This is to inform that by clicking on the hyperlink, you will be

leaving

sc.com/sg

and entering a website operated by other parties.

Such links are only provided on our website for the convenience of

the Client and Standard Chartered Bank does not control or endorse

such websites, and is not responsible for their contents.

The use of such website is also subject to the terms of use and

other terms and guidelines, if any, contained within each such

website. In the event that any of the terms contained herein

conflict with the terms of use or other terms and guidelines

contained within any such website, then the terms of use and other

terms and guidelines for such website shall prevail.

Improve your finances through simple financial fitness

Improve your finances through simple financial fitness

Many life-changing money habits are built over time, from saving to investing to budgeting. You’ve probably got it all under control; still, it’s beneficial to take stock regularly, and ask yourself: “How can my process be tweaked so I can reach my financial goals faster?”

Regardless of your income, financial past or financial management know-how, you can empower yourself by taking steps to refine your financial health. If you haven’t paid much attention to strengthening your financial health, it’s always a great time to start!

Use our five-step guide as a refresher or a starter.

#1 Know yourself financially

No matter what your financial state is, it’s always beneficial to take a long, hard look at within yourself, and figure out your relationship with money and how you approach it, so you can nail down the bad practices.

– Money Vigilance – which is when you’re alert and watchful with money. This is the belief we should work towards.

– Money Avoidance – convincing yourself money isn’t important, so you don’t think about it.

– Money Status – equating self-worth with net worth, which may lead to extravagant displays of wealth

– Money Worship – thinking that having more money will banish your problems

Good financial health boils down to this: If you sweep aside the emotional aspect of money management, the practical solutions may never work.

#2 Create a budget

A structured budget is your north star that helps keep your eye on the prize. It forces you to lay out your financial goals, save cash, and monitor your progress. Turning your dreams into reality is what it does. Imagine if you just drifted through life buying everything you felt like; how would you ever save up enough for a down payment on that swanky condominium unit you’ve been yearning for or a two-week vacation to Japan?

If you’d like to get started without too much fuss, the 50/30/20 method is a straightforward and easy. It is a framework that breaks down 100% of your income into three categories: needs (essentials), wants (non-essentials) and savings (financial goals), respectively. Setting up a 50/30/20 budget will help you discover where your money is going.

‘Needs’ will cover things you cannot live without and bills you cannot escape paying. Mortgage payments, groceries, insurance, healthcare, and utilities drop here.

Extras like a Disney+ subscription, dining out, and that extra bag to add to your collection come under ‘wants’. This category is also known as personal or discretionary spending. Think of items you’d like but could technically live without; these are the bells and whistles that make life just that extra sparkly.

‘Savings’ is about the money to be put aside for your financial goals. It could be cash into your emergency fund, a down payment on a new house, or extra payments to pay off your loans more quickly.

After you’re done with your budget breakdown, you can assess the areas where you’d like to cut back and make adjustments.

The exact proportions will vary from person to person, but 50/30/20 is a good mix to start with.

If you prefer to create your own budget, here’s a simple template. Or perhaps you’re a details person; you might like this then. You can also download templates online through Google Sheets, Microsoft Excel and other sites. Or just start from scratch!

There are countless ways to make and maintain a budget. The exercise in financial responsibility is worthwhile no matter what your income is, so just go for it. Remember, diets and budgets have one thing in common: The best one is the one that works!

#3 Build an emergency fund

Nothing like keeping the stress away like having cash on hand when an emergency strikes! Retrenchment, unexpected health issues…life is unpredictable so why take chances?

What should an emergency fund should cover? Basic expenses such as mortgage and loan payments, insurance premiums, utilities, food, and transportation are a must.

Whether your savings are robust or in need of shoring up, the same advice goes: Set a realistic monthly savings goal – and stick to it, no excuses. An angst-free option to help you stay on track is to have the funds automatically funnelled from your bank account every month and deposited into a designated bank account.

#4 Give your finances a fresh start

The little pieces of plastic are double-edged: a boon if you know how to use them right, without paying a cent in interest while raking up cashback or rewards points; a curse if you’re a big and unchecked spender.

The unpaid interest accrued on a credit card balance is excruciating, typically ballooned by double-digit interest rates, and invariably huge stumbling block in your quest for great financial wellness.

Consider a balance transfer programme, which leverages your available credit card limit, to tackle the credit card debt situation.

By lumping your credit card debt from several sources onto one card that offers 0% or an attractively low interest rate for specific repayment periods, like a Standard Chartered Card Credit Funds Transfer*, and focusing on paying it down in the shortest possible time – before the special interest rate reverts to the original! – your credit card debt will soon be zero-ised.

If your balances can’t fit into one credit card funds transfer, do it on two or more credit cards. But the ritual is the same throughout: Avoid racking up new charges and make disciplined payments.

Ultimately, a credit card funds transfer is just a tool. You’ll still need to commit to making the necessary monthly payments to whittle your balance to $0.

#5 Evaluate the rationale behind big-ticket items

Big-ticket items or BTIs are major buys that are typically long-term and require a substantial financial commitment, like a car or a house. Typically, careful, deliberate consideration goes into such a purchase.

But sometimes, BTIs not on the original to-buy list pop up. What then?

First, take some to dissect the rationale behind the purchase, and look at how it will ding your other financial objectives. Ask yourself questions like:

– What am I willing to forego to have this?

– What do I gain by buying this, and is it worth it?

If you’re happy with your answers, and you’ve done the relevant number crunching, spend away – mindfully, of course. This would be a happy outcome but an even happier one would be if you applied an interest-free instalment programme to the purchase: It will help reduce the pressure of making a full repayment when the bill comes round in a month. Better yet, the cash you would have spent on interest payments can be channelled towards investments.

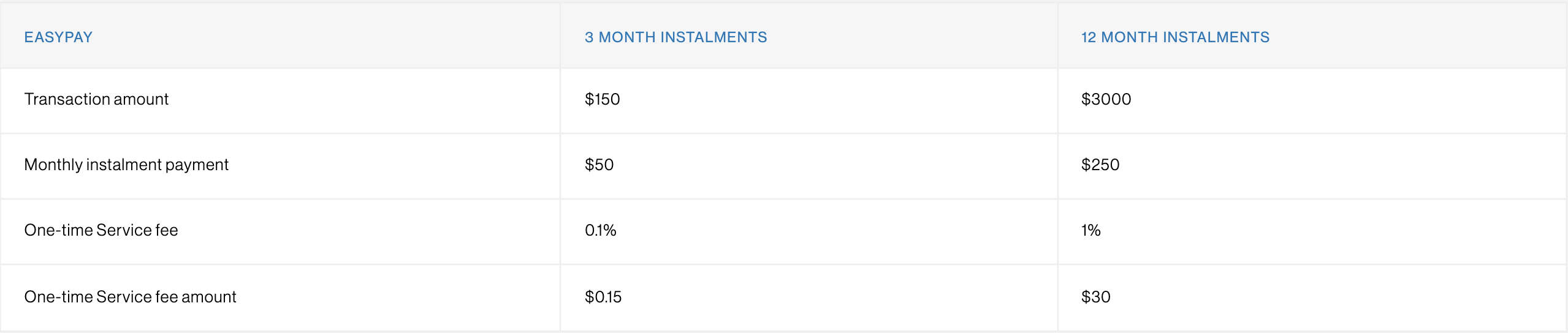

Here’s how an interest-free instalment programme works, using Standard Chartered Bank’s EasyPay* as an example: Because EasyPay converts local or overseas transactions on your Standard Chartered Credit Card into interest-free instalments, by just sticking with the repayment plan vigilantly, you’ve got yourself an attractive and harmless credit facility that effectively keeps unnecessary costs down.

Illustration: EasyPay based on a transaction amount of $150 and S$3,000 respectively.

The example above is for illustration purposes, the actual fee may differ in the actual application and is subjected to change at the Bank’s discretion.

EasyPay splits transactions into interest-free instalments a one-time service fee, as low as 0.1 and offers repayment plans of 3, 6, 9 or 12 months. Find out if it’s for you.

From reaping cashback or reward points to turning your plastic into a effective financial management tool, credit cards can help boost your financial well-being, if you understand how to use them wisely.

Standard Chartered Bank’s Smart Credit Card accommodates both credit card funds transfers and interest-free instalments. It comes with 100% cashback on the processing fee for both the first S$15,000* of Credit Card Funds Transfer and EasyPay with 3 months interest-free instalments.

Apply for a Smart Credit Card today and have your choice of welcome gift: (1) Sonos One SL Speaker (worth S$329) and S$80 cashback PLUS a 6-month Disney+ subscription OR (2) up to S$280 cashback.