This is to inform that by clicking on the hyperlink, you will be

leaving

sc.com/sg

and entering a website operated by other parties.

Such links are only provided on our website for the convenience of

the Client and Standard Chartered Bank does not control or endorse

such websites, and is not responsible for their contents.

The use of such website is also subject to the terms of use and

other terms and guidelines, if any, contained within each such

website. In the event that any of the terms contained herein

conflict with the terms of use or other terms and guidelines

contained within any such website, then the terms of use and other

terms and guidelines for such website shall prevail.

*SingPass holders with a MyInfo profile can use MyInfo to automatically fill up the form. By clicking “Next”, you will be re-directed to the MyInfo portal, which is not owned or controlled by Standard Chartered Bank (Singapore) Limited or any member of the Standard Chartered Group (the “Bank”). The Bank bears no liability or responsibility over your usage of the MyInfo portal.

*Please note that MyInfo is temporarily unavailable at the stipulated downtimes:

Mon, Tues, Thurs, Fri, Sat: 5:00AM to 5:30AM. Wed: 2:00AM to 6:00AM. Sun: 2:00AM to 8:30AM

I am an existing Standard Chartered Current/Checking/Savings Account holder

*SingPass holders with a MyInfo profile can use MyInfo to automatically fill up the form. By clicking “Next”, you will be re-directed to the MyInfo portal, which is not owned or controlled by Standard Chartered Bank (Singapore) Limited or any member of the Standard Chartered Group (the “Bank”). The Bank bears no liability or responsibility over your usage of the MyInfo portal.

*Please note that MyInfo is temporarily unavailable at the stipulated downtimes:

Mon, Tues, Thurs, Fri, Sat: 5:00AM to 5:30AM. Wed: 2:00AM to 6:00AM. Sun: 2:00AM to 8:30AM

I am an existing Standard Chartered Current/Checking/Savings Account holder

This article is an educational piece about the potential end to the decades-long bond bull market. For informational purposes only.

There has been much talk about the recent sharp rise in interest rates across the world, raising concerns that the decades-long bull run for bonds may finally be over. While interest rates have risen largely due to current high levels of inflation, this pressure is expected to gradually abate as fiscal impetus fades and supply-chains return to normalcy. Given that rates are rising from extremely low levels, every blip higher amplifies the move and attracts heightened attention.

Just because interest rates are low, it does not mean it will rise significantly and on a sustained basis. It is important to remind ourselves why interest rates are this low in the first place, and that many of the key drivers, such as debt levels, ageing demographics and deflationary pressure from disruptive technology are still with us today and will be in the foreseeable future. In the near-term, interest rates can be expected to rise further from here but eventually, these same structural forces will likely reassert themselves again to drive interest rates back down.

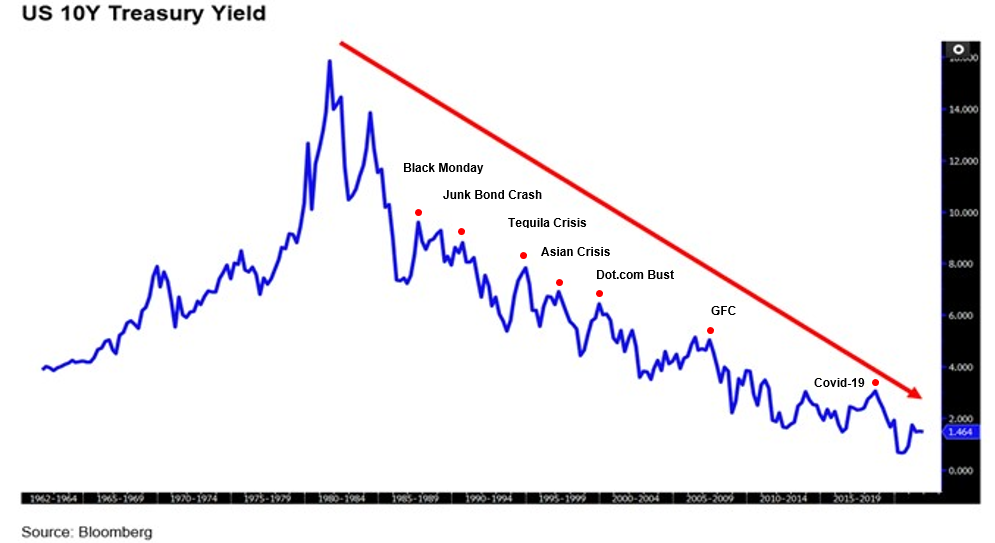

Bond yields tracking lower for decades

Since peaking in the early 1980s, interest rates have tracked lower and lower as crisis after crisis hit economies and markets. Driven by the fear of economic fallout and contagion, governments are compelled to enact bailouts while central banks are forced to cut rates. A quick look at the United States’ 10-year Treasury Yield shows this extremely consistent pattern of lower yields after each crisis over the past four decades.

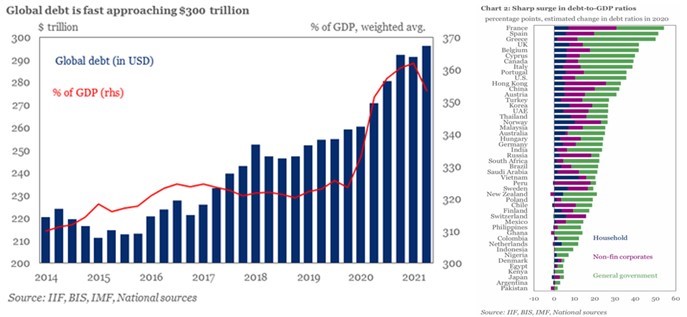

Governments are now leading the global debt binge

The systematic response to every crisis has driven an incremental rise in global debt levels. According to the Institute of International Finance, the total global debt hit another all-time high in the second quarter of 2021 to USD296 trillion or 353% in debt-to-GDP ratio, driven by a massive USD36 trillion rise over 18 months from onset of the pandemic crisis¹.

Unlike the past where households or the corporate sector led the debt binge, governments have now taken over as the main drivers of debt growth. Since governments’ debts are now substantially larger than ever before, it is their prerogative to keep interest rates low to cap interest expense as minimal as possible. Higher interest expense could strain a government’s finances and lead to instability within its financial system which would negatively impact its economy.

This is where the central banks step in. They are responsible for monetary policies which support the economic and financial stability of their country, and one such policy is to keep interest rates low. Given that a debtor will always prefer the lowest borrowing rate possible, one can expect the trend of lower interest rates to continue.

US fiscal and monetary policies will be important

It is important to focus on US monetary policy since the US’ 10-year Treasury Yield is the global defacto risk-free rate for which all financial assets are priced against. Data by the Federal Reserve Bank of St. Louis shows that pandemic-related fiscal spending has driven the US government’s debt levels sharply higher to over USD$28 trillion or 125% in debt-to-GDP ratio² – a figure which will rise further with the passage of the USD$1.2 trillion infrastructure package and soon to be followed by the USD1.75 trillion “Build Back Better” spending plan³. This high debt-to-GDP ratio is a major concern as a study by the World Bank found that when this ratio exceeds 77% for prolonged periods of time, countries will experience significant slowdowns in economic growth⁴.

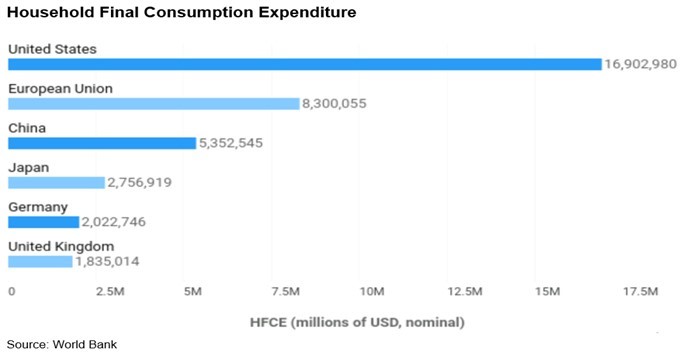

With the ever-growing mountain of debt, the US government can ill-afford interest rates to rise too high or else debt servicing will become a major issue. A sharper rise in interest rates could also stall the fragile recovery and drive the economy back towards recession, especially in one where consumer spending contributes a significant 70% of GDP, and higher interest rates tend to curtail consumption. A consumer-led recession in US consumption will also be felt globally as the US consumer market is by far the largest in the world⁵. And as history has shown us numerous times over the past decades, interest rates will fall when recession hits.

Debt burden to drive US on similar path as Japan and Europe

In the early 1990s following the bursting of the bubble in Japan, interest rates not only decreased but it went into negative territory as the Bank of Japan (BOJ) enacted quantitative easing (QE). QE is an unconventional monetary policy where the central bank purchases long-term securities from the market to boost money supply and lower interest rates to stoke economic activity and growth. After decades of QE which continues to this day, Japan is still combating anaemic growth and deflationary pressures resulting in a government deficit that currently stands at 266% in debt-to-GDP ratio – the highest among developed economies⁶.

Following the Global Financial Crisis and European Sovereign Crisis, this ultra-loose monetary policy and the immense build-up of debt has been copied by the European Central Bank (ECB) and European governments in 2015 in their fight against persistent stagnation and deflation, low-growth and low-inflation economy. And similar to Japan, these policies remain intact in Europe to this day, and both economies are stuck in a negative interest rate environment.

As the saying goes, “one is a once-off, two is a trend, three is a pattern”. It looks highly likely that the US will follow the same policy path as the BOJ and ECB because once one embarks on the path of debt binging, it becomes an addiction that is extremely difficult to wean off.

History is a great teacher

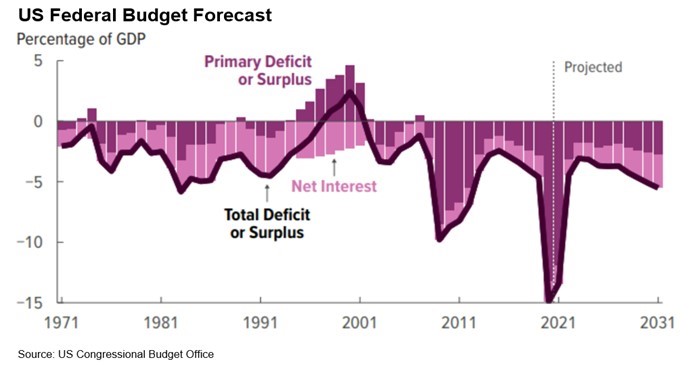

There are a few ways to address a massive debt problem. One can choose to either default, decrease, or defer the debt. For the US government, defaulting is out of the question and decreasing the debt would be a near impossibility as an austerity drive to cut spending will be required. Over the past two decades, the US government has spent much more than it earned and according to the US Congressional Budget Office’s forecast, it is likely this will continue over the next decade⁷. As history has shown us, any reduction in spending will likely lead to an economic contraction and the remedy is often even more debt-funded spending.

This leaves deferring the debt as the only viable option. All the US government needs to do is to continue servicing its debt obligations by ensuring interests due are paid. And the way to do this is to keep interest rates as low as possible and for as long as possible. This should be easy to do since the US Dollar is a leading global reserve currency (as are the Euro and Japanese Yen) and the US Federal Reserve can simply print more dollars and set interest rates accordingly.

“History is a great teacher” – since the least painful and most viable monetary policy going forward for both the US government and its central bank is to keep interest rates at ultra-low levels and possibly even negative (and can likely do so for decades as seen in Japan and Europe), the bond bull market is far from dead as ever lower bond yields will only drive bond prices higher.

About the writer

Prior to venturing into wealth advisory, Jamie was an equity sales trader for two decades covering global financial markets and servicing both institutional and retail clients. Having seen many market cycles, booms and busts, a key lesson that Jamie learnt is to never underestimate human ingenuity and its ability to adapt, improvise and overcome. Jamie hopes he can help to free the mind of others on the complexities and inter-connectedness of the financial markets, just like Morpheus in the Matrix movies.

This article is for general information only and it does not constitute an offer, recommendation, or solicitation of an offer to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments.

This article has not been prepared for any particular person or class of persons and does not constitute and should not be construed as investment advice or an investment recommendation. It has been prepared without regard to the specific investment objectives, financial situation or particular needs of any person or class of persons.

You should seek advice from a licensed or an exempt financial adviser on the suitability of a product for you, taking into account these factors before making a commitment to purchase any product or invest in an investment. In the event that you choose not to seek advice from a licensed or an exempt financial adviser, you should carefully consider whether the product or service described herein is suitable for you.

You are fully responsible for your investment decision, including whether the investment is suitable for you. The products/services involved are not principal-protected and you may lose all or part of your original investment amount. Standard Chartered Bank (Singapore) Limited will not accept any responsibility or liability of any kind, with respect to the accuracy or completeness of information in this article.

This document is being distributed for general information only and is subject to the relevant disclaimers available here. It is not and does not constitute research material, independent research, an offer, recommendation or solicitation to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments.

This document is for general evaluation only. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person or class of persons and it has not been prepared for any particular person or class of persons. You should not rely on any contents of this document in making any investment decisions. Before making any investment, you should carefully read the relevant offering documents and seek independent legal, tax and regulatory advice. In particular, we recommend you to seek advice regarding the suitability of the investment product, taking into account your specific investment objectives, financial situation or particular needs, before you make a commitment to purchase the investment product.

Opinions, projections and estimates are solely those of SCB at the date of this document and subject to change without notice. Past performance is not indicative of future results and no representation or warranty is made regarding future performance. Any forecast contained herein as to likely future movements in rates or prices or likely future events or occurrences constitutes an opinion only and is not indicative of actual future movements in rates or prices or actual future events or occurrences (as the case may be). This document must not be forwarded or otherwise made available to any other person without the express written consent of the Standard Chartered Group (as defined below).

Standard Chartered Bank is incorporated in England with limited liability by Royal Charter 1853 Reference Number ZC18. The Principal Office of the Company is situated in England at 1 Basinghall Avenue, London, EC2V 5DD. Standard Chartered Bank is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and Prudential Regulation Authority. Standard Chartered PLC, the ultimate parent company of Standard Chartered Bank, together with its subsidiaries and affiliates (including each branch or representative office), form the Standard Chartered Group. Standard Chartered Private Bank is the private banking division of Standard Chartered. Private banking activities may be carried out internationally by different legal entities and affiliates within the Standard Chartered Group (each an “SC Group Entity”) according to local regulatory requirements. Not all products and services are provided by all branches, subsidiaries and affiliates within the Standard Chartered Group.

Market Abuse Regulation (MAR) Disclaimer Banking activities may be carried out internationally by different branches, subsidiaries and affiliates within the Standard Chartered Group according to local regulatory requirements. Opinions may contain outright “buy”, “sell”, “hold” or other opinions. The time horizon of this opinion is dependent on prevailing market conditions and there is no planned frequency for updates to the opinion. This opinion is not independent of Standard Chartered Group’s trading strategies or positions. Standard Chartered Group and/or its affiliates or its respective officers, directors, employee benefit programmes or employees, including persons involved in the preparation or issuance of this document may at any time, to the extent permitted by applicable law and/or regulation, be long or short any securities or financial instruments referred to in this document or have material interest in any such securities or related investments. Therefore, it is possible, and you should assume, that Standard Chartered Group has a material interest in one or more of the financial instruments mentioned herein. Please refer to https://www.sc.com/en/banking-services/market-disclaimer.html for more detailed disclosures, including past opinions/ recommendations in the last 12 months and conflict of interests, as well as disclaimers.

A covering strategist may have a financial interest in the debt or equity securities of this company/issuer. This document must not be forwarded or otherwise made available to any other person without the express written consent of Standard Chartered Group.

Deposit Insurance Scheme Singapore dollar deposits of non-bank depositors are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law. For clarity, these investment products are not deposits and do not qualify as an insured deposit under the Singapore Deposit Insurance and Policy Owners’ Protection Schemes Act 2011. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured.

This advertisement has not been reviewed by the Monetary Authority of Singapore.