This is to inform that by clicking on the hyperlink, you will be

leaving

sc.com/sg

and entering a website operated by other parties.

Such links are only provided on our website for the convenience of

the Client and Standard Chartered Bank does not control or endorse

such websites, and is not responsible for their contents.

The use of such website is also subject to the terms of use and

other terms and guidelines, if any, contained within each such

website. In the event that any of the terms contained herein

conflict with the terms of use or other terms and guidelines

contained within any such website, then the terms of use and other

terms and guidelines for such website shall prevail.

Wealth BuildingForex, Gold & Alternative InvestmentsInvestment Strategies

20 November 2025 I 4 mins read

We started 2025 as U.S. Dollar bears and, thus far, the year has borne out as we expected. At its trough, the U.S. Dollar Index (the ‘DXY’) fell by over 10% since the start of the year before staging a modest rebound in recent months. This move has been driven by a combination of somewhat-mistaken ‘De-dollarisation’ fears and the more mundane driver of lower interest rates.

Is Dollar weakness now behind us, or is this only the start of a larger move lower? We are of the view that further weakness is yet ahead, albeit after a breather.

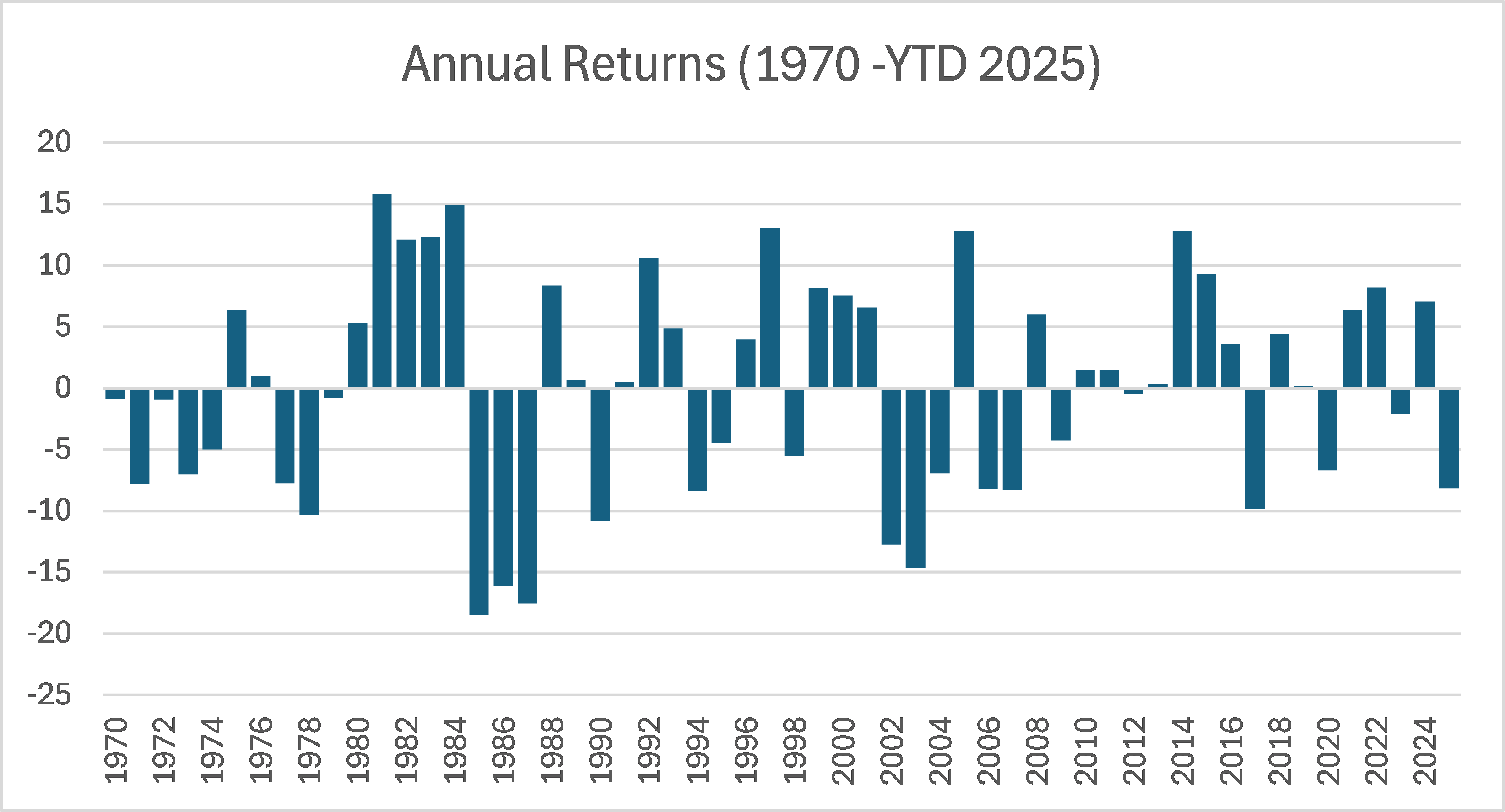

Putting the 2025 sell-off in perspective

The chart illustrates annual calendar year returns of the U.S. Dollar Index. What becomes clear is that while the 2025 fall has been among the steepest in recent years – this was at one point the largest calendar year falls in over 20 years – the extent of the weakness remains far from unusual. A significant share of down years have involved drawdowns of 10% or more. Prior to 2008, many years were also not isolated and were often followed by one or more subsequent years of similar-sized declines.

What’s driving the U.S. Dollar weakness?

In our view, there are three key drivers working against the U.S. Dollar today

Falling Fed interest rates and lower bond yields continue to erode the Dollar’s yield advantage. Prior to 2025, policy rates and bond yields outside the U.S. were largely falling , while Fed policy rates held firm. This year, that started to change as the Fed restarted its rate cut cycle. While the Dollar still holds a yield advantage in absolute terms, we expect this to continue dissipating as the Fed extends rate cuts.

De-dollarisation fears have raised concerns about whether investors should hold as much U.S. Dollars, or U.S. assets, as they have in recent years relative to non- U.S. assets. While we are sceptical of the argument that the U.S. Dollar’s dominance is set to vanish imminently, on the margin these fears can be sufficient to cause moderate currency weakness, especially at a time when non- U.S. equity assets arguably offer more value than U.S. markets on many traditional valuation metrics.

A backdrop of elevated valuation makes the U.S. Dollar more sensitive than usual to negative news. Common measures of currency market valuation include purchasing power parity or real effective exchange rates. Across most measures, the U.S. Dollar looks expensive. While currency valuations tend to normalise only over multi-year horizons, we believe this sets up the U.S. Dollar for further downside, especially given other catalysts are increasingly present.

History rhymes

Considering these drivers against the perspective of the Dollar’s historical moves means we remain comfortable with our view that further U.S. Dollar weakness is ahead of us. The experience of the mid-1980s or early 2000s involved cumulative multi-year weakness totalling more than 20% when catalysts were in place. While the current cycle’s USD downside could be more moderate, directionally the combination of a historical experience and our view on the major drivers mean USD weakness likely has further go. We do not expect this to occur in a straight line – indeed we may very well see a pause or a rebound higher going into end-2025 – but this is unlikely to stand in the way of the long-term trend.

When putting this to work in investment portfolios, our view of a weaker USD should not be limited to currency markets alone. Indeed, this year we have often pointed out that weak USD periods historically coincided with (i) positive returns in risky assets like equities, and (ii) the relative outperformance of non- U.S. markets. In particular, Emerging Markets have been key beneficiaries of a weak U.S. Dollar through history. This is one key reason why we currently prefer Asia ex-Japan equities and Emerging Market local currency bonds. A temporary Dollar rebound would only create an opportunity to build exposure.

Your feedback is valuable to us. Did you find this article helpful?

Disclaimer

This article is for general information only and it does not constitute an offer, recommendation or solicitation of an offer to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments. This article has not been prepared for any particular person or class of persons and does not constitute and should not be construed as investment advice or an investment recommendation. It has been prepared without regard to the specific investment objectives, financial situation or particular needs of any person or class of persons. You should seek advice from a licensed or an exempt financial adviser on the suitability of a product for you, taking into account these factors before making a commitment to purchase any product or invest in an investment. In the event that you choose not to seek advice from a licensed or an exempt financial adviser, you should carefully consider whether the product or service described herein is suitable for you.

You are fully responsible for your investment decision, including whether the investment is suitable for you. The products/services involved are not principal-protected and you may lose all or part of your original investment amount.

Standard Chartered Bank (Singapore) Limited will not accept any responsibility or liability of any kind, with respect to the accuracy or completeness of information in this article.

Deposit Insurance Scheme

Singapore dollar deposits of non-bank depositors are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law. For clarity, these investment products are not deposits and do not qualify as an insured deposit under the Singapore Deposit Insurance and Policy Owners’ Protection Schemes Act 2011. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured.

The information stated in this article is accurate as at the date of publication

Global Market Outlook H2 2025

Positioning for a weak dollar We are Overweight global equities. Policy easing worldwide, strong chances of a US soft landing and a weaker USD are supportive of risky assets. We favour diversified global equity exposure, within which we upgrade Asia ex-Japan equities to Overweight.