This is to inform that by clicking on the hyperlink, you will be

leaving

sc.com/sg

and entering a website operated by other parties.

Such links are only provided on our website for the convenience of

the Client and Standard Chartered Bank does not control or endorse

such websites, and is not responsible for their contents.

The use of such website is also subject to the terms of use and

other terms and guidelines, if any, contained within each such

website. In the event that any of the terms contained herein

conflict with the terms of use or other terms and guidelines

contained within any such website, then the terms of use and other

terms and guidelines for such website shall prevail.

*SingPass holders with a MyInfo profile can use MyInfo to automatically fill up the form. By clicking “Next”, you will be re-directed to the MyInfo portal, which is not owned or controlled by Standard Chartered Bank (Singapore) Limited or any member of the Standard Chartered Group (the “Bank”). The Bank bears no liability or responsibility over your usage of the MyInfo portal.

*Please note that MyInfo is temporarily unavailable at the stipulated downtimes:

Mon, Tues, Thurs, Fri, Sat: 5:00AM to 5:30AM. Wed: 2:00AM to 6:00AM. Sun: 2:00AM to 8:30AM

I am an existing Standard Chartered Current/Checking/Savings Account holder

*SingPass holders with a MyInfo profile can use MyInfo to automatically fill up the form. By clicking “Next”, you will be re-directed to the MyInfo portal, which is not owned or controlled by Standard Chartered Bank (Singapore) Limited or any member of the Standard Chartered Group (the “Bank”). The Bank bears no liability or responsibility over your usage of the MyInfo portal.

*Please note that MyInfo is temporarily unavailable at the stipulated downtimes:

Mon, Tues, Thurs, Fri, Sat: 5:00AM to 5:30AM. Wed: 2:00AM to 6:00AM. Sun: 2:00AM to 8:30AM

I am an existing Standard Chartered Current/Checking/Savings Account holder

Planning and investing for retirement can sometimes seem overwhelming, but it doesn’t need to. A simple process, which we refer to as goals-based investing, can help you every step along the way.

At any age, young, near retirement, or somewhere in between, you are likely to have several different financial goals. Often these goals may compete with one another. For example, you may want to buy a home this year and send your child abroad for college in two years, but you also aim to retire in 20 years and want to be sure you have enough funds set aside. How can you plan so that you are successful in meeting the goals that are most important to you—and not just drift from year to year, paying whatever expenses that come along and hoping that your nest egg will be there when you need it?

The answer is to plan for your long-term and short-term goals together and follow a goals-based investing approach. This process can be helpful:

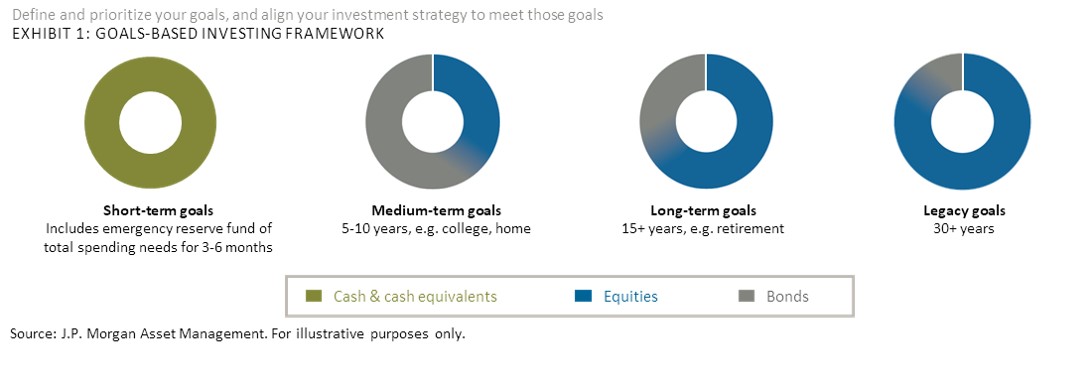

Define your goals clearly (when will they start, how long will they last and how much will they cost) and divide them into different buckets based on their time horizons: for example, paying for a child’s college expenses, buying a home, retirement and legacy planning.

Prioritize your goals: You may not be able to afford it all—setting your priorities can help you determine if trade-offs need to be made. Decide how much of your current assets and future savings to put towards your different goals based on their relative importance. If your child’s education is a top priority, are you willing to delay your retirement or spend less in retirement if needed? Often trade-offs must be made.

Align your investment strategy by goal, based on risk tolerance and the investment horizon, so that you can use time to your advantage.

For your short-term goals, you need liquidity, and that means cash, as it allows flexible access to your money and is not subject to the volatility of the market. You need cash to cover any emergencies and pay for upcoming large expenses without the risk of having to sell your investments at inopportune times.

For your longer-term goals, you have time to take more risk and weather market cycles. In general, the more distant your goal, the more risk you can take to seek higher return. As Exhibit 1 illustrates, someone 15 years from retirement can have quite a high allocation to equities (shown in blue) because over the long term, volatility is less of a concern.

This is what we call goals-based investing, and it can help you be more disciplined by giving you a mental accounting framework to plan your finances. This approach draws on a powerful behavioral finance concept: rules can influence behavior. Studies have suggested that when people segregate their money into separate accounts for different purposes they are less likely to spend that money for “unselected” purposes. This is because dipping into those accounts for an unrelated expense would effectively violate a rule, triggering a sense of guilt that would in turn make one think twice before acting. Some studies have shown that using a photo of the savings goals as a visual reminder can reinforce that sense of guilt.

Understand that there are trade-offs between spending today and meeting your goals for the future. For example, if you choose to fund your child’s wedding from your retirement account, keep in mind that eventually you will need to either replace that money or expect to spend less in retirement. Withdrawing, say, SGD 50,000 from your retirement fund may seem a modest amount relative to your retirement nest egg. However, with the compounding of interest over time, the growth of this SGD 50,000 may mean an additional SGD 4,0001 per year for you to spend in retirement. You may decide that spending that SGD 50,000 on your child’s wedding now, and thus potentially sacrificing the annual SGD 4,000 in additional retirement income, is a reasonable trade-off, but it is important to make an informed choice about both goals. You don’t want to ignore the initial trade-off and be forced to live with the consequences decades later.

Using goals-based investing, it becomes clear which goals have a shorter vs. longer time horizon. That’s important, because you can use the time that you have for your long-term goals to make your savings work harder for you. This approach makes sure that you don’t put everything in cash and lose out on the opportunity to let your savings grow to meet your long-term goals. Investing only in cash can make your long-term goals more costly to you because you will need to save more to reach your goal. Instead, by saving longer and at a higher return, you can make accomplishing your long-term goals less costly.

Retirement, of course, is a critical long-term goal. As we explain in the following sections, to reach this goal, you need to get invested, diversify and stay invested in long-term growth assets.

This article is written by J.P. Morgan Asset Management.

Footnote:

1This is based on the assumption that the amount of SGD 50,000 is withdrawn 10 years prior to retirement. If instead of being withdrawn, this SGD 50,000 is invested at 5.5% average returns per annum, the investment will grow to SGD 85,000 at retirement, providing SGD 4,000 per annum for 30 years in retirement.

Disclaimer

This article is for general information only and it does not constitute an offer, recommendation or solicitation of an offer to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments. This article has not been prepared for any particular person or class of persons and does not constitute and should not be construed as investment advice or an investment recommendation. It has been prepared without regard to the specific investment objectives, financial situation or particular needs of any person or class of persons. You should seek advice from a licensed or an exempt financial adviser on the suitability of a product for you, taking into account these factors before making a commitment to purchase any product or invest in an investment. In the event that you choose not to seek advice from a licensed or an exempt financial adviser, you should carefully consider whether the product or service described herein is suitable for you.

You are fully responsible for your investment decision, including whether the investment is suitable for you. The products/services involved are not principal-protected and you may lose all or part of your original investment amount. Standard Chartered Bank (Singapore) Limited will not accept any responsibility or liability of any kind, with respect to the accuracy or completeness of information in this article.

Deposit Insurance Scheme

Singapore dollar deposits of non-bank depositors are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law. For clarity, these investment products are not deposits and do not qualify as an insured deposit under the Singapore Deposit Insurance and Policy Owners’ Protection Schemes Act 2011. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured.

The information stated in this article is accurate as at the date of publication.