This is to inform that by clicking on the hyperlink, you will be

leaving

sc.com/sg

and entering a website operated by other parties.

Such links are only provided on our website for the convenience of

the Client and Standard Chartered Bank does not control or endorse

such websites, and is not responsible for their contents.

The use of such website is also subject to the terms of use and

other terms and guidelines, if any, contained within each such

website. In the event that any of the terms contained herein

conflict with the terms of use or other terms and guidelines

contained within any such website, then the terms of use and other

terms and guidelines for such website shall prevail.

However, it’s important to know all of the facts about life insurance before you commit to a policy. Make sure you learn from these seven common mistakes people make when buying life insurance, so you can avoid doing the same.

Mistake #1: Not understanding the various types of life insurance policies

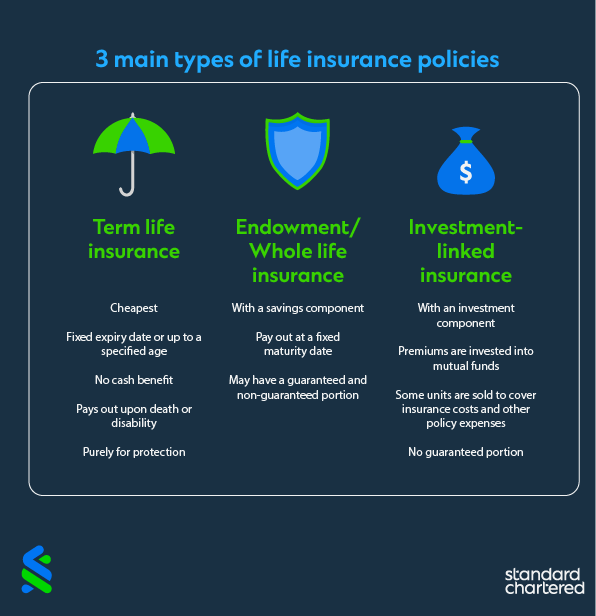

There are three main types of life insurance policies in Singapore:

Term life insurance: The cheapest and most basic form of life insurance. It has a fixed expiry date — usually five to 40 years, or up to a specified age. It has no cash benefit and pays out upon death or disability. You take out this type of life policy purely for protection purposes.

Endowment and whole life insurance: Life insurance with a savings component. The savings part will pay out at a fixed maturity date and may have a guaranteed and non-guaranteed portion, depending on the specific policy.

Investment-linked insurance:Life insurance with an investment component. Premiums are invested into mutual funds, and some of these units are then sold each year to cover insurance costs and other policy expenses. Returns are tracked according to the funds’ performance, and there is no guaranteed portion.

Understanding these key differences will help you identify the right type of life insurance policy for your needs.

Mistake #2: Not having a clear objective before deciding on a life insurance policy

It helps to know exactly what you want your life policy to cover. Speak to your loved ones before deciding on the best life insurance policy in Singapore for you, and decide what coverage you want and need. It may, for example, include protection in case of death, disability, or illness.

There is also the matter of when you want to receive the funds. If you are saving for your retirement or for your children’s education, then you may want to receive your funds earlier. Or, you may just want it to be paid out upon your death.

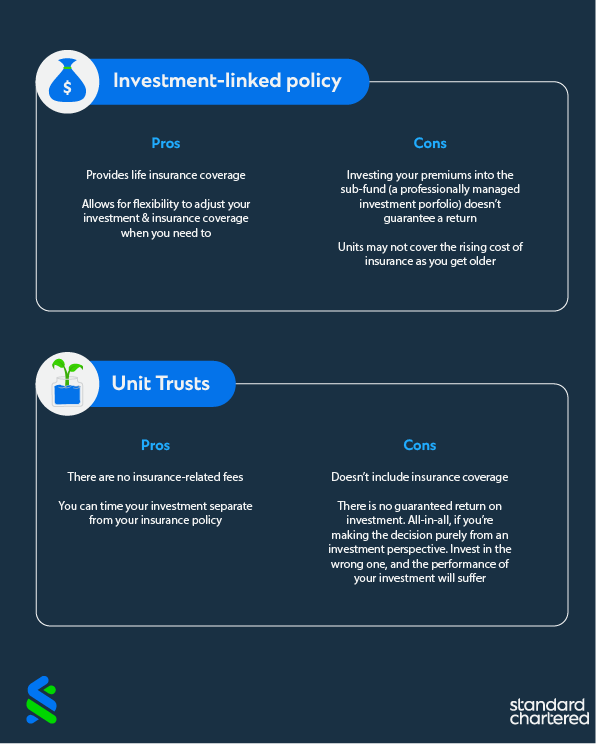

Mistake #3: Using life insurance primarily as an investment vehicle

Combining life insurance coverage with wealth-accumulation goals using an investment-linked policy may seem like a good idea. After all, you get the best of both worlds. However, it may not always be the best option.

The mutual funds you could invest in through an investment-linked insurance policy are likely also available separately as unit trusts. Depending on the specific fund or policy, it may turn out to be cheaper from a fees perspective to buy a term product for insurance protection and invest the premium difference directly into unit trusts instead. Make sure you understand the investment-linked policy pros and cons and those of unit trusts before making your decision. The following are a few to consider.

Mistake #4: Focusing on the wrong coverage priorities

Always review and prioritise your plans based on changes in your life stages. Over time, your objectives will change, whether you’re younger or older, you’re married or single, or you have children or not. As you transition from one life stage to the next, you are likely to require a different level of coverage to suit whatever your current needs. Riders are options that offer additional coverage; however, there are many riders available, and you want to make sure you get the right ones to meet your specific needs. A popular rider is Total and Permanent Disability protection, which provides coverage for unexpected costs arising from a disability.

When you’re considering coverage, being over insured is better than being underinsured, but there are opportunity costs involved; you may be paying for ‘features’ that you don’t need. Could you more productively use that extra money that you’re putting towards premiums? For instance, it may be worth it to consider using that money to invest in a different product.

Mistake #5: Incorrectly setting up ownership and beneficiaries

When you purchase life insurance, it’s important to make sure you have properly set up who will own the policy and who its nominees and beneficiaries will be. This proper setup, in turn, helps ensure the policy will achieve its planned purpose. Ask yourself the following questions:

Will the policy be in your name?

Will you use a trust?

Who will the policy’s beneficiaries be (both primary and contingent)

Who is the nominee (person appointed by the policyholder to manage finances after his or her death)?

Is the beneficiary a minor?

Will you have multiple beneficiaries?

How much will each beneficiary receive?

It’s also important to note that if you have a will and one of your policy beneficiaries is listed in it, that doesn’t necessarily mean that he or she will receive the proceeds. This doesn’t mean you shouldn’t include your policy in your will; it’s beneficial for anyone dealing with a will to know the assets of the deceased. However, it does further emphasise the importance of setting up your policy properly from the beginning and updating it along the way. Doing so will save your family a lot of time and hassle when the time comes for the life insurance policy to pay out.

Mistake #6: Buying on impulse

Don’t jump into a life policy without understanding how it works and how it can meet your needs. Often, under emotional circumstances, such as times of intense stress at one extreme or happiness at the other, people will buy something on impulse. Or they may act out of fear that they’re missing out on something they should have. Before you act hastily and commit, it’s important to take your time and make sure you understand a policy’s features, risks, returns and limitations. If you’re unsure, shop around and compare policies. Although only a few broad categories of life insurance policies exist, the differences from policy to policy and from insurer to insurer can vary widely.

Mistake #7: Taking too long to buy

So, you’ve done all of your research and have a clear idea of what you’d like to achieve with your life insurance. And though we’ve already urged you not to make an impulse purchase, it’s equally important that you don’t wait too long to buy your policy. With life insurance, the older you are, the more expensive purchasing a policy can become. By planning for and purchasing life insurance at a younger age, you’re more likely to save a substantial amount of money in the long run.

Always get a tailored plan

As we’ve learned, it’s easy to make mistakes when buying life insurance in Singapore. That’s why it’s key to understand the finer details of each of the policies available and the pros and cons of each.

Everyone’s life and goals are unique. Your insurance policy should cater to these unique needs. Now that you know which mistakes to avoid and how to avoid them, you’re in a better position to purchase a policy that truly suits you.

Whether your goal is to accumulate wealth or ensure that your loved ones are protected in the long term, Standard Chartered is here to help you achieve your objectives. The earlier you get started on this journey, the better. Speak to one of our trusted financial advisers today to learn more about how we can help you.

Your feedback is valuable to us. Did you find this article helpful?

Disclaimer

This article is for general information only and it does not constitute an offer, recommendation or solicitation of an offer to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments. This article has not been prepared for any particular person or class of persons and does not constitute and should not be construed as investment advice or an investment recommendation. It has been prepared without regard to the specific investment objectives, financial situation or particular needs of any person or class of persons. You should seek advice from a licensed or an exempt financial adviser on the suitability of a product for you, taking into account these factors before making a commitment to purchase any product or invest in an investment. In the event that you choose not to seek advice from a licensed or an exempt financial adviser, you should carefully consider whether the product or service described herein is suitable for you.

You are fully responsible for your investment decision, including whether the investment is suitable for you. The products/services involved are not principal-protected and you may lose all or part of your original investment amount.

Standard Chartered Bank (Singapore) Limited will not accept any responsibility or liability of any kind, with respect to the accuracy or completeness of information in this article.

Deposit Insurance Scheme

Singapore dollar deposits of non-bank depositors are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law. For clarity, these investment products are not deposits and do not qualify as an insured deposit under the Singapore Deposit Insurance and Policy Owners’ Protection Schemes Act 2011. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured.

The information stated in this article is accurate as at the date of publication