This is to inform that by clicking on the hyperlink, you will be

leaving

sc.com/sg

and entering a website operated by other parties.

Such links are only provided on our website for the convenience of

the Client and Standard Chartered Bank does not control or endorse

such websites, and is not responsible for their contents.

The use of such website is also subject to the terms of use and

other terms and guidelines, if any, contained within each such

website. In the event that any of the terms contained herein

conflict with the terms of use or other terms and guidelines

contained within any such website, then the terms of use and other

terms and guidelines for such website shall prevail.

*SingPass holders with a MyInfo profile can use MyInfo to automatically fill up the form. By clicking “Next”, you will be re-directed to the MyInfo portal, which is not owned or controlled by Standard Chartered Bank (Singapore) Limited or any member of the Standard Chartered Group (the “Bank”). The Bank bears no liability or responsibility over your usage of the MyInfo portal.

*Please note that MyInfo is temporarily unavailable at the stipulated downtimes:

Mon, Tues, Thurs, Fri, Sat: 5:00AM to 5:30AM. Wed: 2:00AM to 6:00AM. Sun: 2:00AM to 8:30AM

I am an existing Standard Chartered Current/Checking/Savings Account holder

*SingPass holders with a MyInfo profile can use MyInfo to automatically fill up the form. By clicking “Next”, you will be re-directed to the MyInfo portal, which is not owned or controlled by Standard Chartered Bank (Singapore) Limited or any member of the Standard Chartered Group (the “Bank”). The Bank bears no liability or responsibility over your usage of the MyInfo portal.

*Please note that MyInfo is temporarily unavailable at the stipulated downtimes:

Mon, Tues, Thurs, Fri, Sat: 5:00AM to 5:30AM. Wed: 2:00AM to 6:00AM. Sun: 2:00AM to 8:30AM

I am an existing Standard Chartered Current/Checking/Savings Account holder

Find out if you can afford a property upgrade and retire as planned.

TL;DR

Thinking about upgrading your residential property? Here are the things you should know:

1. This is a big decision, but you can make an informed choice and avoid regrets (Read on for the steps.)

2. A space upgrade is great, just beware the potential lifestyle downgrade when your disposable income temporarily falls (unless you’ve just gotten promoted or a large enough increment to cover your monthly mortgage repayment)

3. Your ability to afford that dream home depends on

a) the amount of cash savings you have,

b) the amount of Central Provident Fund (CPF) available in your Ordinary Account, and

c) the amount you can borrow from the bank.

4. Not great with spreadsheets? Map and assess the feasibility with Standard Chartered Goals Planner to aid your decision making

Property upgrade – A hallmark of progress

For many years, the Singaporean dream constitutes the five C’s – cash, car, credit card, condominium (“condo”), and country club membership. While the five C’s are said to be shifting, they still hold to some extent. Over the past two decades, the proportion of resident households living in HDB flats fell from 88% to 78.7%. In contrast, the figures for condos increased from 6.5% to 16%, underscoring property upgrade as a hallmark of progress in life. In this article, we’ll focus on the condo (and landed property) dream.

Getting the big picture right with Standard Chartered Goals Planner

If you’re reading this, congratulations on thinking about a property upgrade. But did you know that on average, a condo costs S$1.8 million and a landed property costs S$5 million^? It certainly isn’t a small sum, so you definitely need to consider if it is indeed an upgrade or probably just a downgrade in disguise.

To make things simpler for you, we have developed Standard Chartered Goals Planner, a free and comprehensive financial planning tool, to help you visualise your financials at every stage of your life. So, you can make informed decisions for yourself. All you need to do is to login to Online Banking on your laptop or SC Mobile on your mobile device and navigate to SC Goals Planner. Once you get there, you may begin by inputting your details and you are set to go!

Start by making sure that the essentials are covered

Before you decide to upgrade, think about your long-term goals as they may require you to make ample financial preparations in time to come. Such goals can include, but are not limited to, providing for your children’s educational needs and retiring comfortably. Plot these essentials and make sure that any financial decision you make later on would not affect your ability to meet these needs.

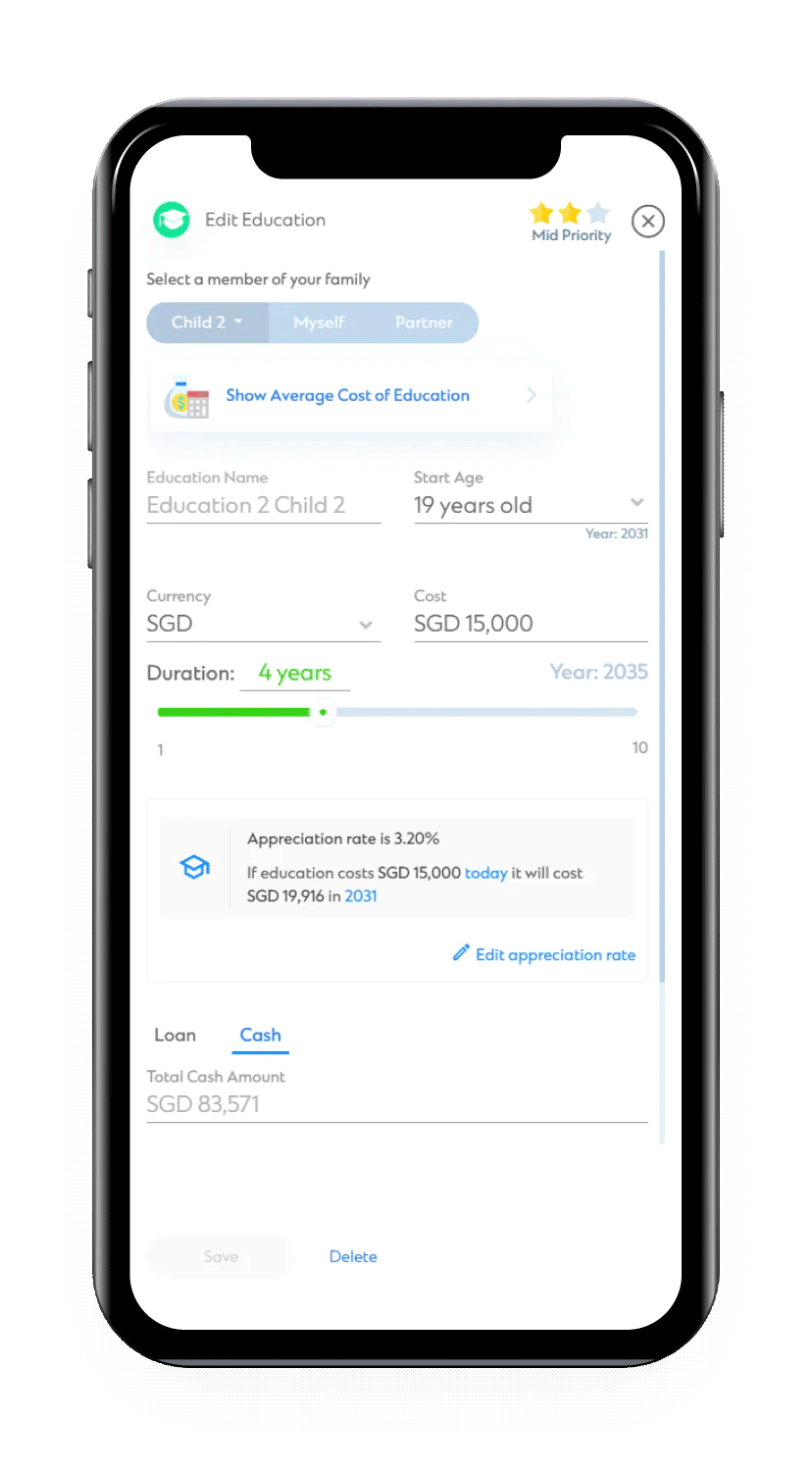

Planning for your children’s educational needs

We know that university costs can vary significantly across different countries and courses. Whether you intend to send your children to local or overseas universities, we got you covered. Once you indicate the current cost, SC Goals Planner will automatically factor in inflation to help you determine how much you’ll need by the time your children enrol in universities.

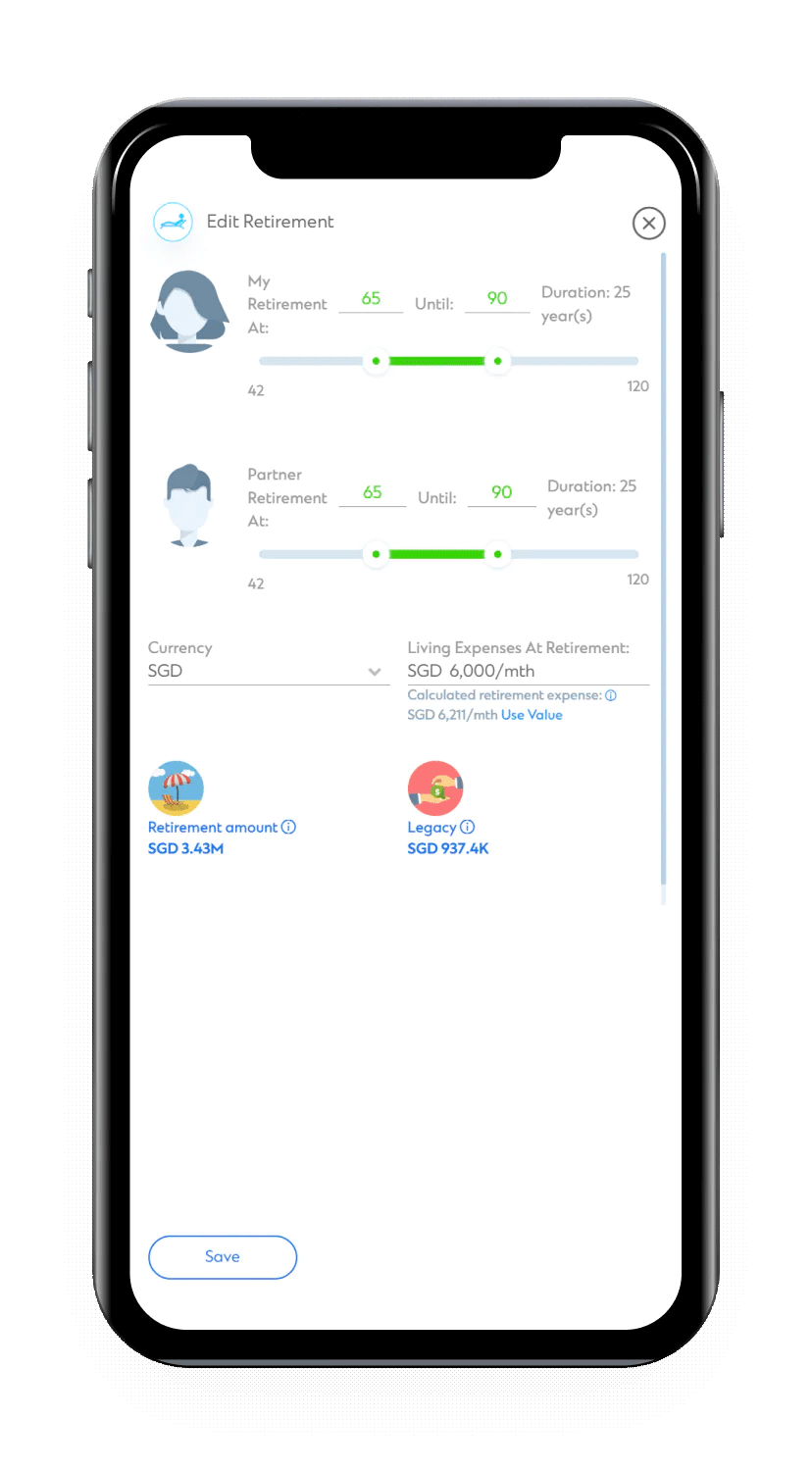

Planning for your retirement

Today, the minimum statutory retirement and re-employment ages in Singapore stands at 62 and 67 years old respectively and will be raised to 65 and 70 years old by year 2030^. Besides, the yearly increment in CPF Basic Retirement Sum (BRS)^ raised the bar for retirement adequacy. So while you may have plans to enjoy the property upgrade now, it may not be wise if it affects your ability to sustain your lifestyle when you retire. There is no hard and fast rule when it comes to retirement preparation – the key is to figure out how much you would need and plan adequately for it.

Once you’re confident of meeting these needs, you can think about a property upgrade with less worries.

Are you eligible for a property upgrade?

Before you jump the gun and do the math, you should find out if you pass the eligibility check.

If you currently own a HDB flat, you will need to satisfy the Minimum Occupation Period (MOP) of five years^ before you can sell / rent out your HDB flat or purchase a private property. If you own a condo or a landed property, the MOP would be three years^. Otherwise, a Seller’s Stamp Duty (SSD) applies. Do note that only Singaporeans can own a HDB flat and a private property at the same time.

What do you intend to do with your first property?

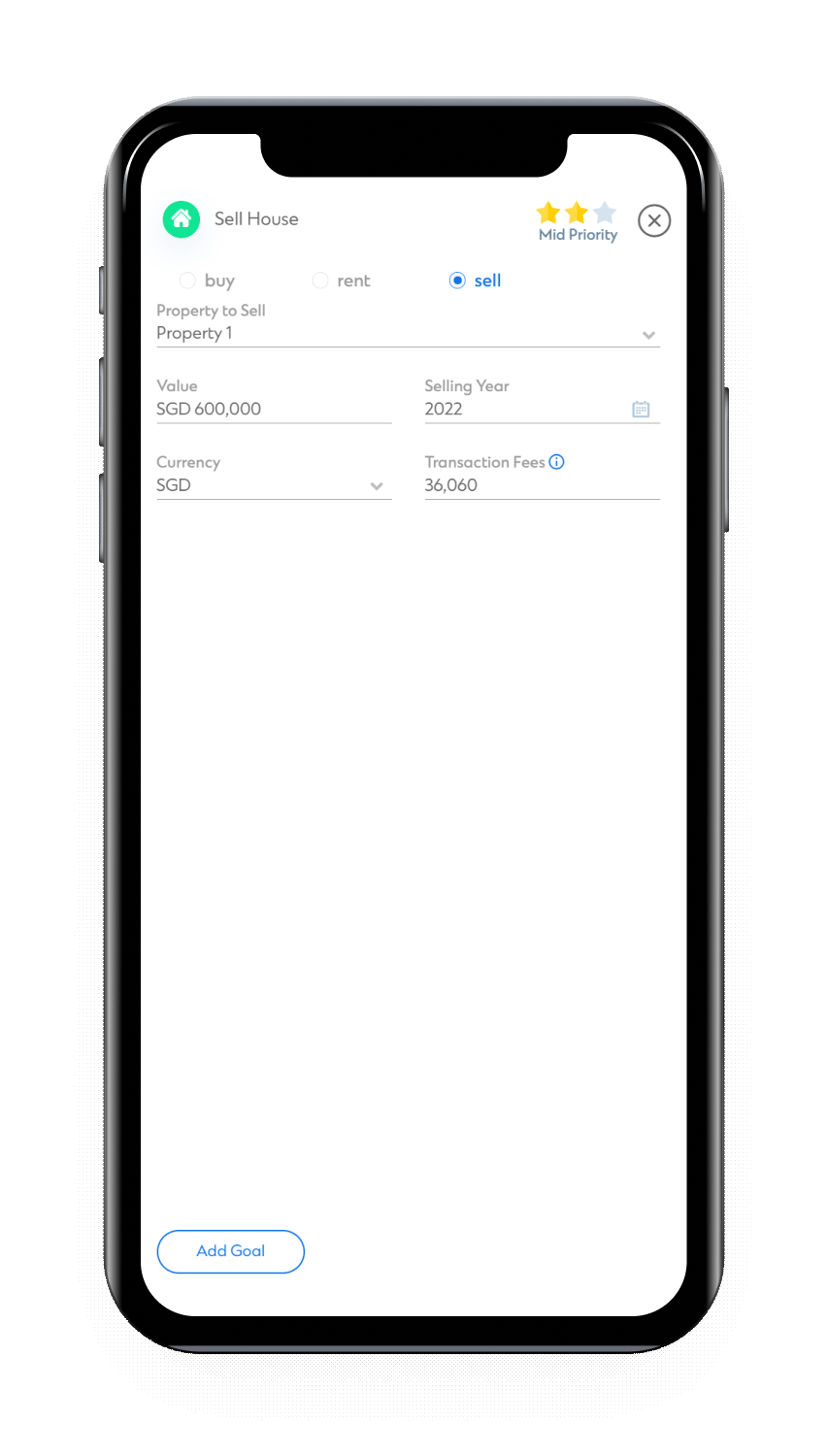

Provided you have an option to keep your first home, the question of “keeping or selling?” greatly depends on your finances. Some homeowners may prefer to keep and rent it out for a passive income, while others sell to finance part of their second home.

The next question follows, “To buy or sell first?” Generally, it’s better to sell first unless you have nowhere to stay in the interim. By selling first, you can better grasp your budget and need not pay the Additional Buyer’s Stamp Duty (ABSD). Should you decide to buy first, you can apply for an ABSD remission, but only if you manage to sell your first property within six months of the second purchase and at least one of the owners is a Singapore citizen. To avoid the costly implications of a potential miscalculation, the general rule of thumb is to sell first and buy later.

Can you really afford a property upgrade?

Time for the million-dollar (literally) question – can you really afford it? For most people, the financing options revolve around their cash savings, available funds in their Central Provident Fund Ordinary Account (CPF-OA), and a bank loan. Here are some factors that would affect your financing options.

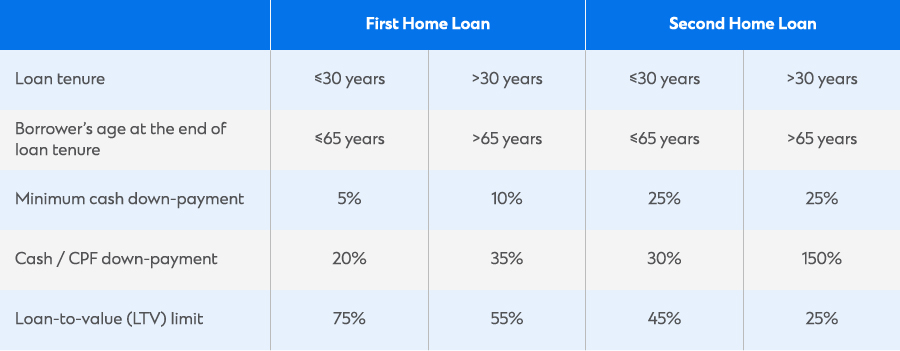

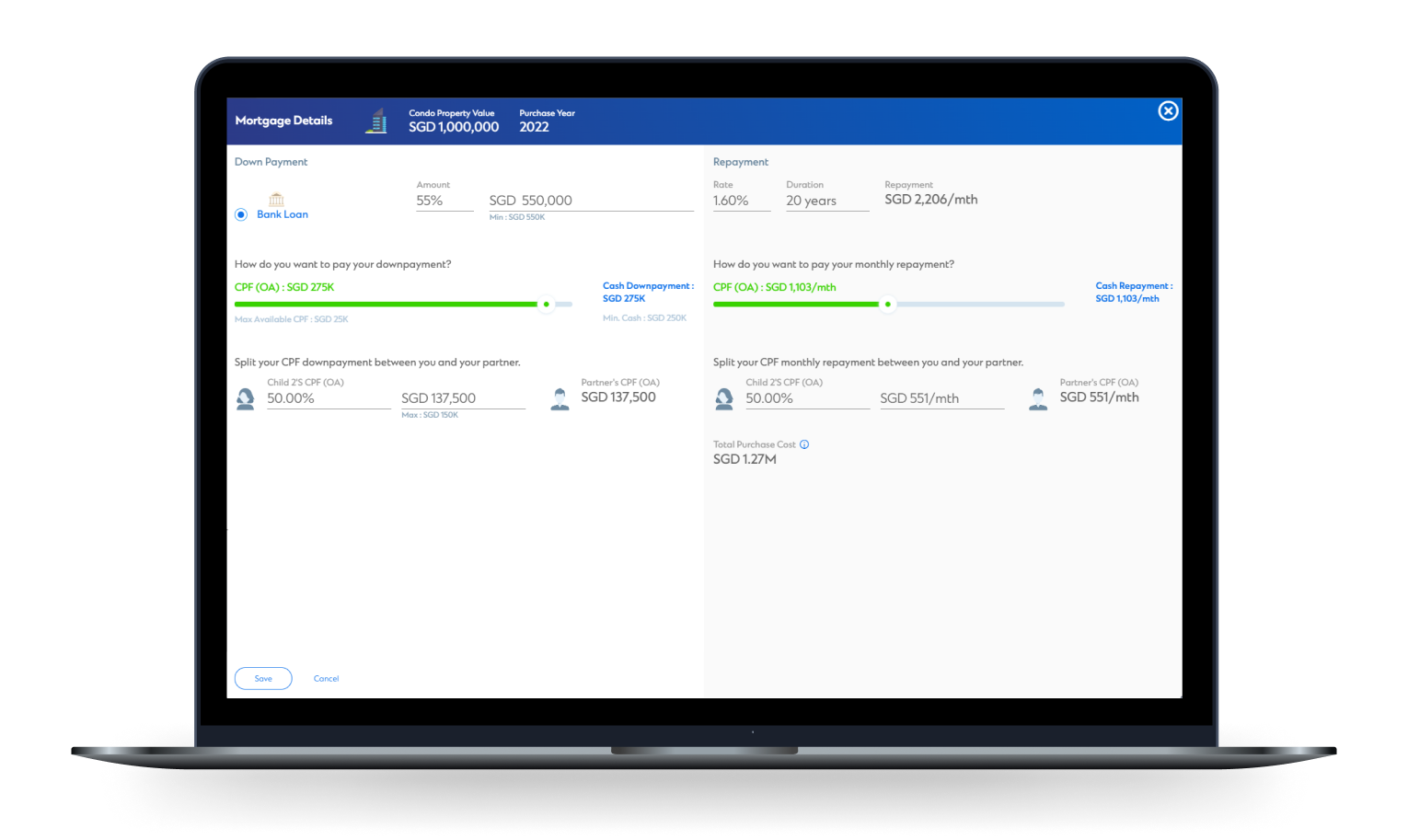

Loan-to-Value (LTV) limit refers to the percentage you can borrow from the bank^, based on the lower of the market value or purchase price of the property. Supposed you have fully repaid any outstanding loan on your first property, you would get the rate for “First Home Loan”. Otherwise, it would be considered a “Second Home Loan” and you would be subject to a lower LTV limit.

2) Total Debt Servicing Ratio (TDSR)

Under the TDSR framework, the total amount of monthly debt obligations which a borrower can have is up to 55% of their gross monthly income. This includes the monthly repayment on the home loan, and any outstanding debt which a borrower may have such as car and credit card loans.

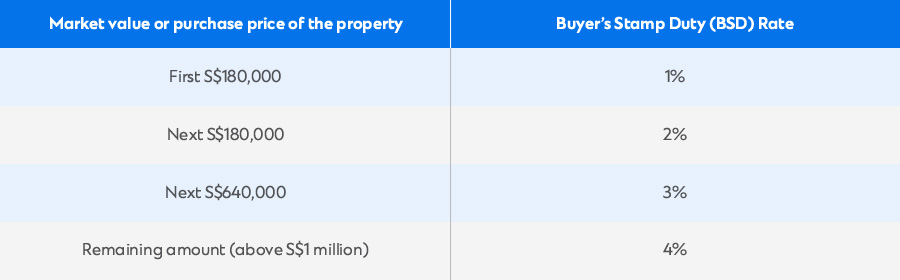

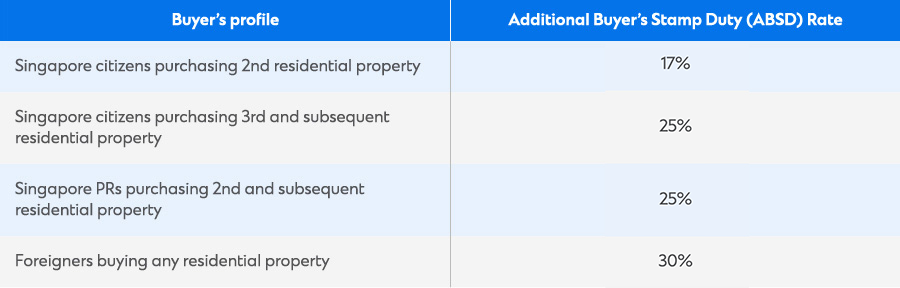

As you are already well-aware of, you’re required to pay the mandatory BSD on any property you purchase. To help you recap, here are the rates.

Unless you’ve already sold your first property, you would be liable to pay an ABSD on top of the BSD^. Fun fact: It is one of the most painful measures as it increases your overall costs by a whopping 17% to 30%.

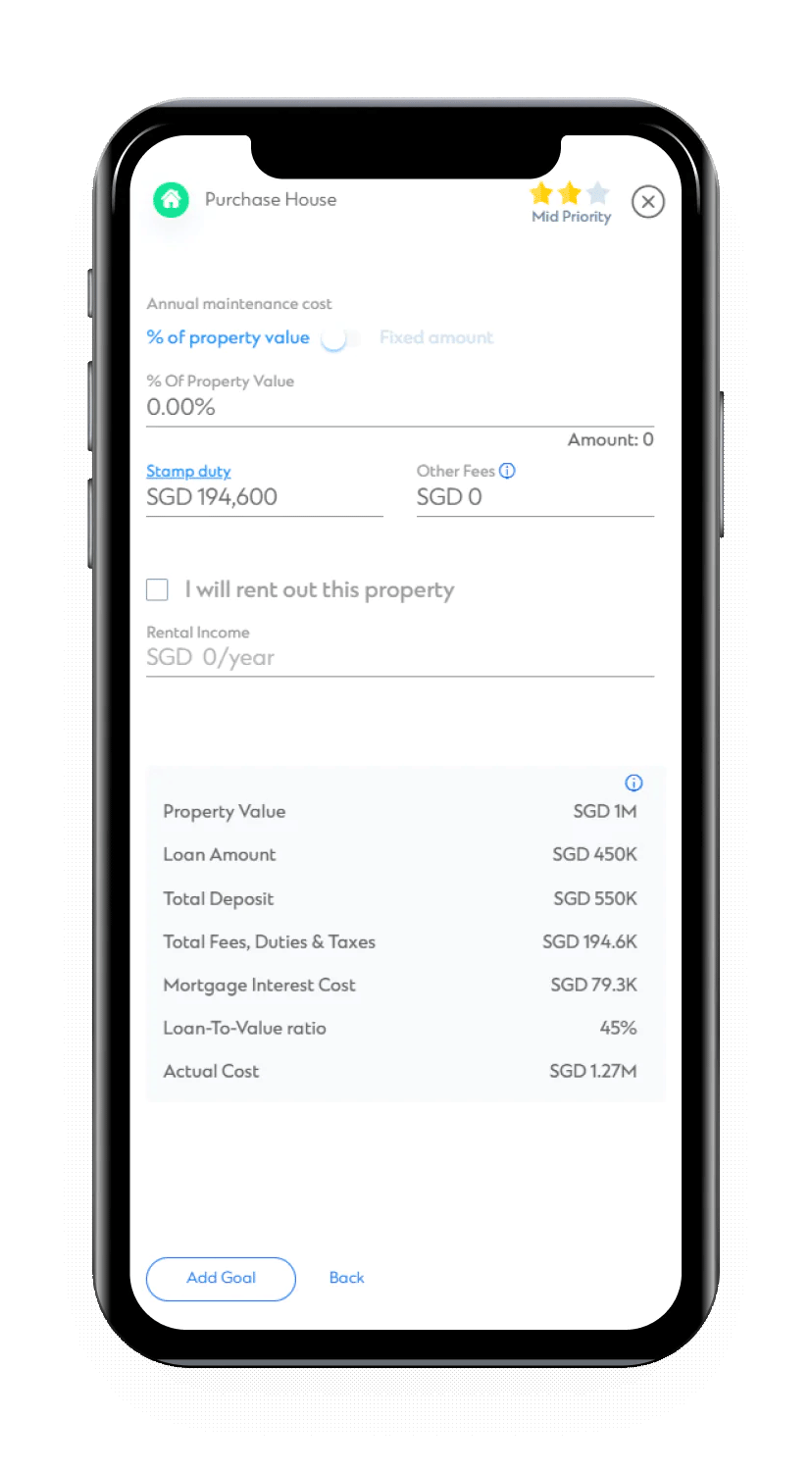

4) Property tax

Since you’re already thinking about owning your second home, we’re sure you are familiar with property tax. The property tax that will be charged on your second property is calculated in a similar manner – based on the property’s “Annual Value” (AV). This is dependent on its estimated market rental value. If you’re unsure of the property’s AV, you can refer to IRAS’ site.

5) Other costs

These costs may seem relatively small compared to the purchase price and BSD, but we want to make sure you are aware of such costs, so you won’t get a shock later in your purchase journey. These include legal / conveyancing fees and property agent commission. For any private property purchase, you are required to hire a private lawyer to help you execute the legal processes of the transaction. This typically costs anywhere between S$2,500 and S$5,000. Fortunately, there is no property agent commission charged to the buyers as it is typically absorbed by the sellers.

Know how much you can afford

We hope that you’re not confused at this stage. If you are, we understand because there are simply too many factors to consider. The great thing about SC Goals Planner is that you can perform simulations to know how your decisions affect your finances before you even make a real decision. On top of that, you don’t need to worry about the sequence of your actions, the amount of cash savings you have, or the amount of CPF you can withdraw to make the purchase as SC Goals Planner will factor all these in while you simulate your financial dreams. Just simply plot them in, and it will do all the math for you!

So, is upgrading your property a strategic move?

After planning all your financial goals, you would expect to see either of the following three conclusions:

You are out of cash – This is far from ideal. Fortunately, you would know it beforehand, so you can recalibrate your finances

You do not end up with a shortfall, but have minimal buffer – This is alright, but you need to think about ways to increase your buffer

You have adequate buffer – This is the ideal situation to ensure your comfort during old age, and possibly having sufficient to leave a legacy for your children (if any)

Built to grow with you and your changing needs, SC Goals Planner provides you with a comprehensive overview of your finances depending on your financial choices. At Standard Chartered, we want the best for you, and we want you to make informed decisions. Simulate your dreams using SC Goals Planner and find out for yourself if a property upgrade is indeed an achievable and a wise decision. If it’s not, you can always make some adjustments today to achieve that dream in the near future. Good luck!

Disclaimer

This article is for general information only and it does not constitute an offer, recommendation or solicitation of an offer to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments. This article has not been prepared for any particular person or class of persons and does not constitute and should not be construed as investment advice or an investment recommendation. It has been prepared without regard to the specific investment objectives, financial situation or particular needs of any person or class of persons. You should seek advice from a licensed or an exempt financial adviser on the suitability of a product for you, taking into account these factors before making a commitment to purchase any product or invest in an investment. In the event that you choose not to seek advice from a licensed or an exempt financial adviser, you should carefully consider whether the product or service described herein is suitable for you.

You are fully responsible for your investment decision, including whether the investment is suitable for you. The products/services involved are not principal-protected and you may lose all or part of your original investment amount. Standard Chartered Bank (Singapore) Limited will not accept any responsibility or liability of any kind, with respect to the accuracy or completeness of information in this article.

Deposit Insurance Scheme

Singapore dollar deposits of non-bank depositors are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law. For clarity, these investment products are not deposits and do not qualify as an insured deposit under the Singapore Deposit Insurance and Policy Owners’ Protection Schemes Act 2011. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured.

The information stated in this article is accurate amp s at the date of publication.