This is to inform that by clicking on the hyperlink, you will be

leaving

sc.com/sg

and entering a website operated by other parties.

Such links are only provided on our website for the convenience of

the Client and Standard Chartered Bank does not control or endorse

such websites, and is not responsible for their contents.

The use of such website is also subject to the terms of use and

other terms and guidelines, if any, contained within each such

website. In the event that any of the terms contained herein

conflict with the terms of use or other terms and guidelines

contained within any such website, then the terms of use and other

terms and guidelines for such website shall prevail.

When you lend money to a friend, there is always the danger you will not get it all back. It is a chance you must take. With fixed income investing, this uncertainty is known as credit risk – the ability of the issuer to repay the capital or interest to an investor.

How is credit risk assessed?

The answer to this question lies in a discipline called credit risk analysis. This considers factors such as operating margins, fixed expenses, overhead burdens and cash flow, with the goal of providing a fundamental view of a company’s financial ability to repay its obligations.

A common method of credit risk assessment called ‘bottom up analysis’ seeks to study individual companies’ accounts and business prospects in detail to determine how likely they are to honour their debts. For instance, a poorly performing company may bear high credit risk, despite a favourable economic backdrop, while a well-managed company could still be a relatively safe investment, even if the economy is slowing.

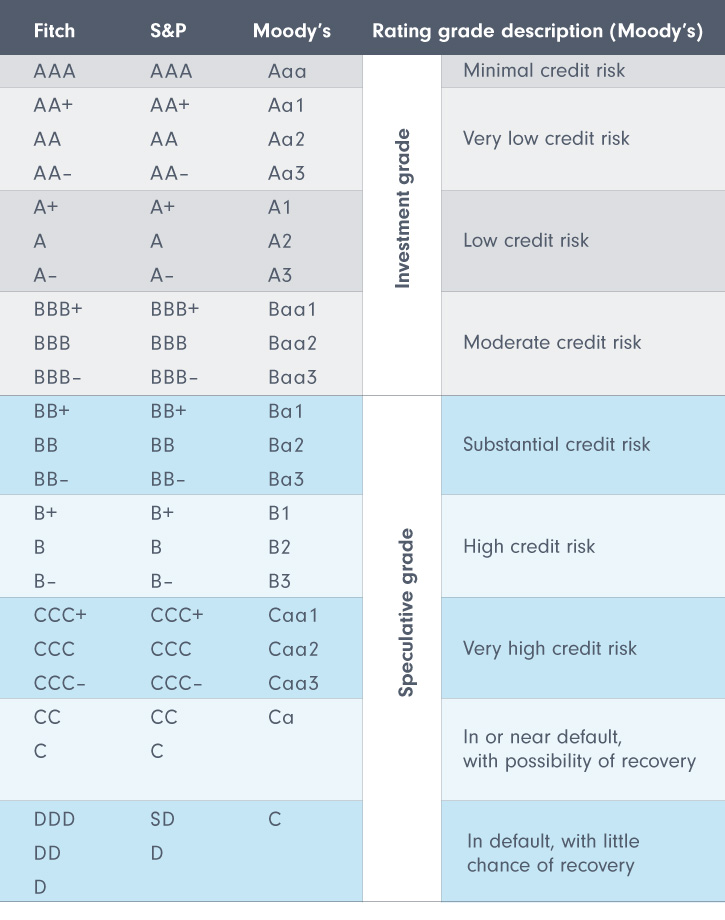

Credit rating agencies carry out such assessments of bond issuers, whether companies or government entities. The primary bond rating agencies are Standard & Poor’s (S&P), Moody’s and Fitch Ratings. Individual bonds are rated broadly as investment grade or high yield – commonly known as ‘junk’ bonds – and under these two grades, bonds are assigned more specific ratings from AAA to D.

In general, a bond with higher credit risk (and lower price) will carry a higher yield, bearing in mind that yield moves in the opposite direction of price. A bond’s rating can be downgraded or upgraded by the rating agencies, which could have implications on price.

Credit risk management

In a bond fund, which is a basket of dozens or hundreds of securities within one bond portfolio, the portfolio manager will look at both the interest rate sensitivity and credit risk of the holdings in a portfolio. It is their job to make sure it is properly diversified with the correct balance struck between risk and reward.

If we look at this differently – the process is similar to the methodology that a bank manager uses in undertaking credit risk management. There will be some loans which are riskier than others, in terms of the borrower’s ability to pay back the capital or principal, whereas others will be safer and require less ongoing scrutiny.

The purpose of a bond’s convenant

The exact terms and conditions attached to a fixed income instrument are contained in the bond’s covenant. This is a legal document which sets out the key metrics that the issuer must meet to safeguard its ability to pay back and service (i.e. pay interest on) the bond. For example, there may be a cap imposed on the amount of debt that a company can have on its balance sheet in proportion to its total assets.

How do credit defaults and credit losses vary?

An essential part of credit risk analysis is trying to determine how much capital will be recovered in the event of a default.

Here, it is worth distinguishing between the defaulted amount and the ultimate capital loss. With fixed income instruments, it is often the case that the actual capital loss is lower than the defaulted amount because of recoveries. This can be because the creditor, or lender, can reach an agreement with the debtor, or borrower, to make the final repayment of the outstanding loan easier. Examples of this could be newly negotiated contract terms, such as a slightly lower interest rate or a longer repayment term. Therefore, with this process, there are parallels with what might happen if a borrower is at risk of defaulting on their mortgage and the lending that a bank subsequently decides to revise the terms of its loan.

Fund structure – an investor perspective

Some bond funds may invest in both investment grade quality and high yield bonds. It is important for individual investors to read a fund’s prospectus to make sure they fully understand the fund’s credit quality guidelines. Since bond funds are made up of many individual bonds, diversification can help mitigate the credit risk of an issuer defaulting or being downgraded, which would affect bond prices. An investment grade bond fund will typically have no less than 80% allocated to investment grade bonds; whereas a high yield bond fund will usually hold most of its assets in non-investment grade bonds.

Your feedback is valuable to us. Did you find this article helpful?

Disclaimer

This article is for general information only and it does not constitute an offer, recommendation or solicitation of an offer to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments. This article has not been prepared for any particular person or class of persons and does not constitute and should not be construed as investment advice or an investment recommendation. It has been prepared without regard to the specific investment objectives, financial situation or particular needs of any person or class of persons. You should seek advice from a licensed or an exempt financial adviser on the suitability of a product for you, taking into account these factors before making a commitment to purchase any product or invest in an investment. In the event that you choose not to seek advice from a licensed or an exempt financial adviser, you should carefully consider whether the product or service described herein is suitable for you.

You are fully responsible for your investment decision, including whether the investment is suitable for you. The products/services involved are not principal-protected and you may lose all or part of your original investment amount.

Standard Chartered Bank (Singapore) Limited will not accept any responsibility or liability of any kind, with respect to the accuracy or completeness of information in this article.

Deposit Insurance Scheme

Singapore dollar deposits of non-bank depositors are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law. For clarity, these investment products are not deposits and do not qualify as an insured deposit under the Singapore Deposit Insurance and Policy Owners’ Protection Schemes Act 2011. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured.

The information stated in this article is accurate as at the date of publication