This is to inform that by clicking on the hyperlink, you will be

leaving

sc.com/sg

and entering a website operated by other parties.

Such links are only provided on our website for the convenience of

the Client and Standard Chartered Bank does not control or endorse

such websites, and is not responsible for their contents.

The use of such website is also subject to the terms of use and

other terms and guidelines, if any, contained within each such

website. In the event that any of the terms contained herein

conflict with the terms of use or other terms and guidelines

contained within any such website, then the terms of use and other

terms and guidelines for such website shall prevail.

*SingPass holders with a MyInfo profile can use MyInfo to automatically fill up the form. By clicking “Next”, you will be re-directed to the MyInfo portal, which is not owned or controlled by Standard Chartered Bank (Singapore) Limited or any member of the Standard Chartered Group (the “Bank”). The Bank bears no liability or responsibility over your usage of the MyInfo portal.

*Please note that MyInfo is temporarily unavailable at the stipulated downtimes:

Mon, Tues, Thurs, Fri, Sat: 5:00AM to 5:30AM. Wed: 2:00AM to 6:00AM. Sun: 2:00AM to 8:30AM

I am an existing Standard Chartered Current/Checking/Savings Account holder

*SingPass holders with a MyInfo profile can use MyInfo to automatically fill up the form. By clicking “Next”, you will be re-directed to the MyInfo portal, which is not owned or controlled by Standard Chartered Bank (Singapore) Limited or any member of the Standard Chartered Group (the “Bank”). The Bank bears no liability or responsibility over your usage of the MyInfo portal.

*Please note that MyInfo is temporarily unavailable at the stipulated downtimes:

Mon, Tues, Thurs, Fri, Sat: 5:00AM to 5:30AM. Wed: 2:00AM to 6:00AM. Sun: 2:00AM to 8:30AM

I am an existing Standard Chartered Current/Checking/Savings Account holder

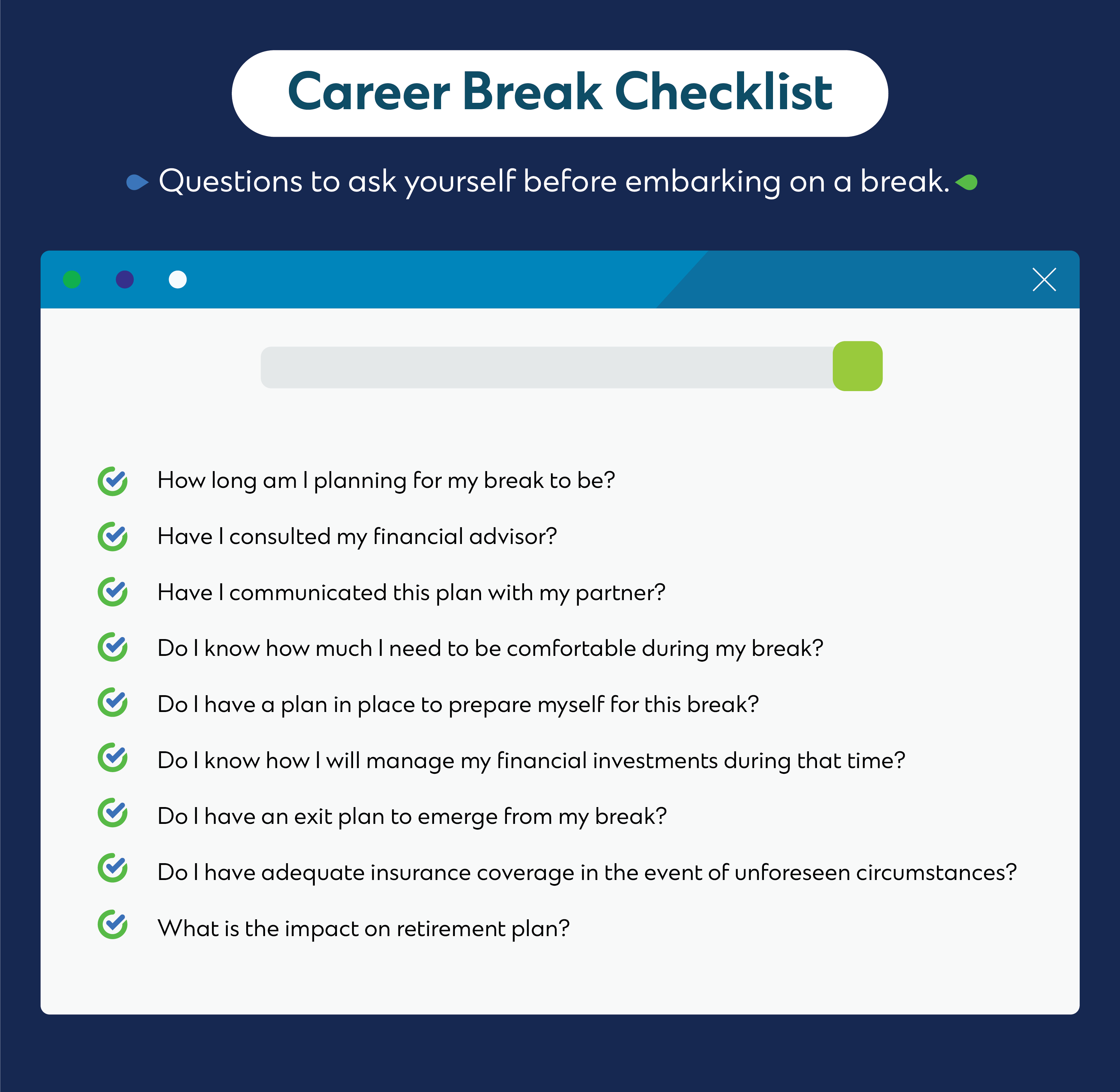

What should you do before you decide on a mid-career break?

This article is for information only.

Burnout is real. And many working women are feeling it.

One of the lessons learnt from living with COVID-19 has been the need to acknowledge the mental toll on working women. From increased childcare due to remote learning in the early days of COVID-19, to bearing primary responsibility for household chores and the care of ageing parents

Time for a hard reset

An emerging trend is the increasing number of working adults who are putting their careers on pause. A study from the Institute for Women’s Policy Research found that more than 40 percent of women take at least one year off—almost twice the number of men who do. One reason women are taking time off at a greater rate has to do with remote work: a survey by the National University Health System’s (NUHS) Mind Science Centre found that 61 percent of remote workers reported feeling stressed compared to those who worked in the office. Women were more likely than men to report feeling stressed.

The idea of hitting pause on your career can be tough

With the demands and satisfactions of work and life in a constant balancing act, it can be hard to even imagine taking a breather from one’s full-time jobs. Professionals who have invested years in building their careers may be understandably reluctant to step on the brake pedal. Others feel that they simply cannot afford to stop working for any amount of time. However, the challenges of the last three years have shown that self-care is an essential component of every professional’s arsenal and yet there is still a lot of uncertainty around how to start preparing for a career break and how much money is “enough” to get you through.

Start at the beginning

Before you consider a career break, you need to be financially ready for it.

First assess the impact of your loss of income, for example do you need to cut down on your lifestyle activities. If you have a trusted financial advisor, speak with him or her to understand the impact of a career break on your portfolio, and vice-versa. You will also need to understand the impact of your temporary loss of income on your long-term investment premiums. Those who manage their money independently can explore online tools such as SC Goals Planner, which helps to plan and track your financial goals through real life simulations of situations that include unemployment. To give you a better idea of what you can expect, SC Goals Planner can also be adjusted to account for the period of time you will be out of employment.

Next, determine how much you need in your “career break fund”. It will depend on your current state of financial health, your recurring payments such as your mortgage and insurance premiums, the needs of your dependents if you have any,and the duration of your break.

Build up your career break fund

Once you have worked out how much you need, you can start building this fund. While regular savings help, consider investing in income yielding unit funds, which provide a regular cash income stream from your investments over a period of time. Reinvesting the regular cash income you receive will then enable you to purchase more units, ultimately increasing your unit trust portfolio.

When thinking about your investment strategy, remember diversification is key. The income portfolio will benefit from broad diversification across asset classes, geographies and sectors. Having multiple income streams will also help your portfolio to deliver income across different market conditions.

Be prepared in case of emergency

You should have at least six months’ worth of expenses in your emergency fund. And it should be used for unexpected expenses, not your day-to-day expenses. While some women in dual-income families may not require this buffer, it may help with peace of mind once their career break has begun.

In fact, data from SC Goals Planner found that the majority of female users made it a habit to put more than 20 percent of their income away in savings – 55% of women aged between 35 to 44 years old saved more than 40% of their income. Being able to enjoy and thrive during your mid-career break requires a longer runway of planning and ultimately,

Ensure you are protected, come what may

Your current employer may cover some of your health care costs. However, these benefits will lapse once you leave your job.

Assess any gaps that may appear while you are out of the rat race, including medical expense insurance, hospital cash insurance, critical illness insurance, disability income insurance, long-term care insurance and personal accident insurance. Once you identify your gaps, you can proceed to develop a plan to fill them. Health and protection insurance are important pillars you need to include as part of your career break checklist. While no one wants the unexpected to happen while focusing on recharging, it is best to be prepared for the unforeseen, so as to protect your savings and wealth.

The challenges of professional life are real, and the COVID-19 pandemic has pushed too many to drastic measures – hence the Great Resignation. By giving yourself permission to pause your career, you can protect yourself and your loved ones from the impact of burnout. And by making your financial preparations beforehand, you will be able to make the best of your much-needed break.

After all, there’s not a whole lot of life you can enjoy or fix if you don’t have the means to make it happen.

Disclaimer

This article is for general information only and it does not constitute an offer, recommendation or solicitation of an offer to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments. This article has not been prepared for any particular person or class of persons and does not constitute and should not be construed as investment advice or an investment recommendation. It has been prepared without regard to the specific investment objectives, financial situation or particular needs of any person or class of persons. You should seek advice from a licensed or an exempt financial adviser on the suitability of a product for you, taking into account these factors before making a commitment to purchase any product or invest in an investment. In the event that you choose not to seek advice from a licensed or an exempt financial adviser, you should carefully consider whether the product or service described herein is suitable for you.

You are fully responsible for your investment decision, including whether SC Online Trading and Online UT platform are suitable for you. The products/services involved are not principal-protected and you may lose all or part of your original investment amount. Standard Chartered Bank (Singapore) Limited will not accept any responsibility or liability of any kind, with respect to the accuracy or completeness of information in this article.

Deposit Insurance Scheme

Singapore dollar deposits of non-bank depositors are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law. For clarity, these investment products are not deposits and do not qualify as an insured deposit under the Singapore Deposit Insurance and Policy Owners’ Protection Schemes Act 2011. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured.

The information stated in this article is accurate as at the date of publication.