This is to inform that by clicking on the hyperlink, you will be

leaving

sc.com/sg

and entering a website operated by other parties.

Such links are only provided on our website for the convenience of

the Client and Standard Chartered Bank does not control or endorse

such websites, and is not responsible for their contents.

The use of such website is also subject to the terms of use and

other terms and guidelines, if any, contained within each such

website. In the event that any of the terms contained herein

conflict with the terms of use or other terms and guidelines

contained within any such website, then the terms of use and other

terms and guidelines for such website shall prevail.

The article is an educational piece about value and growth style investing. For informational purposes only.

Since the onset of the “Great Pandemic Crisis”, global central banks and governments have initiated massive stimulus packages to hasten the development of vaccines, economic recovery and liquidity. The result has led to several developed nations being able to re-open within months after the initial outbreak. Economy recovery seems to be steadily coming into fruition, and now, as the Federal Reserve (Fed) approaches a decision point regarding its accommodative stance, a debate on whether using a value or growth investing style is the best way forward for investors.

So, what is this debate about? Before I proceed, let me explain what a Growth and Value stock is:

– Growth equities are stocks that have high expected earnings, often using the measure of earnings-per-share (EPS) as well as high current and historical growth, as current and historical would imply a consistently high growth rate. Facebook Inc (FB) is an example of a Growth stock.

– Value equities on the other hand, are inexpensive stocks, based on price-to-book (P/B) and price-to-earnings (P/E) ratios. These ratios compare the stock price against the book value or earnings of the company. A low ratio would indicate that the stock is cheap in comparison to the value of its assets (book) and similarly if it was compared against its earnings. JPMorgan Chase & Co. (JPM), the largest bank in the United States and fifth largest bank globally in terms of total assets, is an example of a Value stock.

Behavioural differences: Growth vs Value

By and large, the two groups of equities behave differently in certain economic conditions:

– Sustained improvement in economic growth: Value equities tend to outperform Growth equities in periods of strong economic growth as they often closely track the economic cycle of expansion and recession. However, any resurgence in Covid-19 could dampen the pace of global recovery.

– Rising inflation expectations: Historically, Value equities’ performance is correlated with rising inflation expectations. The recent downtrend in inflation expectations has resulted in Value equities giving up some of its gains versus Growth equities.

– Higher bond yields: Rising yields benefit Value equities more than Growth equities as the former has a relatively higher existing cashflow than the latter, whose earnings are expected to come further in the future. From a technical lens, future cashflows are discounted more heavily as bond yields rise, resulting in a higher present value for Value equities than Growth equities.

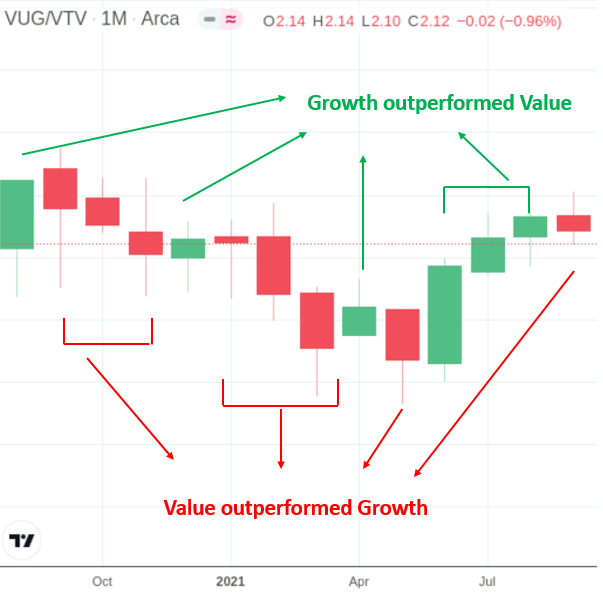

The constant evolution of these conditions has led to a battle between Growth and Value equities as they continuously vie for leadership even to date. In a span of 12 months from August 2020 to September 2021, US Growth and Value equities have traded a monthly leadership of eight times as seen in the chart below.

Growth vs. Value monthly leadership since August 2020

Source: TradingView.com Note: Chart shows the monthly ratio of Vanguard Growth ETF (VUG)/Vanguard Value ETF (VTV) from August 2020 to September 2021. Green bars represent Growth outperformance over Value whilst red bars represent Value Outperformance over Growth.

As we march into the mid-cycle period of a somewhat slower but sustainable economic growth, the once definite distinction between Growth and Value is beginning to blur. Instead of being torn between Growth or Value equities, perhaps we could marry both their aspects. To explain this concept in more detail, I will be referring to two well-known stocks purely for illustrative and educational purposes.

Finding value in Growth: Facebook Inc?

Taking FB as an example, a member in the S&P 500 Growth Index (SGX). It has a 12-month trailing (historical) and 12-month forward P/E ratio of *24.6 and *22.6, while the aggregate numbers of the SGX Growth Index are actually higher: *33.8 and *26.5 respectively. This possibly implies that the former is relatively undervalued as compared with the index.

Using a price to book (P/B) ratio also displays the same relative valuation. FB, which has a 12-month trailing and 12-month forward P/B ratio of *6.6 and *6.3 and SGX numbers of *10.6 and *9.6 respectively, implies that the former is relatively undervalued as compared with the latter. (A P/B ratio of 10 implies that investors are paying $10 for every dollar of the company’s asset, and is derived by dividing price per share with earnings per share. Intuitively, paying a lower P/B ratio would make more economic sense.)

In the chart below, you can see that the FB stock has consistently been delivering higher returns on the SGX and S&P500 Value Index (SVX) since the post-COVID recovery.

Source: Bloomberg *Data quoted above are extracted from Bloomberg

Finding growth in value: JPMorgan Chase & Co. (JPM)

So if you are able to find “value” in a high Growth stock like Facebook, could we also possibly find cheap stocks with high earnings potential?

Let’s use JPMorgan (JPM) as an example, a member in the S&P 500 Value Index (SVX). It has a 12-month forward earnings-per-share (EPS) growth rate of *57.9% per annum (p.a.) versus the SVX index rate of *27.8% p.a. Essentially, this largest bank in the US and fifth largest bank in the world, has delivered higher returns than both the SGX and SVX rates since the post-COVID recovery, as seen in the chart below. So yes, you can find high growth in Value stocks!

Source: Bloomberg *Data quoted above are extracted from Bloomberg

Make love, not war

So are Growth or Value equities the way to go? The examples above demonstrate that value and growth can potentially coexist with each other instead of being at the opposite ends of the spectrum. One method for investors to integrate both aspects into their portfolio would be to invest in a mutual fund managed under an investment philosophy that embraces both Growth and Value.

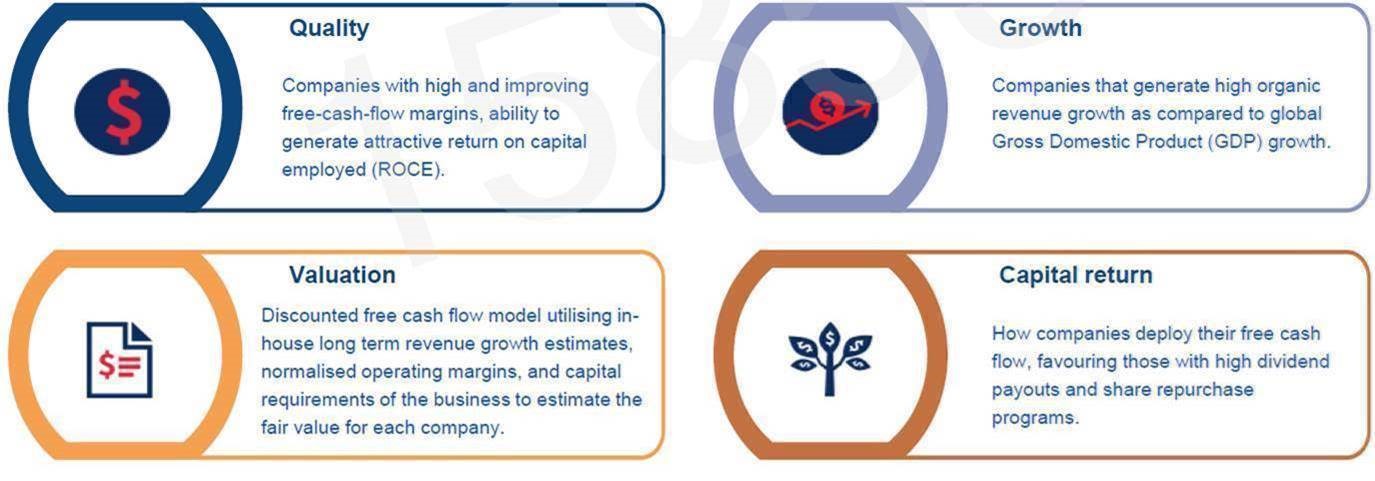

One such fund is the United Global Quality Growth Fund, which seeks four enduring attributes (see table below) when investing in companies, including growth and valuation. The above stocks which I mentioned earlier, Facebook Inc (FB) and JPMorgan Chase & Co. (JPM), are two of the fund’s top ten holdings as of 31 September 2021 per the United Global Quality Growth Fund October 2021 factsheet.

Source: Wellington Management, 30 June 2021

Besides focusing on growth or value, quality can be a key for differentiation amidst current rich equity valuations. Quality traits of a company can include clean balance sheets and high free cashflows, defensive characteristics to mitigate downside and the ability to reduce impact of market declines to benefit long-term investment performance. This can help serve as an additional lens when assessing the stock’s characteristics.

Other considerations

Just like any other forms of investments, United Global Quality Fund is still vulnerable to headwinds and the overall direction of the equity market. Few identifiable risks that come to mind are the potential mutation of Covid-19 virus which could lead to more potent variants beyond the efficacy of current vaccines thereby derailing the economy, earlier-than-expected rate hikes by the Federal Reserve resulting in slowdown in economic expansion, or company-specific issues faced by the underlying holdings of the fund, especially in relation to the top holdings such as Facebook and JPMorgan Chase & Co.

Written by Kelvin Lee, Senior Investment Advisor at Standard Chartered Wealth Management.

About the writer:

Kelvin started his career as an Equity Analyst before moving on to advisory roles for both retail and institutional portfolios. With a strong background in technical analysis, Kelvin sees Fibonacci lines, Elliot Waves and chart patterns above his bed, à la Beth Harmon in the Queen’s Gambit. He also enjoys culinary movies, such as “Chef” and “Julie & Julia”, as they delve into the neuroticism of ideas and end in the satisfaction of creating something beautiful, put together with simple, unassuming ingredients, somewhat like working out an investment portfolio. When he’s not obsessing about the financial markets, Kelvin appreciates quality time with friends and family over a game of darts.

Disclaimer

This article is for general information only and it does not constitute an offer, recommendation or solicitation of an offer to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments.

This article has not been prepared for any particular person or class of persons and does not constitute and should not be construed as investment advice or an investment recommendation. It has been prepared without regard to the specific investment objectives, financial situation or particular needs of any person or class of persons. You should seek advice from a licensed or an exempt financial adviser on the suitability of a product for you, taking into account these factors before making a commitment to purchase any product or invest in an investment. In the event that you choose not to seek advice from a licensed or an exempt financial adviser, you should carefully consider whether the product or service described herein is suitable for you. You are fully responsible for your investment decision, including whether the investment is suitable for you. The products/services involved are not principal-protected and you may lose all or part of your original investment amount. Standard Chartered Bank (Singapore) Limited will not accept any responsibility or liability of any kind, with respect to the accuracy or completeness of information in this article.

This document is being distributed for general information only and is subject to the relevant disclaimers available at https:// www. sc. com/en/regulatorydisclosures/#market-commentary-disclaimer. It is not and does not constitute research material, independent research, an offer, recommendation or solicitation to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments. This document is for general evaluation only. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person or class of persons and it has not been prepared for any particular person or class of persons. You should not rely on any contents of this document in making any investment decisions. Before making any investment, you should carefully read the relevant offering documents and seek independent legal, tax and regulatory advice. In particular, we recommend you to seek advice regarding the suitability of the investment product, taking into account your specific investment objectives, financial situation or particular needs, before you make a commitment to purchase the investment product. Opinions, projections and estimates are solely those of SCB at the date of this document and subject to change without notice. Past performance is not indicative of future results and no representation or warranty is made regarding future performance. Any forecast contained herein as to likely future movements in rates or prices or likely future events or occurrences constitutes an opinion only and is not indicative of actual future movements in rates or prices or actual future events or occurrences (as the case may be). This document must not be forwarded or otherwise made available to any other person without the express written consent of the Standard Chartered Group (as defined below). Standard Chartered Bank is incorporated in England with limited liability by Royal Charter 1853 Reference Number ZC18. The Principal Office of the Company is situated in England at 1 Basinghall Avenue, London, EC2V 5DD. Standard Chartered Bank is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and Prudential Regulation Authority. Standard Chartered PLC, the ultimate parent company of Standard Chartered Bank, together with its subsidiaries and affiliates (including each branch or representative office), form the Standard Chartered Group. Standard Chartered Private Bank is the private banking division of Standard Chartered. Private banking activities may be carried out internationally by different legal entities and affiliates within the Standard Chartered Group (each an “SC Group Entity”) according to local regulatory requirements. Not all products and services are provided by all branches, subsidiaries and affiliates within the Standard Chartered Group.

Market Abuse Regulation (MAR) Disclaimer Banking activities may be carried out internationally by different branches, subsidiaries and affiliates within the Standard Chartered Group according to local regulatory requirements. Opinions may contain outright “buy”, “sell”, “hold” or other opinions. The time horizon of this opinion is dependent on prevailing market conditions and there is no planned frequency for updates to the opinion. This opinion is not independent of Standard Chartered Group’s trading strategies or positions. Standard Chartered Group and/or its affiliates or its respective officers, directors, employee benefit programmes or employees, including persons involved in the preparation or issuance of this document may at any time, to the extent permitted by applicable law and/or regulation, be long or short any securities or financial instruments referred to in this document or have material interest in any such securities or related investments. Therefore, it is possible, and you should assume, that Standard Chartered Group has a material interest in one or more of the financial instruments mentioned herein. Please refer to https:// www .sc. com/en/banking-services/market-disclaimer.html for more detailed disclosures, including past opinions/ recommendations in the last 12 months and conflict of interests, as well as disclaimers. A covering strategist may have a financial interest in the debt or equity securities of this company/issuer. This document must not be forwarded or otherwise made available to any other person without the express written consent of Standard Chartered Group.

Deposit Insurance Scheme

Singapore dollar deposits of non-bank depositors are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law. For clarity, these investment products are not deposits and do not qualify as an insured deposit under the Singapore Deposit Insurance and Policy Owners’ Protection Schemes Act 2011. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured.

This advertisement has not been reviewed by the Monetary Authority of Singapore.