This is to inform that by clicking on the hyperlink, you will be

leaving

sc.com/sg

and entering a website operated by other parties.

Such links are only provided on our website for the convenience of

the Client and Standard Chartered Bank does not control or endorse

such websites, and is not responsible for their contents.

The use of such website is also subject to the terms of use and

other terms and guidelines, if any, contained within each such

website. In the event that any of the terms contained herein

conflict with the terms of use or other terms and guidelines

contained within any such website, then the terms of use and other

terms and guidelines for such website shall prevail.

*SingPass holders with a MyInfo profile can use MyInfo to automatically fill up the form. By clicking “Next”, you will be re-directed to the MyInfo portal, which is not owned or controlled by Standard Chartered Bank (Singapore) Limited or any member of the Standard Chartered Group (the “Bank”). The Bank bears no liability or responsibility over your usage of the MyInfo portal.

*Please note that MyInfo is temporarily unavailable at the stipulated downtimes:

Mon, Tues, Thurs, Fri, Sat: 5:00AM to 5:30AM. Wed: 2:00AM to 6:00AM. Sun: 2:00AM to 8:30AM

I am an existing Standard Chartered Current/Checking/Savings Account holder

*SingPass holders with a MyInfo profile can use MyInfo to automatically fill up the form. By clicking “Next”, you will be re-directed to the MyInfo portal, which is not owned or controlled by Standard Chartered Bank (Singapore) Limited or any member of the Standard Chartered Group (the “Bank”). The Bank bears no liability or responsibility over your usage of the MyInfo portal.

*Please note that MyInfo is temporarily unavailable at the stipulated downtimes:

Mon, Tues, Thurs, Fri, Sat: 5:00AM to 5:30AM. Wed: 2:00AM to 6:00AM. Sun: 2:00AM to 8:30AM

I am an existing Standard Chartered Current/Checking/Savings Account holder

December to March is a time when retailers tend to get excited. The reason? The much-anticipated year-end bonus often leads to spending sprees. For those who are receiving their bonus for the first-time this year, it can be exhilarating to get one or more months of your salary. However, this also carries the risk of being swept away with exuberance and wiping out your bonus on impulse buys. Today, we will talk about how to make that bonus last longer than the next 60 days. But before that, let us look at some of the reasons why this bonus doesn’t last long:

Things to look out for when spending your bonus

Whether it is your first time receiving a bonus, or you have come to expect it over the years, there are some common trends that do not allow individuals to use their bonuses properly and for a longer term.

1. Overindulging – If you are new to the workforce, or have never received a big bonus before, it is easy to get swept up with the possibilities. Young adults grapple with having a heap of money and being able to buy whatever they want – an exhilarating release from the days of controlled allowances.

Older workers may use the bonus as a stress release valve. If you have had a tough year, some retail therapy may be the best therapy. While you can allow for some indulgences, it is imprudent to squander the entire bonus – especially if you have existing debt or may have foreseeable expenses in the coming year. For instance, getting married, moving to a new home, or children’s enrichment classes.

Rather than go on uncontrolled spending sprees, try to practice conscious spending: budget for a reasonable number of indulgences, and no more. This helps to ensure the next 12 months – and not just Christmas or New Year – can go smoothly.

As an added benefit, conscious spending ensures you spend on the things you really want, rather than impulsive spending on overpriced meals, lavish parties, vacations, unnecessary cab rides, etc. It can be quite painful to realize you have spent your entire bonus, and still have not been able to buy the things you wanted.

2. Paying too much to get the goods – Christmas and New Year often bring a rise in “convenience costs”. Examples of this include paying for express shipping, to get your gifts on time. Depending on the courier, express or overnight shipping could raise the cost of delivery to almost double the usual rate.

Some companies may also use artificial scarcity, to raise costs. It’s long been known that toy companies, for instance, sometimes create undersupply around Christmas.

This may get you to “double buy”. This is when you buy a cheaper substitute during Christmas, and then buy the actual item when it’s in stock again come January to March. Otherwise, it may involve paying higher costs on a secondary market, such as eBay, just to secure a much-wanted item. Try to order your items earlier in the year, rather than end up burning your year-end bonus on these added costs.

3. Not using it to manage debt – If you have high-interest loans, such as personal loans and credit card outstanding balance, your priority should be to pay them off as soon as possible. This is where your bonus should go. Ignoring to pay down your loan will result in you incurring additional fees because of the high interest rates. Besides, relief from debt-driven anxiety can be as much a reward, if not more so, than just another shopping spree.

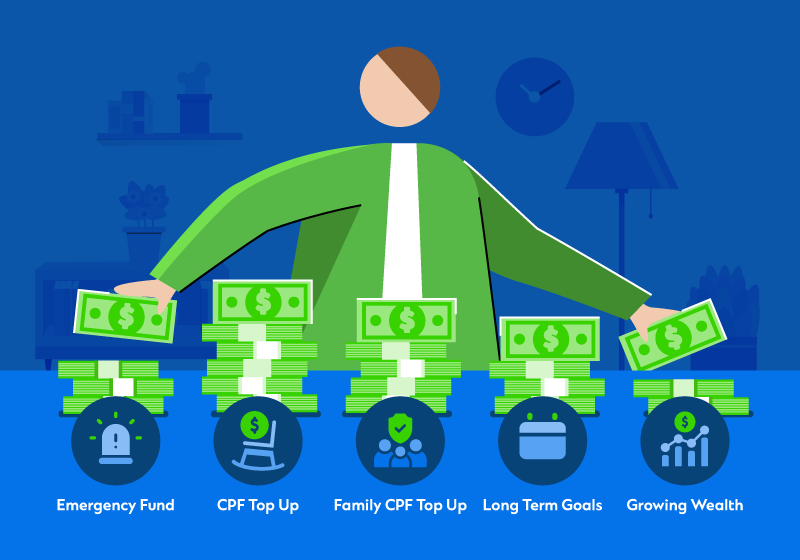

Smarter ways you can use your bonus

Take your bonus further by:

1. Starting or topping up an emergency fund – Avoid living pay cheque-to-pay cheque. When you have no savings, any financial emergency can cause undue hardship. You may also be forced to resort to high-interest debt, such as personal loans, if you have no funds in an emergency. A good way to use your bonus is to add to an emergency fund, which might be anywhere from three to six months of your monthly expenses.

2. Use it to reach specific financial goals – Your bonus can be used in short to mid-term savings plans, such as five to 10 years. These plans can be useful for a specific financial target, such as to pay for down payment for your first home – to fund your child’s tertiary education. Repaying debt is also a viable financial goal.

Do speak to an investment expert before picking one; the right product will depend on the time horizon, and the amount you are willing to set aside for it.

3. Top up your CPF for better security – Putting your bonus in your CPF may not sound terribly exciting right now. However, consider the peace of mind this can give you. Your CPF Ordinary Account (OA) can be used to pay for your home, and to service the monthly home loan. Your Medisave Account (MA) can pay for private healthcare, beyond MediShield Life; and your Retirement Account (RA) can provide absolute returns of four per cent per annum, regardless of market conditions.

If you do not mind committing the money for the long term, your CPF could provide better returns, compared to just keeping the money in a savings account. However, you must ensure that you have sufficient cash in savings- as contingency, since you would not be able to withdraw your CPF monies until your draw down age of 55.

4. Use it to support your family – Older Singaporeans may have depleted more of their CPF over time. As such, another smart way to use your bonus is to top up your family’s CPF account. This is useful if you have elderly parents, who might not have accumulated as much in their CPF.

This is a move that also helps you in the long run. When your parents are better provided for, it is also a relief on your own finances. You won’t have overstretched your funds when you are in your 50’s or 60’s, for instance, if you are still supporting your surviving parents then. You also enjoy tax savings when you top up their CPF accounts.

5. Invest it to grow your wealth – By investing in a long-term savings plan, you can channel your bonus into something that will benefit you for the rest of your life, not just a single holiday season. Your bonus can be the foundation of your first investment portfolio, for instance, which can be used to accrue wealth for retirement. It is smart to invest with a purpose.

If you already have an investment portfolio, your bonus can be used to seize investment opportunities that may not have been there earlier. As a nice coincidence, the start of a new year is also when most investors need to review their assets and decide on how to rebalance their portfolio. Sometimes, a bit of your bonus can help to accelerate your returns or make up for any underperformance in the previous year.

A bonus is a testament to a job well-done

Ultimately, your efforts and skills deserve more than just one good holiday season! Channel your bonus towards the long-term financial security that you and your family deserve, for all your hard work. This does not mean you can’t enjoy any of your bonuses right away; simply control the amount you use, such as spending only 20 percent of the bonus, and saving or investing the rest. This can pay off in bigger ways later, such as saving you from debt burdens, and ensuring you meet major financial aspirations.

Speak to our branch sales and service executives at Standard Chartered Bank, to find tailor-made solutions that optimise your earnings.

Disclaimer

This article is for general information only and it does not constitute an offer, recommendation or solicitation of an offer to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments. This article has not been prepared for any particular person or class of persons and does not constitute and should not be construed as investment advice or an investment recommendation. It has been prepared without regard to the specific investment objectives, financial situation or particular needs of any person or class of persons. You should seek advice from a licensed or an exempt financial adviser on the suitability of a product for you, taking into account these factors before making a commitment to purchase any product or invest in an investment. In the event that you choose not to seek advice from a licensed or an exempt financial adviser, you should carefully consider whether the product or service described herein is suitable for you.

You are fully responsible for your investment decision, including whether the investment is suitable for you. The products/services involved are not principal-protected and you may lose all or part of your original investment amount. Standard Chartered Bank (Singapore) Limited will not accept any responsibility or liability of any kind, with respect to the accuracy or completeness of information in this article.

Deposit Insurance Scheme

Singapore dollar deposits of non-bank depositors are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law. For clarity, these investment products are not deposits and do not qualify as an insured deposit under the Singapore Deposit Insurance and Policy Owners’ Protection Schemes Act 2011. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured.

The information stated in this article is accurate as at the date of publication.