This is to inform that by clicking on the hyperlink, you will be

leaving

sc.com/sg

and entering a website operated by other parties.

Such links are only provided on our website for the convenience of

the Client and Standard Chartered Bank does not control or endorse

such websites, and is not responsible for their contents.

The use of such website is also subject to the terms of use and

other terms and guidelines, if any, contained within each such

website. In the event that any of the terms contained herein

conflict with the terms of use or other terms and guidelines

contained within any such website, then the terms of use and other

terms and guidelines for such website shall prevail.

*SingPass holders with a MyInfo profile can use MyInfo

to automatically fill up the form. By clicking “Next”, you will

be re-directed to the MyInfo

portal, which is not owned or controlled by Standard Chartered

Bank (Singapore) Limited or any member of the Standard Chartered

Group (the “Bank”). The Bank bears no liability or

responsibility over your usage of the MyInfo portal.

*Please note that MyInfo is temporarily unavailable at the stipulated downtimes:

Mon, Tues, Thurs, Fri, Sat: 5:00AM to 5:30AM. Wed: 2:00AM

to 6:00AM. Sun: 2:00AM to 8:30AM

I am an existing Standard Chartered Current/Checking/Savings

Account holder

*SingPass holders with a MyInfo profile can use MyInfo

to automatically fill up the form. By clicking “Next”, you will

be re-directed to the MyInfo

portal, which is not owned or controlled by Standard Chartered

Bank (Singapore) Limited or any member of the Standard Chartered

Group (the “Bank”). The Bank bears no liability or

responsibility over your usage of the MyInfo portal.

*Please note that MyInfo is temporarily unavailable at the stipulated downtimes:

Mon, Tues, Thurs, Fri, Sat: 5:00AM to 5:30AM. Wed: 2:00AM

to 6:00AM. Sun: 2:00AM to 8:30AM

I am an existing Standard Chartered Current/Checking/Savings

Account holder

Blackrock offers top tips to help your money deliver.

Nobody likes the unknown, including when it comes to the future value of your money. Retirement planning used to be simple – invest in a portfolio [of bonds?] that comfortably paid a steady stream of income for life while keeping the bulk of your investments (the principle) for the next generation.

My father-in-law regularly reminds me of a time in the early ‘80s when he was able to buy municipal bonds with a 12% yield. Unfortunately, in our current reality of lower interest rates, a comfortable stream of income has become far more challenging to achieve. Many retirement investors find themselves faced with no-win choices:

– spend less

– take on more risk in their portfolio

– withdraw money from their nest egg earlier than planned

Prematurely ‘decumulating’ (withdrawing money from your nest egg) is bad for two reasons: (1) it reduces your base of money overall and (2) it reduces your future income stream earned from that money.

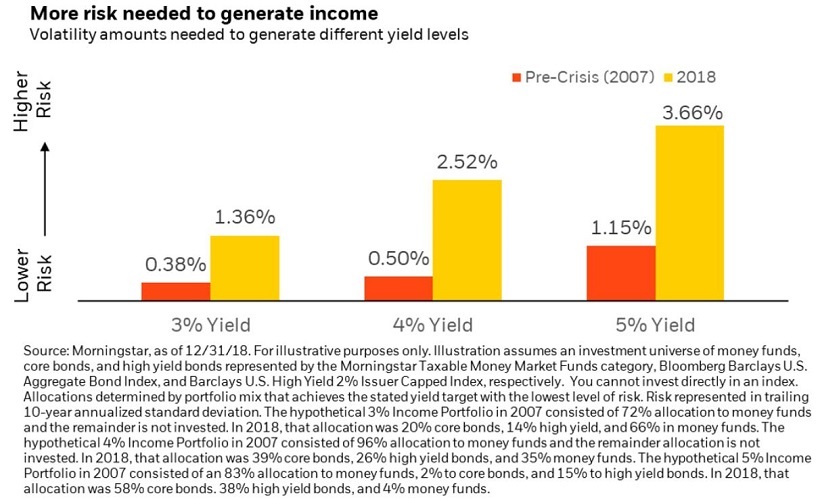

The chart below outlines the challenge. Today, we need to accept three to five times more volatility than we did before the 2007 credit crisis in order to generate yield targets of between three and five percent.

So beyond wishing for interest rates to bounce back to historic highs, what can you do to help your portfolio produce income into your golden years?

1. Set an income target, and make sure it’s reasonable

Ideally your portfolio should provide the cash flow you need with some wiggle room. But with interest rates lingering well below historical norms, you also need to be realistic about the income your portfolio can deliver. A relatively safe bet is to set a yield target in line with the yields of core bonds. A good point of reference here is the yield of the Bloomberg Barclays US Aggregate Bond Index The closer you can stay to that level, the longer your portfolio can likely sustain you.

If your income target depends on a market-beating yield, chances are you will need to invest in riskier assets and experience more portfolio – and income – volatility. Consider that reaching for higher yield now may result in losses that mean fewer years of retirement income later.

2. Focus on the purpose of the investments and the costs

Even if your current portfolio is consistently meeting your income targets, it is worth considering the longer term ‘costs’ or tradeoffs of your investment choices. For example, annuities are the poster child for highly reliable income products – but they tend to be expensive and, depending on the type you choose and how long you live, there may be little or nothing left to pass on to the next generation.

On the flip side, a standard investment portfolio has the potential to increase in value over time, but it lacks the guarantees of annuities, meaning you’ll likely have higher volatility and more variable income. Your ultimate goal should be achieving your priorities, even if it comes with higher fees. If you most value steady income, annuities may be your best friend, but if your highest goal is to build a legacy, an investment portfolio may be better

3. Know that risk can take many different forms

History is littered with stories of investments that appeared to be low risk – until they weren’t. There are always trade-offs for the extra yield, even if they are not immediately obvious. Don’t be fooled by investments offering low-risk opportunities with market-beating yields or returns. Instead, make sure to ask “What’s the catch?”

For example, bank loans are a popular income investment because they have produced a nice yield and seem to have low risk. If we looked at the volatility for bank loans over the last five years, we’d expect to lose 3% or more once every 6 years. If we extrapolate that rate over longer time frames, we’d expect to lose 10% or more once every 330 years. How about losing 30% or more? Try once in a ridiculously large number that has 24 zeroes in it. Yet that’s exactly what happened in 2008. So it could be the case that the risk demonstrated over the past five years may not tell us enough. You need to carefully evaluate the risks you’re taking, over realistic time horizons, to understand both how and when your investments can go wrong.

Conclusion

When it comes to income investing, I stand by the old adage: If it sounds too good to be true it probably is. Being realistic and well-informed about your income and risk goals today can better set you up to reap benefits well past tomorrow.

This article is written by BlackRock.

Disclaimer

This article is for general information only and it does not constitute an offer, recommendation or solicitation of an offer to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments, nor does it constitute any prediction of likely future movements in rates or prices or any representation that any such future movements will not exceed those shown in any illustration. This article has not been prepared for any particular person or class of persons and it has been prepared without regard to the specific investment objectives, financial situation or particular needs of any person, and does not constitute and should not be construed as investment advice nor an investment recommendation. Where the article describes any insurance product or service, it also does not constitute an offer, recommendation or solicitation of an offer to buy or sell any insurance product or service, nor is it intended to provide insurance or financial advice. You should seek advice from a licensed or an exempt financial adviser on the suitability of a product for you, taking into account these factors before making a commitment to purchase any product. In the event that you choose not to seek advice from a licensed or an exempt financial adviser, you should carefully consider whether the product is suitable for you.

Standard Chartered Bank (Singapore) Limited (the “Bank”) will not accept any responsibility or liability of any kind, with respect to the accuracy or completeness of the information herein. The Bank makes no representation or warranty of any kind, express, implied or statutory regarding this article or any information contained or referred to in this article. This article is distributed on the express understanding that, whilst the information in it is believed to be reliable, it has not been independently verified by the Bank.