This is to inform that by clicking on the hyperlink, you will be

leaving

sc.com/sg

and entering a website operated by other parties.

Such links are only provided on our website for the convenience of

the Client and Standard Chartered Bank does not control or endorse

such websites, and is not responsible for their contents.

The use of such website is also subject to the terms of use and

other terms and guidelines, if any, contained within each such

website. In the event that any of the terms contained herein

conflict with the terms of use or other terms and guidelines

contained within any such website, then the terms of use and other

terms and guidelines for such website shall prevail.

It says a lot about the state of world affairs when gold is on pace to handsomely outperform global stocks and global bonds for the second year in a row. In fact, gold is on pace to outperform global bonds for the tenth year in a row. Gold’s record-breaking rally, fuelled by geopolitical uncertainty and concerns about easing fiscal policies worldwide, has lifted the price of the precious metal by over 50% this year, and by more than 150% over the past three years. We have strong conviction that gold will outperform global stocks and bonds again in 2026.

Of course, questions about gold’s valuation remain front-and-centre in our client conversations. While gold does not lend itself to traditional valuation measures – since holders do not earn regular income – some relative valuation metrics indicate room for further upside, despite near-term volatility. Hence, we have raised our 3- and 12-month gold price outlook to USD4,300/oz and USD4,500/oz, respectively. Our continued constructive stance on gold is primarily driven by structural drivers and supported by cyclical factors.

Structural drivers of the gold rally

The structural drivers of gold are threefold:

i)Geopolitical uncertainty. Western financial sanctions against Russia in 2022 following the start of the Ukraine war, including freezing of Russia’s central bank assets, were the genesis of gold’s almost parabolic rally. The decision to freeze assets shook Emerging Markets’ (EM) confidence in the security of their reserves held overseas. This led EMs to consistently boost their gold reserves in the past three years. The top three EM central bank gold holders – China, India and Russia – now have around 8%, 15% and 41% of their officially declared reserves in gold. In contrast, the share of gold in U.S. central bank reserves is 78%. These levels suggest there is scope for further upside in EM central bank demand for gold in the coming years.

ii)Concerns about expansionary fiscal policies worldwide. Concerns about lax fiscal policy have risen since the pandemic as the U.S. government continued to ease policy even with the economy growing faster than long-term trend. These concerns increased with the passage of the latest U.S. budget for the fiscal year which started on 1 Oct (the “One Big Beautiful Bill”). Meanwhile, Japan’s new government has just unveiled a larger-than-expected stimulus package, which is likely to further increase the government’s debt which is already close to 230% of GDP, the largest in the world by this measure. Gold, thanks to finite supplies, is seen as an antidote to fiscal profligacy.

iii)Increased doubts about the Fed’s independence. U.S. President Trump’s decision to fire Fed Governor Cook in August (subsequently stayed by courts) added fuel to gold’s rally as it raised concerns about the Fed’s independence and therefore about potential risks to the U.S. Dollar.

Cyclical drivers for the next 6-12 months

Besides structural drivers, gold has cyclical support from three factors:

a) Fed policy easing and falling real rates: The Fed resumed rate cuts in September, after a nine-month pause, to support a slowing job market. It then cut rates again in October to 4.0%, despite core inflation remaining close to 3%. We expect the Fed to cut rates another 75bps by end-2026, dragging U.S. real bond yields and the USD lower. Lower U.S. real yields and a weaker USD make non-interest-bearing gold relatively more attractive.

b)Seasonal demand from China ahead of the Lunar New Year. Jewellery accounts for half of global gold demand, with China and India accounting for over half of the world’s jewellery market. Seasonal demand typically picks up from the Indian festive season in September and runs until the Lunar New Year in January/February. While India’s festive season this year saw a decline in volumes as buyers turned more price sensitive, the overall value of gold sold hit new highs, with demand shifting to gold bars and coins and digital gold. Meanwhile, China’s removal of a tax rebate on gold is likely to be a temporary headwind for demand going into the festive season.

c) Rising demand for gold as an alternative investment. The nascent shift in Indian demand towards gold bars, coins, gold-backed ETFs and digital gold suggests gold’s rising role as an alternative investment. Among institutional investors, gold remains under-owned, with significant scope for upside.

Is gold overvalued?

Gold’s stellar rally has raised questions about whether it is overvalued. It is hard to value gold as a financial asset, given the lack of cash flows. However, we can assess gold’s worth in two ways:

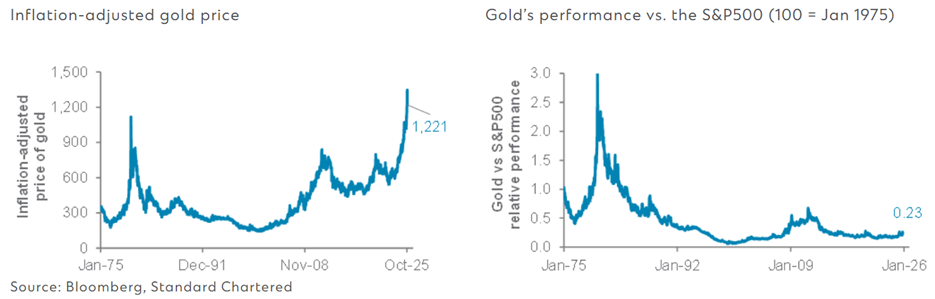

a) Relative value terms: Measuring gold in inflation-adjusted terms shows the precious metal is priced today marginally higher than the peak of the stagflationary 1970s. The first chart below shows that gold displays its true worth in times of crises – eg, the 1970s stagflation, the 2007-08 Global Financial Crisis, the 2020 COVID pandemic and the latest geopolitical shock caused by the Russia-Ukraine conflict and Trump 2.0. Nevertheless, gold is expensive compared to crude oil. On balance, the relative value assessment suggests gold is likely to hold its value as long as the world remains in a state of heightened policy uncertainty.

b) Asset allocation terms: Gold’s historically low correlation with other assets makes it one of the best portfolio diversifiers. For instance, gold delivered an average 22% real annualised return during stagflation periods since 1973, vs. -1.5% return on U.S. equities. Also, gold is extremely inexpensive vs. U.S. equities (see chart below), given the outperformance of stocks in the past three decades. Gold’s share of a typical portfolio would have plunged unless investors actively added gold over the years. Many investors remain underinvested in gold, with allocation through ETFs still below the 2020 peak.

The biggest risk to gold’s sustained rally is if the Fed halts rate cuts or starts to hike again to get ahead of inflation. There is low risk of this outcome, given rising pressure from the Trump administration to maintain an easy monetary policy. Also, the U.S. job market is slowing and leading inflation indicators show moderation ahead, making Fed rate cuts more likely than rate hikes in the coming year.

A peace deal between the West and Russia, leading to a release of Russia’s frozen assets, and/or a U.S.-China detente are other potential near-term risks to gold prices. Nevertheless, we believe the 2022 freezing of Russian assets marked a regime shift – EM central banks are likely to keep building their gold reserves, despite any peace deal, providing medium-to-long-term upside to gold prices.

Conclusion: Based on the above review, while gold appears expensive in some relative value metrics, strategic and cyclical factors suggest the ongoing technical correction in gold is an opportunity for those underinvested in gold to build allocations towards desired targets. Our balanced asset allocation strategy has a 7% allocation to gold.

Gold, adjusted for inflation, currently trades at a higher level than the 1970s’ stagflation period. However, gold trades at rock-bottom levels relative to US equities.

Your feedback is valuable to us. Did you find this article helpful?

Disclaimer

This article is for general information only and it does not constitute an offer, recommendation or solicitation of an offer to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments. This article has not been prepared for any particular person or class of persons and does not constitute and should not be construed as investment advice or an investment recommendation. It has been prepared without regard to the specific investment objectives, financial situation or particular needs of any person or class of persons. You should seek advice from a licensed or an exempt financial adviser on the suitability of a product for you, taking into account these factors before making a commitment to purchase any product or invest in an investment. In the event that you choose not to seek advice from a licensed or an exempt financial adviser, you should carefully consider whether the product or service described herein is suitable for you.

You are fully responsible for your investment decision, including whether the investment is suitable for you. The products/services involved are not principal-protected and you may lose all or part of your original investment amount.

Standard Chartered Bank (Singapore) Limited will not accept any responsibility or liability of any kind, with respect to the accuracy or completeness of information in this article.

Deposit Insurance Scheme

Singapore dollar deposits of non-bank depositors are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law. For clarity, these investment products are not deposits and do not qualify as an insured deposit under the Singapore Deposit Insurance and Policy Owners’ Protection Schemes Act 2011. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured.

The information stated in this article is accurate as at the date of publication.

Global Market Outlook H2 2025: Positioning for a weak dollar

We are Overweight global equities. Policy easing worldwide, strong chances of a US soft landing and a weaker USD are supportive of risky assets. We favour diversified global equity exposure, within which we upgrade Asia ex-Japan equities to Overweight.