This is to inform that by clicking on the hyperlink, you will be

leaving

sc.com/sg

and entering a website operated by other parties.

Such links are only provided on our website for the convenience of

the Client and Standard Chartered Bank does not control or endorse

such websites, and is not responsible for their contents.

The use of such website is also subject to the terms of use and

other terms and guidelines, if any, contained within each such

website. In the event that any of the terms contained herein

conflict with the terms of use or other terms and guidelines

contained within any such website, then the terms of use and other

terms and guidelines for such website shall prevail.

Wealth BuildingFixed Income & BondsForex, Gold & Alternative InvestmentsInvestment StrategiesStocks, ETFs & TradingUnit Trusts & Mutual Funds

03 Sep 2025 I 5 mins read

When it comes to investing, it is tempting to chase what is trending – be it tech stocks, crypto or the latest thematic fund. However, long-term success is not built on hype. It is built on structure, discipline and a portfolio strategy that can weather the ups and downs of the market cycle.

A foundation-first approach

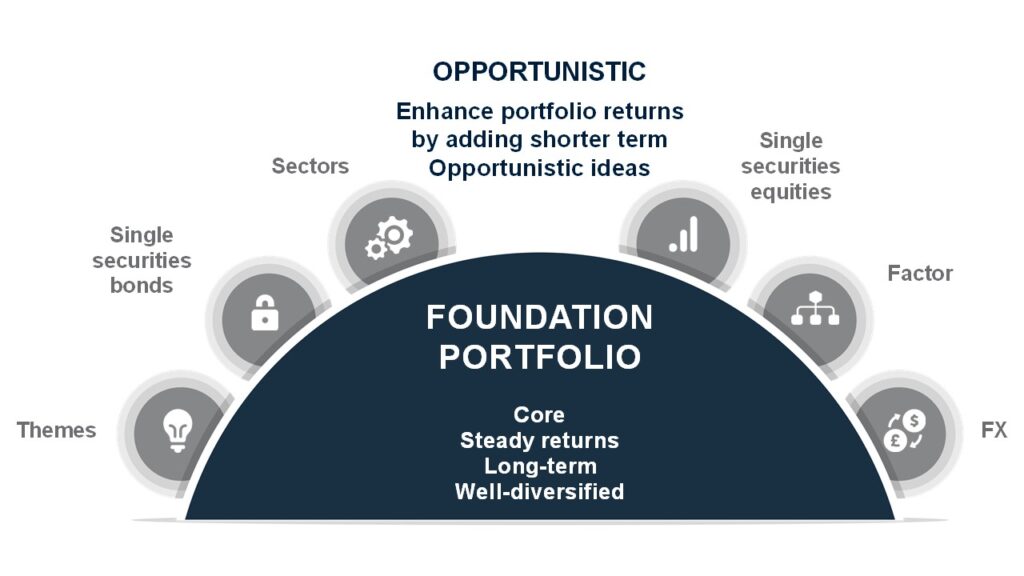

At the heart of a resilient investment strategy lies a simple, but powerful, concept: an optimal balance between foundation vs opportunistic investing, where the foundation provides consistency, and the opportunistic offers flexibility. A strong foundation portfolio is one which is: a) diversified across assets (equities, bonds, alternatives), b) geographically balanced, c) built to withstand market drawdowns, and most importantly, d) aligned with your long-term goals. It is the part of your portfolio you should be comfortable adding to – especially during periods of market volatility – because it is designed to compound steadily over time.

The opportunistic layer

Once a foundation portfolio is in place, one can add opportunistic investments. These are more-focused, higher-risk exposures aiming to capture specific market trends or inefficiencies. Examples include equity/bond sector or thematic funds, factor strategies (e.g. value, momentum), single securities (e.g. stocks, High Yield bonds) or even digital assets. These investments can offer outsized returns but come with greater volatility and downside risks. Sizing is key – limit opportunistic assets to only 10-30% of your portfolio so they enhance rather than derail your long-term strategy.

Fig.1 A “foundation-opportunistic” portfolio approach pairs a diversified core with a flexible sleeve to boost returns

Source: Standard Chartered

Tailoring the foundation to your life stage

A foundation portfolio can tilt towards growth- or income-oriented strategies or a blend of both, depending on your financial goals and where you are in life.

Growth strategies focus on long-term capital appreciation. These are best suited for investors with horizons beyond 10 years, with minimal cash flow needs. Investing success hinges on compounding returns: reinvested dividends and regular contributions significantly boost returns over time. Since 1999, returns from reinvesting dividends have accounted for 268% difference in cumulative returns in the S&P 500 index compared with not reinvesting the dividends. Crucially, time in the market matters more than timing the market. The longer the time horizon, the narrower the performance gap between the best and worst possible returns over an investment period.

Income strategies prioritise steady cash flows. This is relevant for retirees or those who need regular payouts. But beware of longevity risk – drawing too much too early may deplete the portfolio, particularly if distributions are not reinvested. A balanced portfolio of both bonds and equities provides better inflation protection and sustainability than bonds alone. Historical simulations suggest that a balanced portfolio has a 90% probability to last through a 30-year retirement, assuming a 4% annual withdrawal rate, versus just 42% probability for a bonds-only portfolio.

Blended strategies combine the best of both. The key is not to over-allocate to income if payout isn’t essential, as this sacrifices the benefits of compounding to long-term returns. For instance, if you require USD1 k per month and your income portfolio yields 6%, you only need to invest USD 200,000 for income. The rest can be invested for growth.

Two considerations for income investors:

Hedge currency exposure in bonds – Currency swings often outweigh bond volatility and can have a significant impact on total returns.

Avoid value traps – Extremely high yields may be unsustainable, funded by alternative sources, rather than genuine operating earnings or income.

Don’t forget cash: Optionality vs opportunity cost

Cash is often overlooked in a portfolio discussion, but it plays a critical role. It offers optionality – the flexibility to buy undervalued assets when opportunities arise or to cover unexpected expenses. However, holding too much cash can erode long-term returns, making it harder to beat inflation.

A good rule of thumb is to hold at least six months of fixed expenses in cash and invest the rest. Cash tends to outperform risky assets only during recessions or stagflationary periods, which are rare occurrences. Outside of those windows, it is a drag on performance.

Time is your friend

With a well-diversified foundation portfolio, time becomes your greatest ally. The longer your investment horizon, the lower the chances of losses, and the more powerful compounding becomes.

This is why having a strategy matters, not just picking what is popular. A thoughtful portfolio gives you the confidence to stay invested, rebalance when needed and lean in during downturns. It is not about timing the market. It is about time in the market.

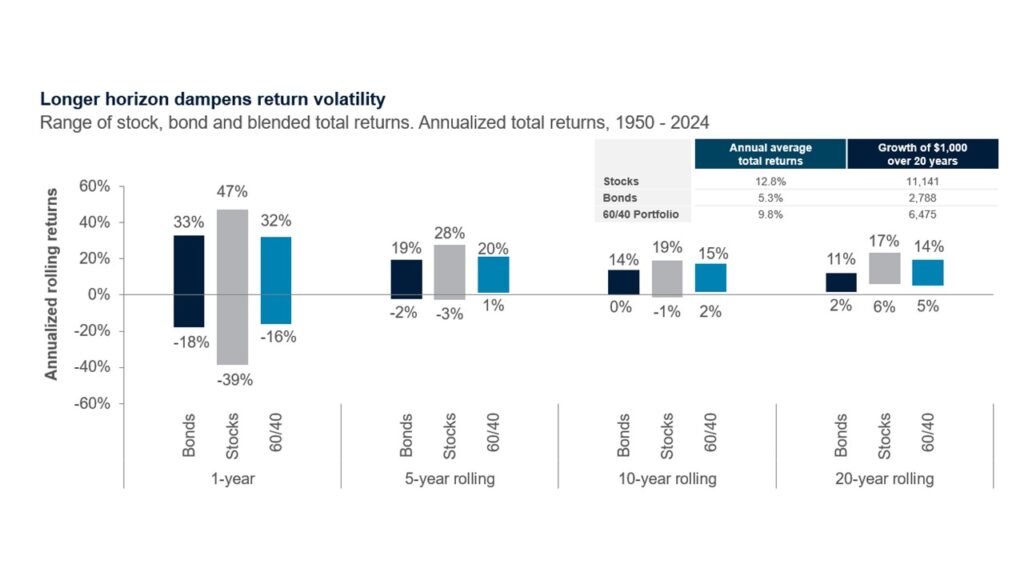

Source: Standard Chartered, Bloomberg

Returns shown are based on calendar year returns from 1950 – 2024. Stocks represented by the S&P Shiller Composite Index. Bonds represented by the US 10-year yield

Your feedback is valuable to us. Did you find this article helpful?

Disclaimer

This article is for general information only and it does not constitute an offer, recommendation or solicitation of an offer to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments. This article has not been prepared for any particular person or class of persons and does not constitute and should not be construed as investment advice or an investment recommendation. It has been prepared without regard to the specific investment objectives, financial situation or particular needs of any person or class of persons. You should seek advice from a licensed or an exempt financial adviser on the suitability of a product for you, taking into account these factors before making a commitment to purchase any product or invest in an investment. In the event that you choose not to seek advice from a licensed or an exempt financial adviser, you should carefully consider whether the product or service described herein is suitable for you.

You are fully responsible for your investment decision, including whether the investment is suitable for you. The products/services involved are not principal-protected and you may lose all or part of your original investment amount.

Standard Chartered Bank (Singapore) Limited will not accept any responsibility or liability of any kind, with respect to the accuracy or completeness of information in this article.

Deposit Insurance Scheme

Singapore dollar deposits of non-bank depositors are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law. For clarity, these investment products are not deposits and do not qualify as an insured deposit under the Singapore Deposit Insurance and Policy Owners’ Protection Schemes Act 2011. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured.

The information stated in this article is accurate as at the date of publication.

Global Market Outlook H2 2025

Positioning for a weak dollar We are Overweight global equities. Policy easing worldwide, strong chances of a US soft landing and a weaker USD are supportive of risky assets. We favour diversified global equity exposure, within which we upgrade Asia ex-Japan equities to Overweight.