As low as 1.85%1

Annualized Percentage Rate

up to HKD 8,000

Cash Rebate

0%

Handling fee

✔ Loan amount up to 18X monthly salary or HKD4,000,000 (whichever is lower)

✔ Loan tenor up to 60 months

Eligibility: Hong Kong resident aged 20 or above; fixed annual income of HKD96,000 or above

Access to Personal Instalment Loan Key Fact Statement

Terms and conditions applies.

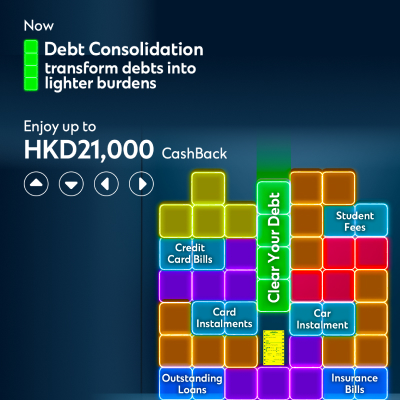

As low as 0.20%2

Monthly Flat Rate

up to HKD $21,000

Cash Rebate

up to 95%

interest saved

✔ Consolidate multiple bills into a single payment

✔ Loan amount up to 24X salary or HKD 2,000,000 (whichever is lower)

✔ Loan tenor up to 84 months

✔ 0% Handling fee

Eligibility: Hong Kong resident aged 20 or above; fixed annual income of HKD96,000 or above

Access to Debt Consolidation Program Key Fact Statement

Terms and conditions applies.

✔ 0% handling fee

✔ Documents waiver

✔ Loan amount up to 18X salary or HKD 2,000,000 (whichever is lower)

✔ Loan tenor up to 60 months

Eligibility: Standard Chartered Bank existing loan customer

Access to Personal Instalment Loan Top Up Service Key Fact Statement

Terms and conditions applies.

as low as 0.083%^

Monthly handling fee

✔ New online platform to get cash from card in 30 seconds

✔ Loan amount up to 18X salary or HKD 1,200,000 (whichever is lower)

✔ Loan tenor up to 60 months

✔ HKD200 application free waiver

Eligibility: Standard Chartered Bank existing cardholders

Access to Get Cash From Credit Card Key Fact Statement

Terms and conditions applies.

HKD 500

Minimum spending

✔ Monthly handling fee as low as 0.19%5

✔ Flexible instalment period 3-60 months

✔ Few easy steps to complete the application in 5-minutes

Eligibility: Standard Chartered Bank existing cardholders

Access to Split Your Credit Card Bills Key Fact Statement

Terms and conditions applies.

✔ Enjoy first year annual fee waiver

✔ Credit limit up to HKD800,000 or 12 times of your monthly salary (whichever is lower)

✔ 2.10% p.a. interest rate for the first 3-month6

✔ Flexible re-borrow

Eligibility: Hong Kong resident aged 18 or above; fixed annual income of HKD96,000 or above

Access to Revolving Cash Card Key Fact Statement

Terms and conditions applies.

Terms and conditions apply, please click corresponding “FIND OUT MORE” for details.

Please be aware of any bogus calls, SMS messages, emails, letters or communications through any other channels from fraudsters for referring personal loan, seeking for client’s personal information or even requesting clients to transfer funds to third party account. The Bank would like to remind clients not to disclose any personal information to suspicious calls or transfer funds to third party account and the Bank has not authorized or appointed any intermediaries to conduct marketing activities of personal loan. If in doubt, you may verify the caller details with the bank. Please contact our staff at 2886-8868 (press 2-6-0) or report to police immediately.