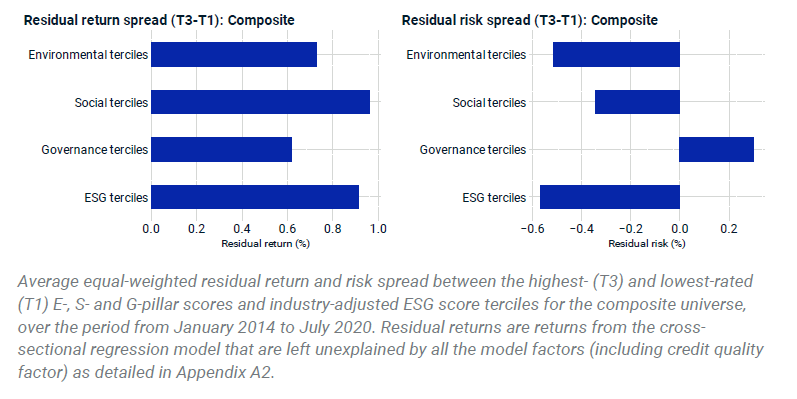

G’s weak correlation with credit scores is especially pronounced for residual risk (see Figure 5) and MSCI holds the view that this could be due to market participants understanding governance-related risks better and therefore have priced them in. In the future, however, as institutional investors apply a broadening set of expectations to G, this correlation may change.

Figure 5: Comparing residual returns and residual risk spreads between high and low E, S and G ratings

Source: MSCI, November 2020

This is the third in a series of articles on the E, S and G aspects of ESG investing. UOBAM became a signatory of the United Nations Principles for Responsible Investment (UNPRI) in January 2020.

2The Sustainability Reporting Standard for Social Housing: The Final Report of the ESG Social Housing Working Group, November 2020

Disclaimer

This article is for general information only and it does not constitute an offer, recommendation or solicitation of an offer to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments. This article has not been prepared for any particular person or class of persons and does not constitute and should not be construed as investment advice or an investment recommendation. It has been prepared without regard to the specific investment objectives, financial situation or particular needs of any person or class of persons. You should seek advice from a licensed or an exempt financial adviser on the suitability of a product for you, taking into account these factors before making a commitment to purchase any product or invest in an investment. In the event that you choose not to seek advice from a licensed or an exempt financial adviser, you should carefully consider whether the product or service described herein is suitable for you.

You are fully responsible for your investment decision, including whether the investment is suitable for you. The products/services involved are not principal-protected and you may lose all or part of your original investment amount. Standard Chartered Bank (Singapore) Limited will not accept any responsibility or liability of any kind, with respect to the accuracy or completeness of information in this article.

Deposit Insurance Scheme

Singapore dollar deposits of non-bank depositors are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law. For clarity, these investment products are not deposits and do not qualify as an insured deposit under the Singapore Deposit Insurance and Policy Owners’ Protection Schemes Act 2011. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured.

The information stated in this article is accurate as at the date of publication.