This is to inform that by clicking on the hyperlink, you will be

leaving

sc.com/sg

and entering a website operated by other parties.

Such links are only provided on our website for the convenience of

the Client and Standard Chartered Bank does not control or endorse

such websites, and is not responsible for their contents.

The use of such website is also subject to the terms of use and

other terms and guidelines, if any, contained within each such

website. In the event that any of the terms contained herein

conflict with the terms of use or other terms and guidelines

contained within any such website, then the terms of use and other

terms and guidelines for such website shall prevail.

*SingPass holders with a MyInfo profile can use MyInfo to automatically fill up the form. By clicking “Next”, you will be re-directed to the MyInfo portal, which is not owned or controlled by Standard Chartered Bank (Singapore) Limited or any member of the Standard Chartered Group (the “Bank”). The Bank bears no liability or responsibility over your usage of the MyInfo portal.

*Please note that MyInfo is temporarily unavailable at the stipulated downtimes:

Mon, Tues, Thurs, Fri, Sat: 5:00AM to 5:30AM. Wed: 2:00AM to 6:00AM. Sun: 2:00AM to 8:30AM

I am an existing Standard Chartered Current/Checking/Savings Account holder

*SingPass holders with a MyInfo profile can use MyInfo to automatically fill up the form. By clicking “Next”, you will be re-directed to the MyInfo portal, which is not owned or controlled by Standard Chartered Bank (Singapore) Limited or any member of the Standard Chartered Group (the “Bank”). The Bank bears no liability or responsibility over your usage of the MyInfo portal.

*Please note that MyInfo is temporarily unavailable at the stipulated downtimes:

Mon, Tues, Thurs, Fri, Sat: 5:00AM to 5:30AM. Wed: 2:00AM to 6:00AM. Sun: 2:00AM to 8:30AM

I am an existing Standard Chartered Current/Checking/Savings Account holder

– Contrary to common perception, the S in environmental, social and governance (ESG) is not too fuzzy to assess in terms of investment risk and opportunity with disclosure approach solidifying for S as much as they are for E and G.

– Bond issuers with the highest S scores show markedly higher excess returns than those with the lowest scores.

– Bond issuers in the top tercile of social scores have tighter spreads than issuers in the bottom tercile.

The COVID-19 pandemic has shone a spotlight on the fragility of the social fabric worldwide, with implications on healthcare access, workplace safety, affordable housing, cybersecurity and other issues related to the communities that businesses operate in.

More institutional investors are starting to track these trails under the social pillar in environmental, social and governance (ESG) as they present both investment risks and opportunities. After all, social responsibility is what mitigates data theft, worker strikes, litigation, workplace accidents, law-enforcement seizure of goods made by forced labour and other people-related disruptions that can hurt a business’ finance and reputation.

While it is commonly believed that social factors are too intangible to assess for investment purposes, an increasing number of credible approaches are emerging.

The Sustainability Accounting Standards Board (SASB), for example, has produced ESG measurement and disclosure methods tailored to 77 major industries ranging from consumer goods to mining using input from both industry players and investors such as the Canadian pension fund Alberta Investment Management Corp, Alibaba, Nike, Moody’s, Chevron, Coca-Cola, among many others. SASB’s social pillar ambit includes customer privacy, data security, customer welfare, selling practices, product labelling, employee health and safety, employee diversity and inclusion, human rights and community relations, just to name a few of the social indicators with potentially material financial impact.

The SASB standards are gaining ground with eight top Canadian pensions representing about C$1.6 trillion in assets under management (AUM) releasing a joint statement in November 2020 to urge companies and investors to provide consistent and complete ESG information. The statement called for the adoption of the SASB standards and the Task Force on Climate-related Financial Disclosures framework. The adoption of common standards will enable investors to more effectively compare ‘apples with apples’ when assessing investment risks and opportunities across the board.

Counting social good

The fact that social integrity can be quantified is borne by companies such as Crown Holdings, a manufacturer of packaging items with headquarters in Singapore, Switzerland and the US. The group has a stewardship programme called Twentyby30 that includes product and employee safety. Crown’s products include packaging for food and beverage items such as tins, caps and closures. The Twentyby30 programme has a target to screen 100% of materials used in food-contact packaging for potentially harmful chemicals by 2025. As an interim step, standards of toxicology, safety and migration across Crown’s global locations will be standardised by 2022.

The group also aims to reduce workplace injuries by 20% by 2025 with concrete steps towards achieving that goal. Working from the ground up, Crown has been standardising data and information collection across its global operations with the aim of analysing safety trends and creating an accurate benchmark to enable informed decisions about which safety aspects need more support and staff training. A software enables plant supervisors to enter relevant information via smartphones which gives the data a real-time perspective. Crown has also created “safety circles”; each with four or five staff from a variety of departments or functions who discuss ways to improve safety and provide suggestions to their plant’s management every quarter.

Workplace injury has significant economic costs involving not just regulatory fines, insurance expense, medical care and litigation but also opportunity costs when incapacitated employees can’t perform their duties over prolonged periods. About 374 million people worldwide suffer from non-fatal occupational injuries every year, while 2.78 million die from work-related hazards and illnesses, according to the International Labour Organization (ILO). In fact, the ILO estimates that weak occupational safety results in economic burdens equivalent to 4% of global Gross Domestic Product (GDP) annually1.

Work-related injuries and deaths have repercussions on families, including their financial security, which has a bearing on the United Nations Sustainable Development Goals (SDGs) of no poverty, zero hunger, good health and well-being, decent work and economic growth. As we mentioned in part one of our ESG series, a growing number of investors are aligned with these goals.

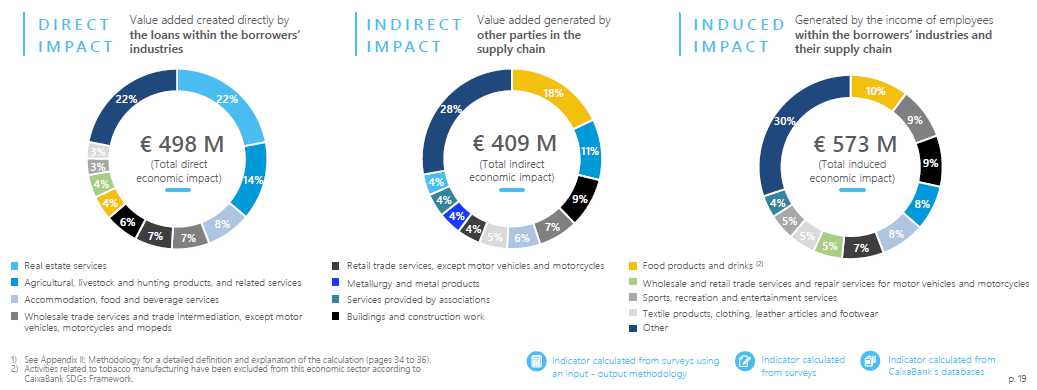

CaixaBank, a Spanish financial institution, has raised EUR1 billion from its social bonds issued in 2019 to positively impact the SDG goals of no poverty, and decent work and economic growth. The proceeds from the five-year notes, rated Baa3/BBB/BBB+ by Moody’s, Standard & Poor’s and Fitch, have been disbursed through 160,945 loans to small-and-medium-sized enterprises, micro businesses, self-employed people and families in the poorest regions of Spain and areas with the highest unemployment.

The bank estimates that every EUR1 million invested in the bond contributes EUR2.79m to GDP. Already, 1,000 new companies and 8,207 jobs have been directly and indirectly created from the loans2. These activities benefited 10 major economic sectors such as real estate, food-and-beverage and retail among others, as the businesses and self-employed individuals who received the loans, as well as the people they employed, enjoyed improved liquidity, according to a survey by CaixaBank (October 2020).

Figure 1: Socially aligned loans’ impact on GDP by sector

Note: Activities related to tobacco manufacturing have been excluded, according to CaixaBank SDG Framework.

Source: CaixaBank, October 2020

The survey shows that 85% of self-employed people who used the loan to start businesses felt that it would not have been possible without financial assistance. They used the funding to invest in technology, business continuity, rent and expansion, among other activities. Among small enterprises, 66% said the loans have helped to strengthen their businesses within 12 months of receiving the loan, while 75% of medium-sized enterprises said the same.

The investment case for social responsibility

Numerous studies have established that ESG-aware companies tend to be sounder investments because they have lower-risk operations, they allocate resources more optimally and they compete more effectively within their sectors.

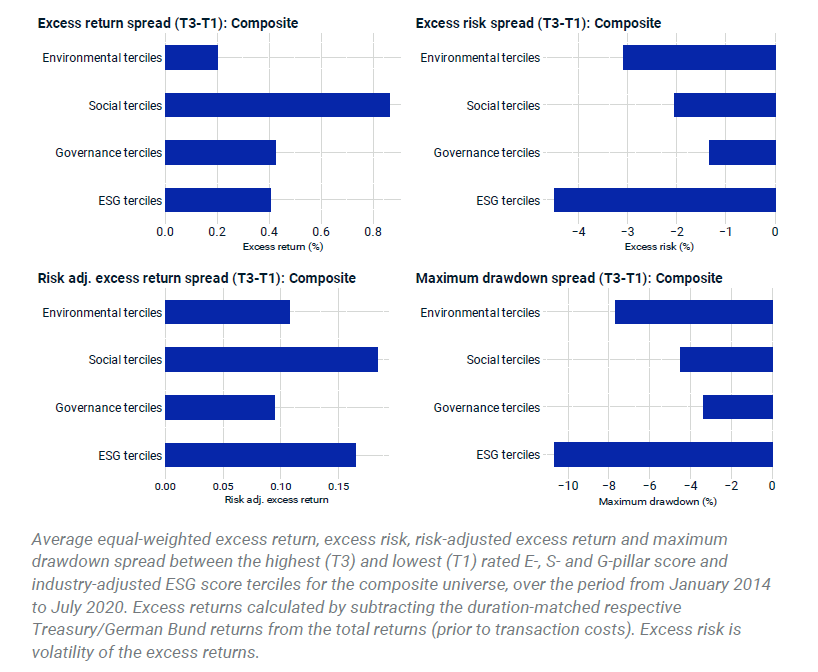

A study by MSCI from data between January 2014 and July 2020 found that corporate bond issuers with high S scores produce markedly higher excess investment returns than issuers with low scores. In terms of risk-adjusted returns and maximum drawdown, the difference between the high and low scorers was less marked but nonetheless notable. The study was published by MSCI in the Foundations of ESG Investing in Corporate Bonds: How ESG Affected Corporate Credit Risk and Performance.

Figure 2: Performance of individual E, S and G pillars

Source: MSCI, November 2020

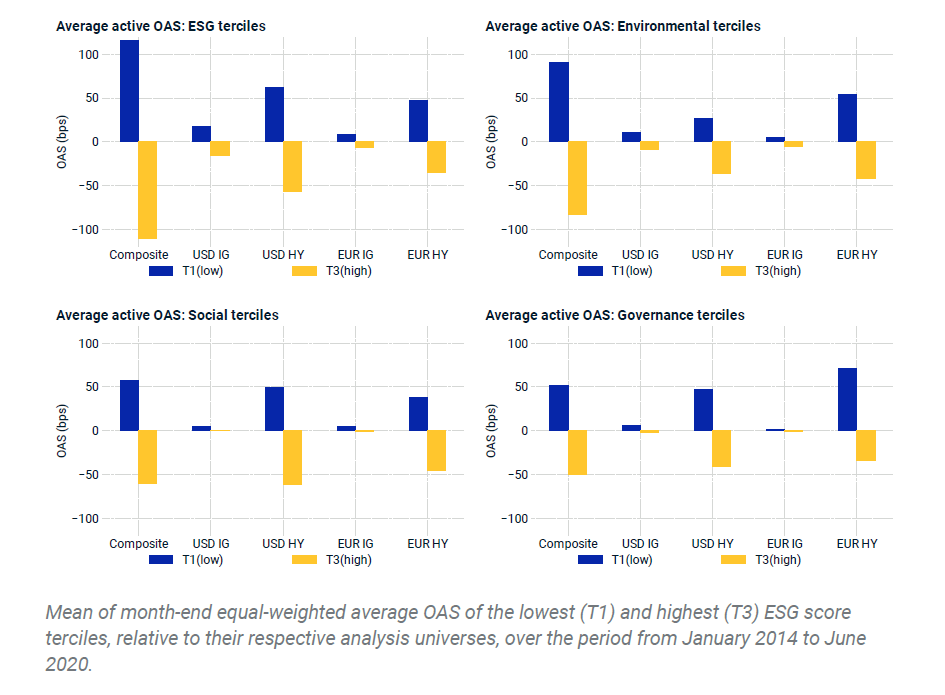

Another way to assess corporate bonds is to look at the difference in the yields of risk-free assets and the bond. This is known as the option-adjusted spread (OAS). The difference in OAS between corporates with high social scores and low scores is substantial, especially in the high-yield space, according to the MSCI study.

Figure 3: Bond spreads of individual E, S and G pillars

Source: MSCI, November 2020

S is catching up with E

Thus far, investors have paid more attention to the E in ESG than to S. This is mainly due to the fact that environmental factors have received more regulatory scrutiny in recent years. It is also relatively straightforward to measure greenhouse gas emissions, pollution and energy consumption. But social dimensions are starting to come to the fore, as evident by public and investors’ increasing attention on issues such as board diversity, cybersecurity, human rights, senior executive remuneration, among other social considerations.

The European Union (EU) is taking the lead by requiring all capital markets participants in the EU, including Undertakings in Collective Investments in Transferable Securities (UCITS) funds to publicly disclose how ESG risks could impact investment returns. All financial products, whether they have a stated ESG focus or not, must make such disclosures or explain their lack of compliance. The draft requirements for disclosing social factors are not significantly less than for environmental or governance aspects. Given the wide adoption of the UCITS structure worldwide including in Singapore, the EU’s Sustainable Finance Disclosure Regulation (SFDR) is far-reaching and may lead to similar regulations in other parts of the world. While the technical details of the SFDR are still being ironed out, the central principle of the regulation is clearly “do not significantly harm”. This is a step in the right direction for protecting both investors and the social fabric that enables businesses to thrive and reward shareholders.

This is the second in a series of articles on the E, S and G aspects of ESG investing. UOBAM became a signatory of the United Nations Principles for Responsible Investment (UNPRI) in January 2020.

This article was written by UOB Asset Management.

References

1International Labour Organization, Guide on sources and uses of statistics on occupational safety and health, October 2020.

2CaixaBank, Social Bond report, October 2020.

3MSCI, Foundations of ESG Investing in Corporate Bonds: How ESG Affected Corporate Credit Risk and Performance. November 2020.

Disclaimer

This article is for general information only and it does not constitute an offer, recommendation or solicitation of an offer to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments. This article has not been prepared for any particular person or class of persons and does not constitute and should not be construed as investment advice or an investment recommendation. It has been prepared without regard to the specific investment objectives, financial situation or particular needs of any person or class of persons. You should seek advice from a licensed or an exempt financial adviser on the suitability of a product for you, taking into account these factors before making a commitment to purchase any product or invest in an investment. In the event that you choose not to seek advice from a licensed or an exempt financial adviser, you should carefully consider whether the product or service described herein is suitable for you.

You are fully responsible for your investment decision, including whether the investment is suitable for you. The products/services involved are not principal-protected and you may lose all or part of your original investment amount. Standard Chartered Bank (Singapore) Limited will not accept any responsibility or liability of any kind, with respect to the accuracy or completeness of information in this article.

Deposit Insurance Scheme

Singapore dollar deposits of non-bank depositors are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law. For clarity, these investment products are not deposits and do not qualify as an insured deposit under the Singapore Deposit Insurance and Policy Owners’ Protection Schemes Act 2011. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured.

The information stated in this article is accurate as at the date of publication.