This is to inform that by clicking on the hyperlink, you will be

leaving

sc.com/ae

and entering a website operated by other parties.

Such links are only provided on our website for the convenience of

the Client and Standard Chartered Bank does not control or endorse

such websites, and is not responsible for their contents.

The use of such website is also subject to the terms of use and

other terms and guidelines, if any, contained within each such

website. In the event that any of the terms contained herein

conflict with the terms of use or other terms and guidelines

contained within any such website, then the terms of use and other

terms and guidelines for such website shall prevail.

This article is brought to you by Standard Chartered Bank (UAE) Limited. All information provided is for informational purposes only.

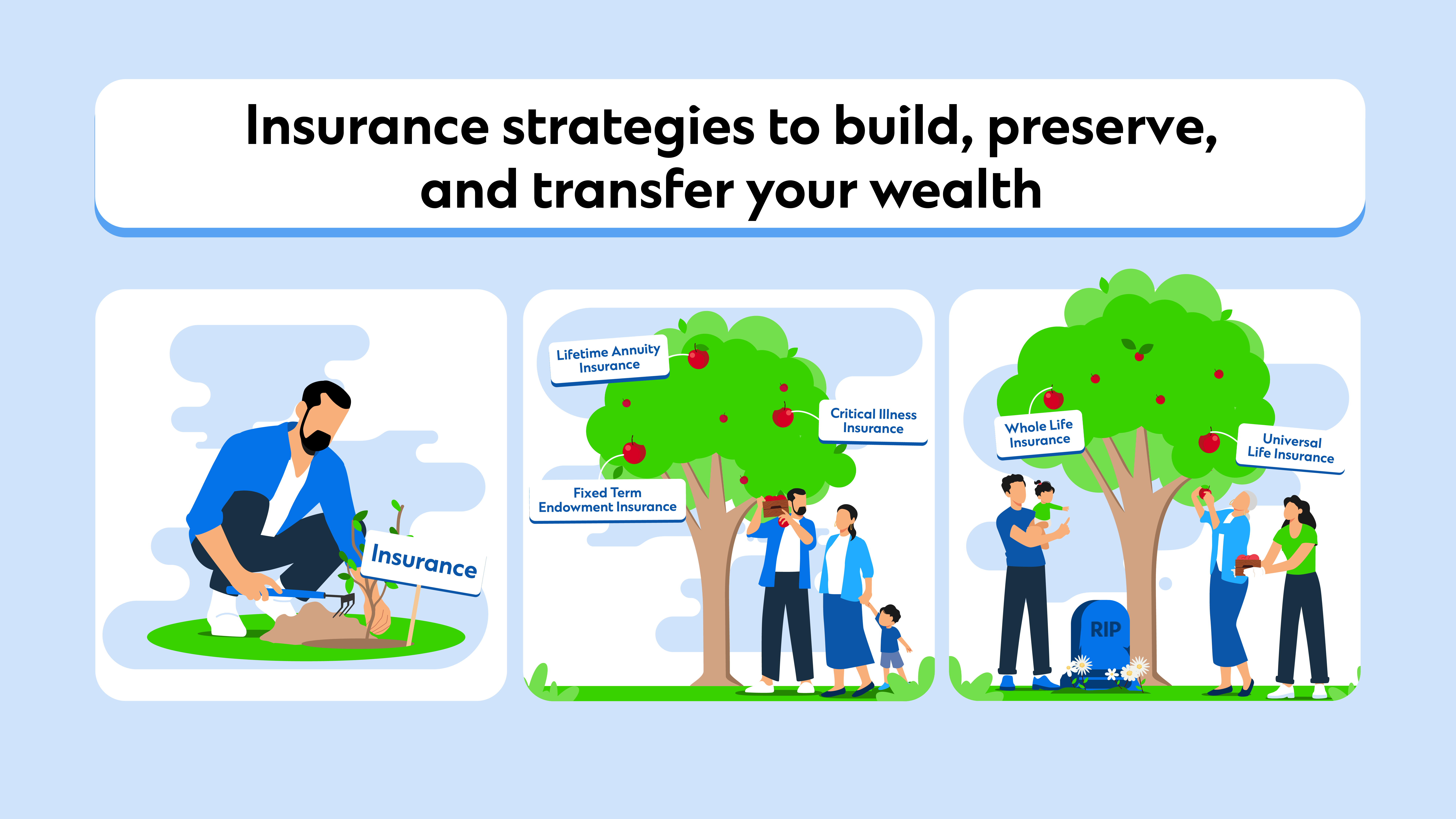

4 insurance strategies to build, preserve, and transfer your wealth

Insurance is one of many welcome solutions in achieving a holistic wealth management plan. While better known for its financial protection benefits, insurance can also help you build, preserve, and transfer your wealth.

Many people, have after all, reaped the benefits of insurance, including, but not limited to, mitigating risk by diversifying their investment portfolio, ensuring security in their financial planning, avail tax exemptions and providing retirement and legacy funding.

Discover four definitive strategies to build, preserve and transfer your wealth pool – with insurance.

1. Ensure income continuity to navigate income loss due to death, disability, critical illness, or hospitalization

Generally, health insurance is purchased to offset hospital and medical expenses when the insured party falls ill, becomes injured, or worse, faces disablement.

While they help tide over the high medical costs due to illness or disability, there often remains a protection gap, it is thus important to ensure there is a provision for replacement of income on the road to recovery.

Some insurance plans can help with such income continuity either in the form of single or regular cash payouts. Below are some types of insurance plans that provide such income protection:

Term Insurance– This insurance type provides a death benefit if the insured individual passes on within the policy’s specified term

Critical Illness Insurance– If you are diagnosed with a critical illness (including major cancers, heart attacks, strokes and etc) as per the plan definition, you will be paid a specified lump sum.

Hospital Cash Insurance– For every day you’re admitted in a hospital, the insurance company will pay you a fixed daily sum.

Disability Income Insurance– This option allays your income loss to a certain extent if you become disabled and are unable to work due to disability

Personal Accident Coverage– If an accident were to cause you either temporary total disability, permanent partial disability, permanent total disability or accidental death, a coverage sum would apply depending on the type of disability

Certain emirates of the United Arab Emirates offer health insurance schemes. Abu Dhabi’s Thiqaprogramme, for example, extends comprehensive medical coverage to every Abu Dhabi resident or UAE national. With a thiqa card, citizens between the ages of 18 to 75 years are able to gain public and private healthcare coverage. Please note that a health screening requirement applies.

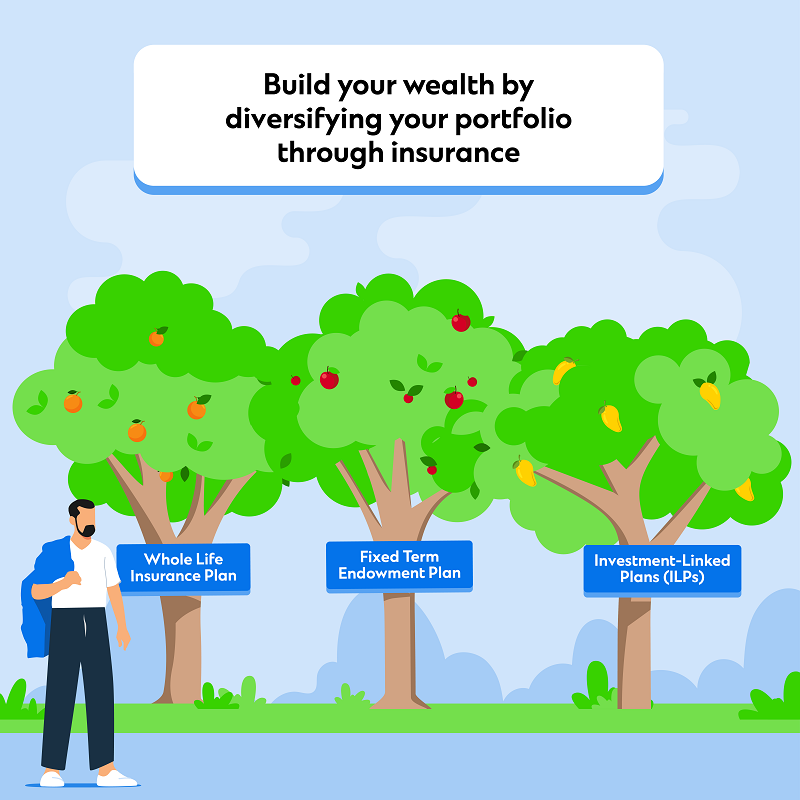

2. Instill discipline, diversify assets and minimize risk to build your wealth and help your portfolio get closer to becoming an all-rounder

In order to achieve your goals in building your wealth, use insurance plans to diversify your investment portfolio. You can make use of whole life plans, fixed term endowment plans or investment-linked plans to achieve your wealth accumulation goals while managing risks.

Let’s look at how these plans can work for you.

A whole life insurance plan gives coverage that provides protection for your entire lifespan. These plans (along with protection) provide cash value that grows over time through investment gains accrued based on guaranteed or non-guaranteed (in the form of bonuses) returns.

A fixed term endowment insurance plan, on the other hand, works as a combination of a term insurance plan and a savings plan, with a fixed maturity term. There is death coverage for unforeseen death during the policy term or a survival or maturity benefit that is paid out if you survive until the policy’s maturity.

Fixed term endowment plans are also very useful when saving for a specific goal like children’s education or saving for down payment of a new house, etc. as it allows to instill discipline of regular and systematic savings.

Investment-linked plans or ILPs are life insurance policies that allow you to participate directly in the investment markets to enhance your wealth accumulation goals. Most ILP plans give you the flexibility to choose the premium and/or life cover, and asset classes (investment funds).

A part of the premium (after deducting for any charges) goes towards life insurance protection coverage, while the other part will be used to purchase investment units, the price of which depends on the price per unit or NAV of your preferred fund.

Now, if your portfolio is made up of low-risk investment assets, ILPs could provide you a well-rounded investment portfolio with funds that have a slightly higher risk (with a potential higher return). On the other end, if most of your investments are assets with higher risks (like equities), then opt to lower your risk by adding fixed term endowment plans.

3. Boost and secure your retirement income for as long as you live

Planning for your retirement can seem like a daunting, monumental task. You’d need to primarily ensure that you have a steady stream of income for you to retire without worry once you’ve stopped working. One surefire way of ensuring you don’t run out of funds altogether is via lifetime annuities.

With a lifetime annuity insurance plan, you’d opt to pay a singular or a monthly premium sum for a fixed timeframe (while you’re working or running your business). When you reach your desired retirement age, you’d be able to enjoy the annuity payouts that are due to you at the frequency you prefer.

Lifetime annuity certainly proves itself useful if you want definite security in establishing your retirement income stream. Do note though these annuity plans provide a number of choices when you buy the plan on how to distribute the remaining funds (to your beneficiary) in the event of an unforeseen demise.

4. Funding your legacy goals with whole life insurance and universal life plans

Balancing your financial goals that cross two junctures simultaneously – legacy planning and retirement planning – can seem like a trade-off, as you’d have to consider tipping one scale lower to benefit the other more.

It does not necessarily have to be that way, as there are insurance solutions that can work to grow your legacy and retirement income sources in tandem.

For instance, purchasing a whole life policy would provide you the option to grow your retirement nest egg until you reach your desired retirement age. In the unforeseen event of your demise, the payout from the whole life plan would help your beneficiaries realign their finances.

Upon reaching your desired retirement age, you could use the value of your whole life plan to purchase a lifetime annuity, which would provide you with lifetime income as long as you live and upon your passing pay the balance value of your policy to your beneficiary as your legacy.

Life insurance also helps in solving issues related to equal asset distribution. When your beneficiaries are faced with tough calls in splitting properties and heirloom jewelry which tend to require liquidation for fair distribution, life insurance payouts could help – one beneficiary could opt for an asset, while another takes the same, but in cash value.

This can be achieved by using insurance plans like Universal life plans, that give you better choice and flexibility in your legacy planning. Universal life insurance is a type of flexible permanent plan that offers low-cost protection of term life insurance as well as a savings element which is invested. to build your cash value.

Discover the right insurance solution for you

A qualified financial advisor plays an integral role. As professional, they understand which factors would be important to you when purchasing an insurance plan, and how to best structure your insurance portfolio to help you achieve your financial goals while protecting your loved ones.

Growing, managing, and protecting your wealth requires close attention and planning. Understand which factors would be important to you prior to purchasing an insurance plan, and how to best structure your insurance portfolio to help you achieve your financial goals while protecting your loved ones.

By working alongside qualified financial advisers, you will experience a robust advisory process, as well as a continuous focus on key wealth principles – Discipline, Diversification, Time in the Market, Risk vs Return, and Protection, to guardrail all your investing decisions.

Standard Chartered UAE is licensed by the Central Bank of the U.A.E.

Standard Chartered Bank does not offer insurance advice, nor does it underwrite or issue insurance policies. Insurance products are underwritten by third party insurance providers. Standard Chartered Bank shall not be responsible for insurance provider’s actions or decisions, nor shall Standard Chartered Bank be liable regarding payment of claims or services under the policy/insurance contract or in any manner whatsoever regarding your application or the contract of insurance.

The contents of this webpage do not constitute a contract of insurance and reference should be made to the respective policies for the exact terms and conditions applicable to the insurance policy. This webpage is being distributed for general information only and it does not constitute an offer, recommendation, solicitation to enter into any transaction. If there is any discrepancy between the information contained in the above and the Terms of the policy, the Terms of the policy shall prevail.